トランプ2.0:終わらない関税ゲーム 最高裁が関税を停止 → トランプが即反撃! 旧関税は終了、新たな10%関税が2月24日から世界中に適用 あなたの財布にどんな影響が?今後の展開に注目!

Last updated: 21 Feb 2026

1588 Views

2026年2月20日:世界税制(Aggressive TAX)が停止、しかしゲームはまだ終わらない

― これは「前半終了」にすぎない。ドナルド・トランプ大統領が戦略を修正し、今後の経済・通貨・株式市場・貴金属への影響を見守る局面へ。

記事 BY SO OK TRADING

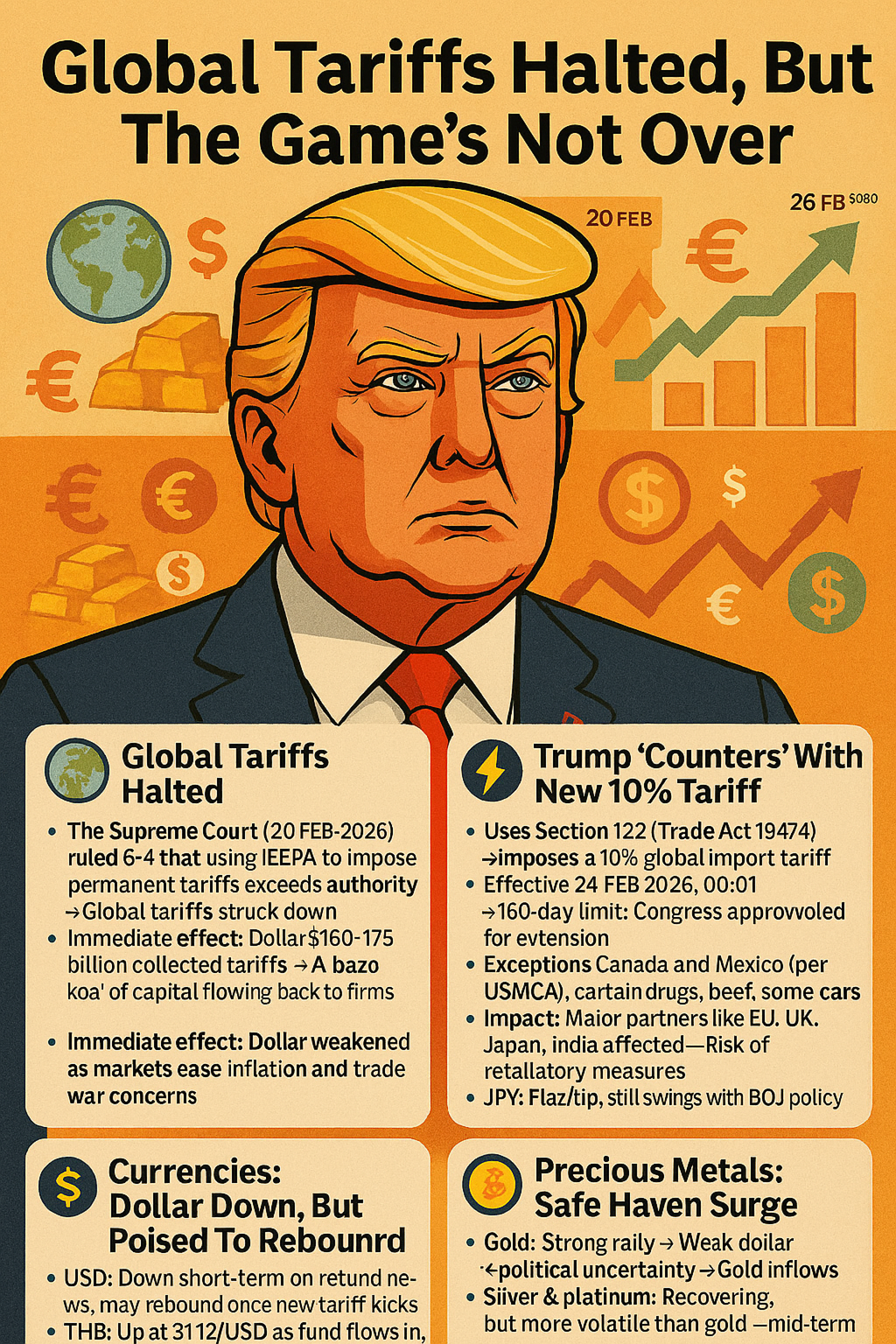

米国最高裁判所の判決(2026年2月20日)

判決結果:6対3で、IEEPA法を用いた恒久的な関税設定は権限の逸脱と判断

結果:包括的関税(Global Tariffs)が撤廃

影響:米国政府はすでに徴収した約1,600~1,750億ドルを輸入企業へ返還する可能性 → この資金は「強力な刺激剤」として民間・株式市場へ流入

即時効果

米ドルは下落:インフレや貿易戦争への懸念が和らぎ、ドル安に

⚡ トランプ大統領「新しいゲーム」― 10%関税

法的根拠:1974年通商法 Section 122

内容:世界全体の輸入品に10%関税を課す

発効:2026年2月24日 午前0時1分から、最長150日間(延長には議会承認が必要)

例外:カナダ・メキシコ(USMCA)、医薬品・牛肉・一部自動車など

影響:EU・英国・日本・インドなど主要貿易相手国が対象 → 報復措置のリスク

通貨市場:ドル安だが反発余地あり

USD:短期的に下落、ただし新関税発効後は反発の可能性

THB:31.12バーツ/ドル付近で堅調、資金流入が背景。ただし政府の介入リスクあり

CNY:6.91元/ドルへ上昇、関税の主要ターゲットでありながら強含み

EUR:ドイツ・欧州輸出への圧力緩和で回復

JPY:小幅な上昇傾向、日銀の政策次第で変動

― これは「前半終了」にすぎない。ドナルド・トランプ大統領が戦略を修正し、今後の経済・通貨・株式市場・貴金属への影響を見守る局面へ。

記事 BY SO OK TRADING

米国最高裁判所の判決(2026年2月20日)

判決結果:6対3で、IEEPA法を用いた恒久的な関税設定は権限の逸脱と判断

結果:包括的関税(Global Tariffs)が撤廃

影響:米国政府はすでに徴収した約1,600~1,750億ドルを輸入企業へ返還する可能性 → この資金は「強力な刺激剤」として民間・株式市場へ流入

即時効果

米ドルは下落:インフレや貿易戦争への懸念が和らぎ、ドル安に

⚡ トランプ大統領「新しいゲーム」― 10%関税

法的根拠:1974年通商法 Section 122

内容:世界全体の輸入品に10%関税を課す

発効:2026年2月24日 午前0時1分から、最長150日間(延長には議会承認が必要)

例外:カナダ・メキシコ(USMCA)、医薬品・牛肉・一部自動車など

影響:EU・英国・日本・インドなど主要貿易相手国が対象 → 報復措置のリスク

通貨市場:ドル安だが反発余地あり

USD:短期的に下落、ただし新関税発効後は反発の可能性

THB:31.12バーツ/ドル付近で堅調、資金流入が背景。ただし政府の介入リスクあり

CNY:6.91元/ドルへ上昇、関税の主要ターゲットでありながら強含み

EUR:ドイツ・欧州輸出への圧力緩和で回復

JPY:小幅な上昇傾向、日銀の政策次第で変動

関連コンテンツ

「金価格急落 世界市場を揺るがす、しかし新たな積立の黄金チャンスへ!」

11 Jun 2026

アルミニウム価格が急騰!2026年6月 – 過去4年間で最も熱い市場

SO OK TRADING | 2026年6月1日

2026年6月、世界のアルミニウム市場はかつてないほどの 「急騰と供給逼迫」 に直面しています。

ロンドン金属取引所(LME)のアルミニウム先物価格は 1トンあたり 3,675~3,769ドル に達し、2022年以来の最高水準を記録。前年同期比で 50%以上の上昇 となりました。

この歴史的な供給ショックを引き起こしている要因は以下の通りです:

中東紛争:UAEのEGA、バーレーンのALBA大規模製錬所が攻撃を受け、世界供給が8~9%減少

ギニアの輸出制限:世界有数のボーキサイト供給国が輸出規制を開始

中国の生産上限:年間4,550万トンの上限に達し、増産が不可能

エネルギーコスト高騰:原油・天然ガス価格が30%上昇し、製錬コストが急増

LME在庫危機:世界需要をわずか1.5日分しか支えられない低水準

主要金融機関はアルミ価格が高止まりすると予測しています:

モルガン・スタンレー:3,700~3,800ドル(長期化すれば4,000ドル突破の可能性)

世界銀行:3,300~3,600ドル(AI・データセンター需要を反映)

ゴールドマン・サックス:3,150~3,500ドル(市場は供給不足へ)

SO OK TRADING:3,500~3,900ドル

タイ国内では、EV・太陽光・包装業界がコスト上昇に直面する一方、スクラップ価格の上昇や米欧市場への輸出機会が新たなチャンスを生み出しています。

✨ 2026年6月は、アルミニウム市場の転換点。価格高騰、供給不足、そしてタイ輸出企業にとっての戦略的チャンスが交錯する月です。

SO OK TRADING

あなたのビジネスパートナー — FAST • SHARP • RELIABLE

1 Jun 2026

✨ 金は調整・原油は下落・産業金属は急騰:世界市場の転換点 ✨

世界市場は大きな転換期を迎えています!

金:短期的には売り圧力に注意。しかし長期的には新たな積み増しの好機。

原油:和平報道後に急落。明確な下落トレンドへ。

産業金属:力強い反発。世界経済の信頼回復を映し出す。

14 Jun 2026