「金属战场!2026年6月非铁金属:聚焦五月价格风暴后的复苏信号 —— 铜与铝正在构筑2026年的新基石」

Last updated: 7 Jun 2026

4135 Views

2026年6月非铁金属市场 – 波动的战场!

SO OK TRADING | 2026年6月7日

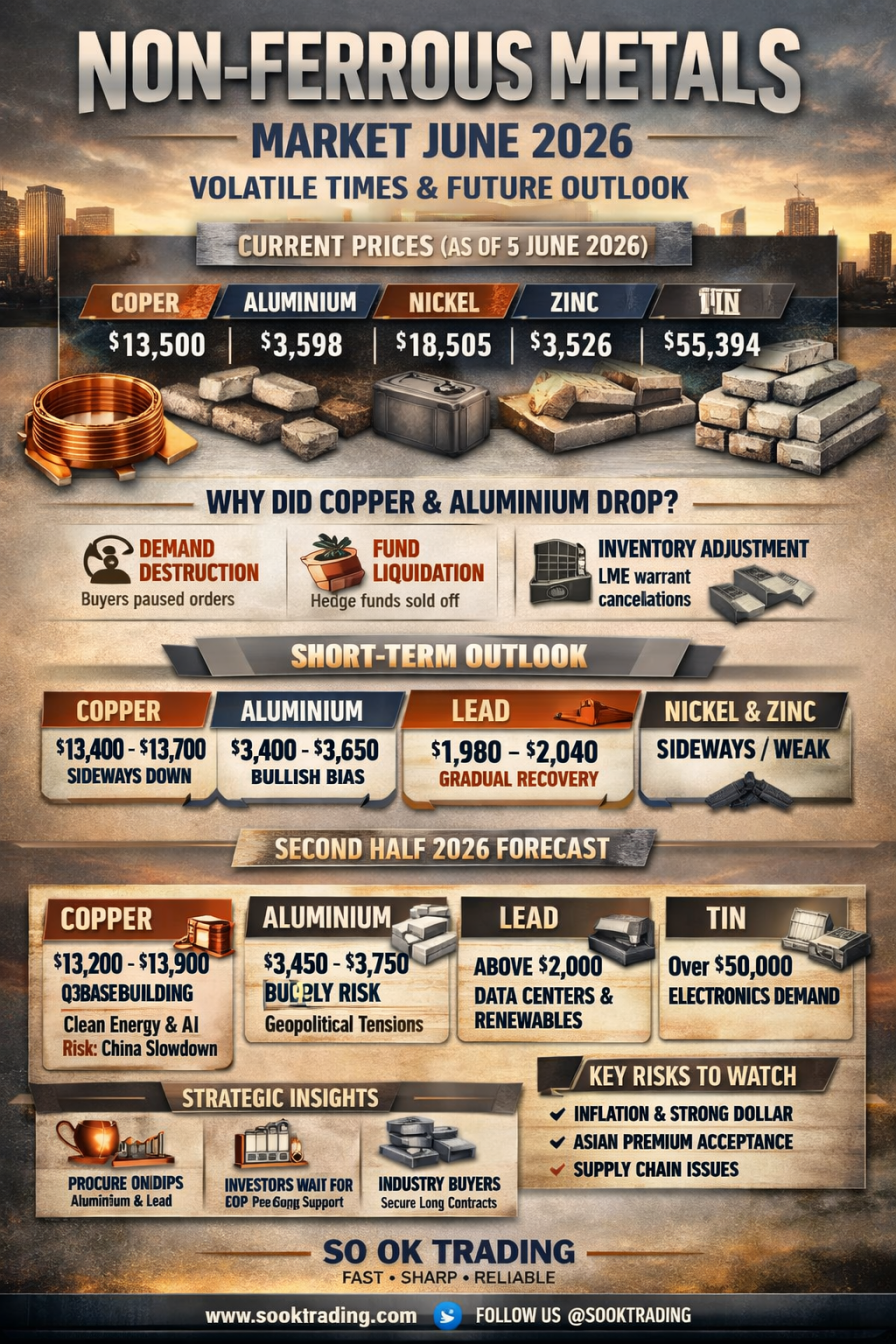

本月,伦敦金属交易所(LME)的非铁金属市场正处于“剧烈波动的战场”。 铜和铝在今年创下多年新高后,于5月底大幅回调,并在6月初开始建立新的价格基准。与此同时,铅、锡、镍和锌也呈现出各自独特的走势,值得关注。

最新价格(截至2026年6月5日)

铜(Copper):13,500美元/吨

铝(Aluminium):3,598美元/吨

镍(Nickel):18,505美元/吨

锌(Zinc):3,526美元/吨

锡(Tin):55,394美元/吨

铅(Lead):2,006美元/吨

“铜与铝仍处于现货升水(Backwardation)状态,显示即期交割需求依然紧张。”

为什么铜和铝价格大幅下跌?

需求破坏(Demand Destruction): 高价导致实际需求停滞

基金平仓(Funds Liquidation): 中国经济放缓促使投机基金获利了结

库存调整(Inventory Management): LME仓库取消提单,反映供需再平衡

➡ 这是一场“降温调整”,而非长期下跌趋势。

短期展望(2026年6月8日–12日)

铜:13,400–13,700美元/横盘偏弱

铝:3,400–3,650美元/偏强波动

铅:1,980–2,040美元/逐步回升

镍与锌:横盘或偏弱

2026年下半年市场预测

铜: 13,200–13,900美元区间筑底,受AI与清洁能源需求支撑

铝: 3,450–3,750美元维持高位,受地缘政治与几内亚铝土矿出口管制影响

铅: 稳定在2,000美元以上,数据中心与新能源系统的铅酸电池需求推动

锡: 高于50,000美元,电子产业需求强劲

⚠️ 需关注的风险因素

美国与欧洲的CPI与通胀 → 美元走强将直接压制金属价格

亚洲市场的现货升水接受度

矿山供应与航运路线的不确定性

SO OK TRADING – FAST • SHARP • RELIABLE

www.sooktrading.com Facebook: SO OK TRADING

SO OK TRADING | 2026年6月7日

本月,伦敦金属交易所(LME)的非铁金属市场正处于“剧烈波动的战场”。 铜和铝在今年创下多年新高后,于5月底大幅回调,并在6月初开始建立新的价格基准。与此同时,铅、锡、镍和锌也呈现出各自独特的走势,值得关注。

最新价格(截至2026年6月5日)

铜(Copper):13,500美元/吨

铝(Aluminium):3,598美元/吨

镍(Nickel):18,505美元/吨

锌(Zinc):3,526美元/吨

锡(Tin):55,394美元/吨

铅(Lead):2,006美元/吨

“铜与铝仍处于现货升水(Backwardation)状态,显示即期交割需求依然紧张。”

为什么铜和铝价格大幅下跌?

需求破坏(Demand Destruction): 高价导致实际需求停滞

基金平仓(Funds Liquidation): 中国经济放缓促使投机基金获利了结

库存调整(Inventory Management): LME仓库取消提单,反映供需再平衡

➡ 这是一场“降温调整”,而非长期下跌趋势。

短期展望(2026年6月8日–12日)

铜:13,400–13,700美元/横盘偏弱

铝:3,400–3,650美元/偏强波动

铅:1,980–2,040美元/逐步回升

镍与锌:横盘或偏弱

2026年下半年市场预测

铜: 13,200–13,900美元区间筑底,受AI与清洁能源需求支撑

铝: 3,450–3,750美元维持高位,受地缘政治与几内亚铝土矿出口管制影响

铅: 稳定在2,000美元以上,数据中心与新能源系统的铅酸电池需求推动

锡: 高于50,000美元,电子产业需求强劲

⚠️ 需关注的风险因素

美国与欧洲的CPI与通胀 → 美元走强将直接压制金属价格

亚洲市场的现货升水接受度

矿山供应与航运路线的不确定性

SO OK TRADING – FAST • SHARP • RELIABLE

www.sooktrading.com Facebook: SO OK TRADING

Related Content

可再生能源 —— 生物燃料

正在取代化石燃料和煤炭的世界级游戏规则改变者

世界正在全面迈入“清洁能源时代”。能源不仅是推动经济的动力,更是维护环境平衡和人类未来的关键。这场转型不仅仅是技术革新,而是全球能源体系的根本重塑,将彻底改变我们对能源的认知与使用方式。

可再生能源,例如 太阳能电池板(Solar Cell) 和 木质颗粒燃料(Wood Pellets),正在成为全球发电和工业的核心力量。其成本持续下降,效率显著提升。

在中国和欧洲每年快速新增数百吉瓦可再生能源的同时,日本、韩国和泰国等亚洲国家也在加速迈向清洁能源之路,以期在未来几十年内实现 “净零排放” (Net Zero Emissions) 的目标。

SO OK TRADING 已准备好成为您在新能源时代的商业伙伴。

我们提供 太阳能电池板一站式安装服务 以及 高品质木质颗粒燃料出口,帮助您的企业在清洁能源世界中稳步前行。

17 Apr 2026

「七月火热!基础金属飙升——原油暴跌,美元走强冲击全球市场」

SO OK TRADING 全球市场分析 | 2026年7月11日

2026年7月,全球市场正处于剧烈波动之中。

贵金属因美联储加息压力而进入“调整期”,而基础金属则在人工智能与清洁能源产业的推动下“强劲上涨”。

与此同时,原油市场因供应过剩与地缘政治紧张局势的缓解,面临大规模抛售压力。

11 Jul 2026

历史性的“特朗普–习近平峰会”(2026年5月12日至15日)不仅仅是一次礼节性访问,而是撼动世界的大交易,涵盖经济、能源与科技。此次会晤展现了两大强国之间复杂的博弈,它们合计占全球GDP的42%。

从中东战争到台湾问题,从稀土贸易到高端技术出口管制的放宽——谈判桌上的每一次“交锋”,都可能成为决定全球市场走向、油价走势以及未来AI供应链的关键变量。

这是一场全球必须关注的峰会。如果协议成功,世界经济或将重回稳定;若失败,其冲击将波及全球民生成本,包括泰国在内的各国都会受到影响。

SO OK TRADING : FAST • SHARP • RELIABLE

在瞬息万变的世界中,您的商业伙伴

14 May 2026