“Battlefield of Metals! Non‑Ferrous Metals June 2026: Watching Recovery Signals After the May Price Storm – Copper & Aluminium Building a New Base for 2026”

Non‑Ferrous Metals Market – June 2026: Battlefield of Volatility!

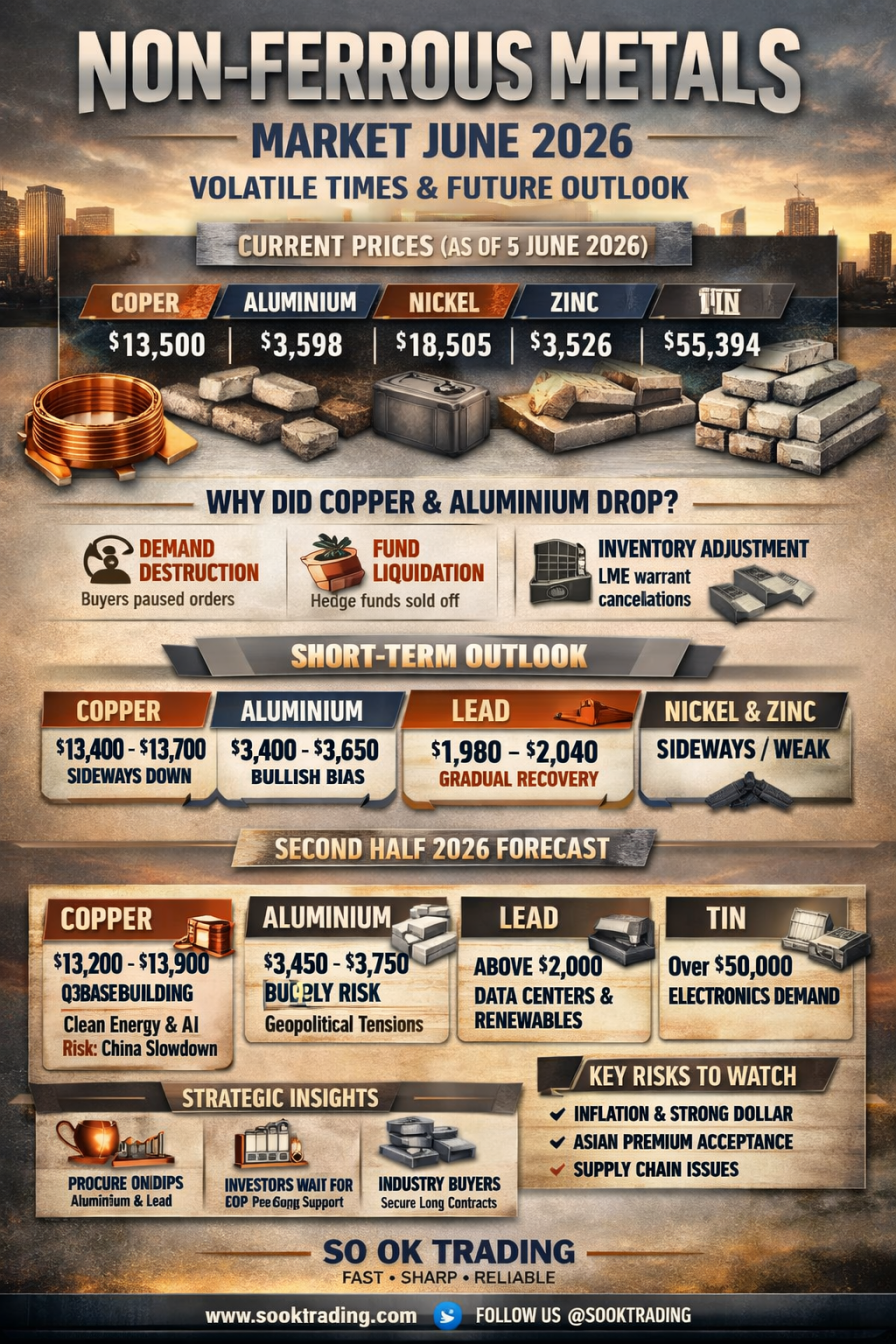

By SO OK TRADING | 7 June 2026

This month, the Non‑Ferrous Metals market on the London Metal Exchange (LME) has become a true battlefield of volatility, reflecting both macroeconomic pressures and geopolitical factors. Copper and aluminium, which had surged to multi‑year highs, corrected sharply in late May before beginning to establish new bases in early June. Meanwhile, lead, tin, nickel, and zinc each show distinct trajectories worth monitoring.

Latest Prices (as of 5 June 2026)

Copper: $13,500/ton

Aluminium: $3,598/ton

Nickel: $18,505/ton

Zinc: $3,526/ton

Tin: $55,394/ton

Lead: $2,006/ton

“Copper & Aluminium remain in backwardation — signaling tight demand for immediate delivery.”

Why Did Copper & Aluminium Drop?

Demand Destruction: Prices near $14,000 forced buyers to pause orders.

Funds Liquidation: Hedge funds sold off positions amid China’s slowdown.

Inventory Adjustment: Cancelled LME warrants reflected supply rebalancing.

➡ This was a cooling correction, not a permanent downtrend.

Short‑Term Outlook (8–12 June 2026)

Copper: Sideways Down ($13,400–$13,700)

Aluminium: Bullish Bias / High Volatility ($3,400–$3,650)

Lead: Gradual Recovery ($1,980–$2,040)

Nickel & Zinc: Sideways to Weak / Stable

Second Half 2026 Forecast – Non‑Ferrous Products

Copper: $13,200–$13,900 base‑building in Q3, driven by clean energy, AI, and data‑center demand.

Risk: China’s slowdown could test $12,800 temporarily.

Aluminium: $3,450–$3,750 sustained highs, supported by geopolitical tensions and Guinea’s bauxite export controls.

Risk: Technical sell‑offs if Middle East tensions ease sooner than expected.

Lead: Above $2,000, supported by lead‑acid battery demand in data centers and renewable systems.

Tin: Over $50,000, sustained by strong electronics demand.

⚠️ Key Risks to Watch

US/EU CPI & inflation → Dollar strength could pressure prices.

Asian physical premiums → Will buyers in China and ASEAN accept current levels?

Supply chain uncertainty → Mining output and shipping routes remain volatile.

Strategic Insights

Procurement: Hedge aluminium and lead on dips.

Short‑term Investors: Wait for copper to form a solid base before re‑entering.

Industrial Buyers: Use current correction to secure long‑term contracts and monitor scrap price drops.

Market Summary

The Non‑Ferrous Metals market is entering a new price‑base zone after May’s sharp correction. With fundamentals still strong and supply tight, the second half of 2026 offers potential for recovery — provided global inflation and geopolitical risks remain manageable. Smart risk management and timely hedging will be the keys to success in this volatile phase.

SO OK TRADING – FAST • SHARP • RELIABLE www.sooktrading.com Facebook: SO OK TRADING