「ホルムズ海峡炎上!世界物流に激震、輸送費が急騰 ― 中東からのSUPPLY SHOCK、コスト高と激しい変動の時代へ」 SO OK TRADINGによる記事 | 2026年3月13日

Last updated: 13 Mar 2026

1962 Views

「ホルムズ海峡炎上 ― 世界物流に激震、輸送費が爆発的に高騰」

SUPPLY & DEMAND SHOCK 中東発 | 2026年3月13日

SO OK TRADINGによる記事

最新状況

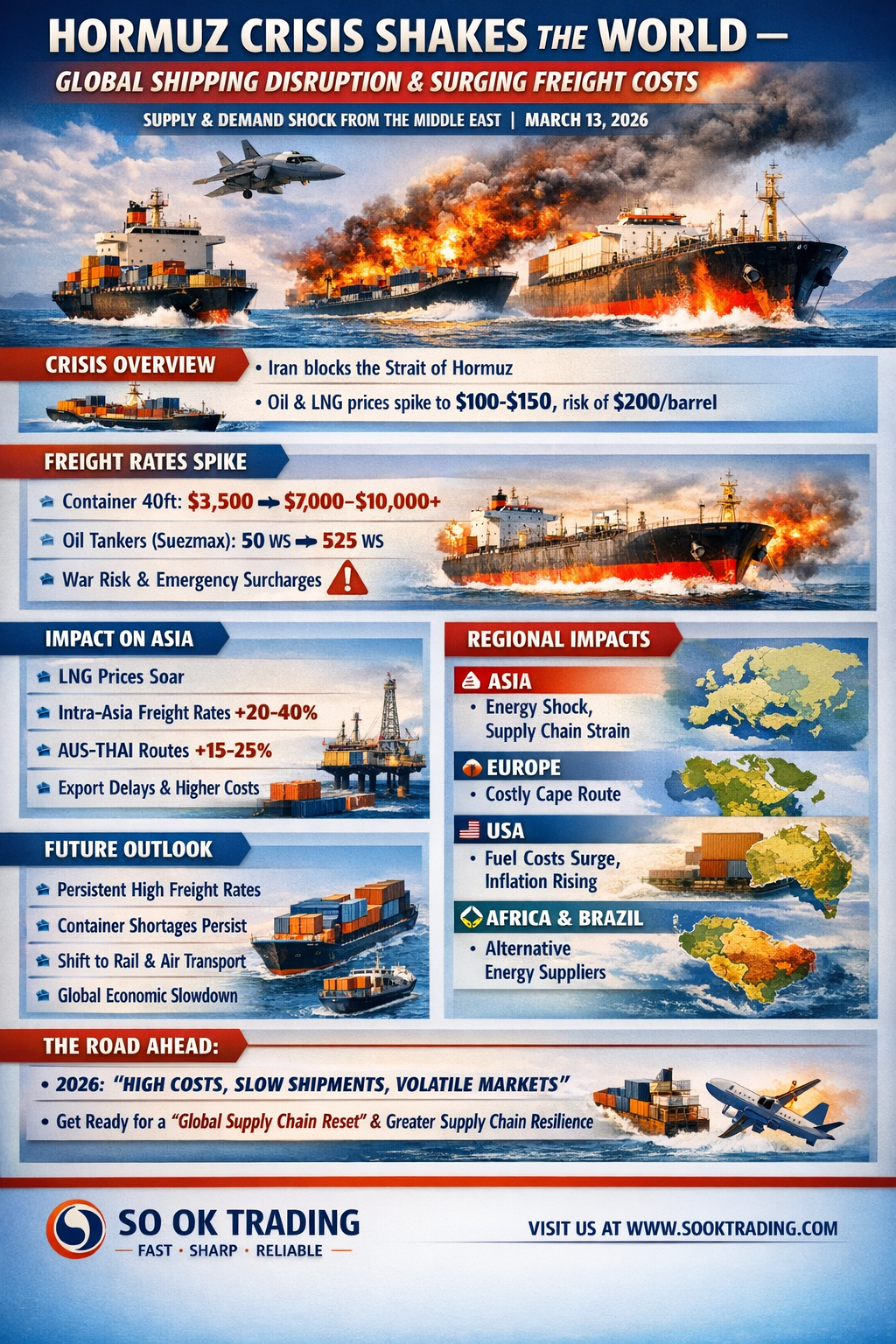

2026年3月、イランがホルムズ海峡を事実上封鎖し、複数の商船を攻撃。タイの「マユリ・ナリー号」を含む被害が発生し、世界の石油・LNG輸送の20〜30%が即座に停止。原油価格は100〜150ドル/バレルに急騰し、事態が長引けば200ドルに達する可能性もある。

運賃の急騰

コンテナ40フィート:3,500ドル ➜ 7,000〜10,000ドル以上

原油タンカー(Suezmax):50〜225 WS ➜ 525 WS

SCFI中東航路指数:わずか1週間で72%上昇

緊急附加費(Emergency Freight Increase)、戦争リスクサーチャージ、バンカーサーチャージが世界的に適用

⚡ タイとアジアへの影響

LNGスポット価格の高騰によりタイの発電コストが圧迫

タイ-中国/タイ-日本航路:運賃20〜40%上昇、コンテナ不足

オーストラリア-タイ航路:バンカーサーチャージと保険料上昇により15〜25%増

農産品輸出:遅延とコスト増で競争力低下

地域別影響比較

アジア:エネルギー価格急騰、日本・韓国はLNG依存度が高く直撃。タイも電力コストと運賃上昇に直面。

ヨーロッパ:喜望峰経由の迂回で物流・エネルギーコストが即座に上昇、インフレ圧力増大。

米国:国内産油があるものの世界市場の影響を免れず、燃料費と輸送コスト上昇。

アフリカ・ブラジル:新たなエネルギー供給源として注目され、輸出機会が拡大。

今後の展望(事態が長期化した場合)

高水準の運賃が「ニューノーマル」に

コンテナ不足が深刻化、アジア輸出に大打撃

Sea-to-Airや中欧鉄道など代替輸送手段が増加

バンカーサーチャージが毎月変動、燃料費の不安定化

世界経済は減速し、インフレと購買力低下が顕著に

結論

2026年は「高コスト・長納期・激しい変動」の年。ホルムズ海峡危機が長引けば、世界は「Global Supply Chain Reset」に突入し、物流とエネルギーコストは容易に元に戻らない。タイやアジアの企業は、リスク分散・新航路の活用・サプライチェーンの柔軟性強化によって競争力を維持する必要がある。

✨ この危機は一時的なものではなく、世界が新たな物流・エネルギーの時代へ移行している警鐘である。迅速に適応し、積極的な戦略を打ち出す企業こそが、生き残り成長できる。

SO OK TRADING — あなたのビジネスパートナー

FAST • SHARP • RELIABLE

WWW.SOOKTRADING.COM

SUPPLY & DEMAND SHOCK 中東発 | 2026年3月13日

SO OK TRADINGによる記事

最新状況

2026年3月、イランがホルムズ海峡を事実上封鎖し、複数の商船を攻撃。タイの「マユリ・ナリー号」を含む被害が発生し、世界の石油・LNG輸送の20〜30%が即座に停止。原油価格は100〜150ドル/バレルに急騰し、事態が長引けば200ドルに達する可能性もある。

運賃の急騰

コンテナ40フィート:3,500ドル ➜ 7,000〜10,000ドル以上

原油タンカー(Suezmax):50〜225 WS ➜ 525 WS

SCFI中東航路指数:わずか1週間で72%上昇

緊急附加費(Emergency Freight Increase)、戦争リスクサーチャージ、バンカーサーチャージが世界的に適用

⚡ タイとアジアへの影響

LNGスポット価格の高騰によりタイの発電コストが圧迫

タイ-中国/タイ-日本航路:運賃20〜40%上昇、コンテナ不足

オーストラリア-タイ航路:バンカーサーチャージと保険料上昇により15〜25%増

農産品輸出:遅延とコスト増で競争力低下

地域別影響比較

アジア:エネルギー価格急騰、日本・韓国はLNG依存度が高く直撃。タイも電力コストと運賃上昇に直面。

ヨーロッパ:喜望峰経由の迂回で物流・エネルギーコストが即座に上昇、インフレ圧力増大。

米国:国内産油があるものの世界市場の影響を免れず、燃料費と輸送コスト上昇。

アフリカ・ブラジル:新たなエネルギー供給源として注目され、輸出機会が拡大。

今後の展望(事態が長期化した場合)

高水準の運賃が「ニューノーマル」に

コンテナ不足が深刻化、アジア輸出に大打撃

Sea-to-Airや中欧鉄道など代替輸送手段が増加

バンカーサーチャージが毎月変動、燃料費の不安定化

世界経済は減速し、インフレと購買力低下が顕著に

結論

2026年は「高コスト・長納期・激しい変動」の年。ホルムズ海峡危機が長引けば、世界は「Global Supply Chain Reset」に突入し、物流とエネルギーコストは容易に元に戻らない。タイやアジアの企業は、リスク分散・新航路の活用・サプライチェーンの柔軟性強化によって競争力を維持する必要がある。

✨ この危機は一時的なものではなく、世界が新たな物流・エネルギーの時代へ移行している警鐘である。迅速に適応し、積極的な戦略を打ち出す企業こそが、生き残り成長できる。

SO OK TRADING — あなたのビジネスパートナー

FAST • SHARP • RELIABLE

WWW.SOOKTRADING.COM

関連コンテンツ

「FEDが『据え置き』を選んだのに、市場は『据え置き』ず!最新の金利決定後の資産価格の動きを総まとめ。金を保有している方、または円・人民元の両替を検討している方は必読です。」

昨夜のFED声明を受けて、金・銀・タイバーツの今後の方向性はどうなるのか?最新情報をチェックして、変動に備えましょう

29 Jan 2026

「2026年6月の銅市場 – スーパーサイクルの沸点!」

SO OK TRADING | 2026年6月2日

今月はまさに世界の銅市場における「歴史的転換点」!

価格は過去10年で最高水準に急騰し、AI・電気自動車(EV)・クリーンエネルギーの波により、新たなスーパーサイクルが幕を開けています

2 Jun 2026