「硅金属引领未来变革:从石英到人工智能芯片与清洁能源 —— 全球科技的新心脏」 文章作者:SO OK TRADING 日期:2026年4月24日

Last updated: 24 Apr 2026

1805 Views

硅金属2026:驱动世界的新战略材料 文章作者:SO OK TRADING 日期:2026年4月24日

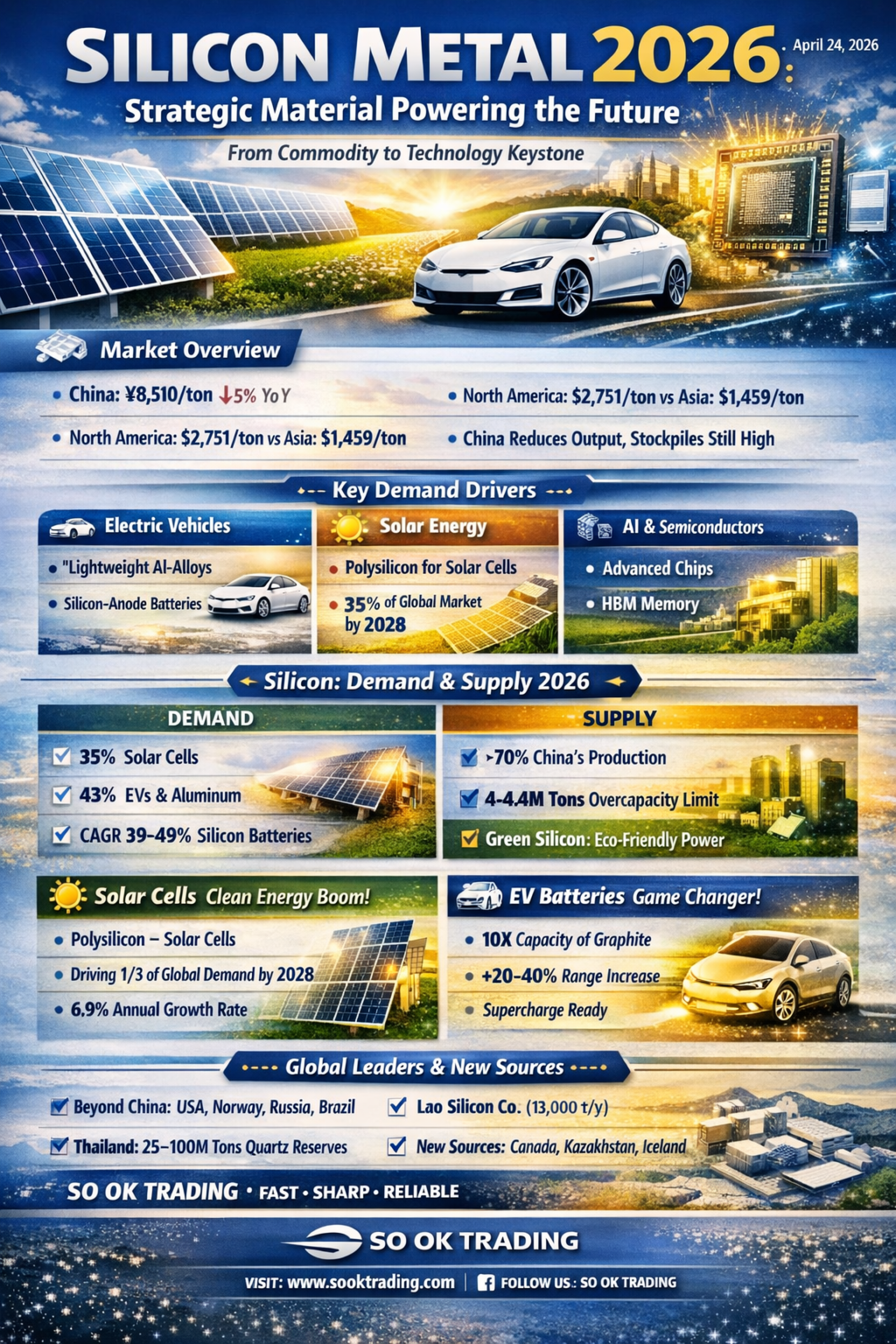

硅金属与硅酮市场在2026年迎来重大转型。 在经历了供过于求和价格低迷之后,今年成为关键转折点——硅金属从“普通原材料”跃升为“全球科技的心脏”。

市场价格与趋势

中国现货价格(#553/#441):8,510元/吨(同比下降约5%)

北美价格:2,751美元/吨 vs 亚洲:1,459美元/吨(因关税与市场保护政策)

中国部分地区减产,但库存仍高,短期内价格难以强劲回升

⚡ 需求驱动力

电动汽车(EV):轻量化铝合金,硅负极电池(容量提升20%以上)

太阳能光伏(Solar PV):多晶硅是太阳能电池的核心,预计到2028年占全球市场35%

人工智能与半导体:高纯度硅是先进芯片与HBM存储的必需材料

SILICON:2026年供需平衡

需求

太阳能电池:约35%

电动汽车与铝合金:约43%

硅电池:CAGR 39–49%,增长最快

供给

中国:仍占全球约80%,实施“防止产能过剩”政策(限制在400–440万吨)

加拿大、挪威、巴西等低成本清洁能源地区成为新生产基地

“绿色硅”市场兴起(利用清洁能源生产,环保低碳)

☀️ 太阳能电池:清洁能源的加速器

高纯度硅 → 多晶硅 → 太阳能电池

到2028年将占全球需求的三分之一

年均增长率(CAGR):6.9%

电动汽车电池:游戏规则改变者

储能能力比石墨高10倍

续航里程提升20–40%

支持超级快充(Supercharge)

挑战:充放电时体积膨胀3–4倍 → 解决方案:硅-石墨复合材料、纳米结构技术

主要玩家:Sila Nanotechnologies、Group14、Enovix,以及保时捷、奔驰、宝马

全球主要生产者与新兴供应源

中国以外:俄罗斯、巴西、挪威、美国、法国、德国

大型企业:Elkem ASA、Ferroglobe、Wacker Chemie、Dow、RIMA、Mississippi Silicon

新兴供应源:哈萨克斯坦、加拿大、冰岛

老挝:Lao Silicon Co., Ltd. 年产13,000吨(水电低成本生产)

泰国:石英储量2,500万–1亿吨(叻丕、罗勇等),供应太阳能与高科技市场

结论

2026年不仅是价格的变化,更是一次真正的转型:硅金属已成为驱动电动汽车、太阳能与人工智能的战略材料。

“硅是未来清洁能源、长续航电动车和智能AI的关键。”

SO OK TRADING 您在全球贸易与创新中的合作伙伴 FAST • SHARP • RELIABLE www.sooktrading.com Facebook: SO OK TRADING

硅金属与硅酮市场在2026年迎来重大转型。 在经历了供过于求和价格低迷之后,今年成为关键转折点——硅金属从“普通原材料”跃升为“全球科技的心脏”。

市场价格与趋势

中国现货价格(#553/#441):8,510元/吨(同比下降约5%)

北美价格:2,751美元/吨 vs 亚洲:1,459美元/吨(因关税与市场保护政策)

中国部分地区减产,但库存仍高,短期内价格难以强劲回升

⚡ 需求驱动力

电动汽车(EV):轻量化铝合金,硅负极电池(容量提升20%以上)

太阳能光伏(Solar PV):多晶硅是太阳能电池的核心,预计到2028年占全球市场35%

人工智能与半导体:高纯度硅是先进芯片与HBM存储的必需材料

SILICON:2026年供需平衡

需求

太阳能电池:约35%

电动汽车与铝合金:约43%

硅电池:CAGR 39–49%,增长最快

供给

中国:仍占全球约80%,实施“防止产能过剩”政策(限制在400–440万吨)

加拿大、挪威、巴西等低成本清洁能源地区成为新生产基地

“绿色硅”市场兴起(利用清洁能源生产,环保低碳)

☀️ 太阳能电池:清洁能源的加速器

高纯度硅 → 多晶硅 → 太阳能电池

到2028年将占全球需求的三分之一

年均增长率(CAGR):6.9%

电动汽车电池:游戏规则改变者

储能能力比石墨高10倍

续航里程提升20–40%

支持超级快充(Supercharge)

挑战:充放电时体积膨胀3–4倍 → 解决方案:硅-石墨复合材料、纳米结构技术

主要玩家:Sila Nanotechnologies、Group14、Enovix,以及保时捷、奔驰、宝马

全球主要生产者与新兴供应源

中国以外:俄罗斯、巴西、挪威、美国、法国、德国

大型企业:Elkem ASA、Ferroglobe、Wacker Chemie、Dow、RIMA、Mississippi Silicon

新兴供应源:哈萨克斯坦、加拿大、冰岛

老挝:Lao Silicon Co., Ltd. 年产13,000吨(水电低成本生产)

泰国:石英储量2,500万–1亿吨(叻丕、罗勇等),供应太阳能与高科技市场

结论

2026年不仅是价格的变化,更是一次真正的转型:硅金属已成为驱动电动汽车、太阳能与人工智能的战略材料。

“硅是未来清洁能源、长续航电动车和智能AI的关键。”

SO OK TRADING 您在全球贸易与创新中的合作伙伴 FAST • SHARP • RELIABLE www.sooktrading.com Facebook: SO OK TRADING

Related Content

」")

RDF-3:水泥厂最爱的废弃物燃料

从垃圾到清洁能源,全球水泥厂——包括泰国在内——正在从昂贵的煤炭转向RDF,以真正实现成本降低和碳减排。

RDF-3(轻质RDF) 是行业明星:体积小、燃烧快、热值高,而且没有残余灰分。

全球趋势:中国、日本、韩国正在迈向更清洁、更稳定的SRF(高品质固体燃料),并引入智能分拣技术。

泰国也不落后:大型水泥厂设定了RDF使用率50–100%的目标,推动“垃圾变水泥”的模式,并制定国家标准(TIS RDF)。

RDF-3不仅仅是“替代燃料”,而是能够真正让水泥厂实现环保的 未来燃料。

15 Mar 2026

2026年泰国产业趋势

泰国产业正在从“追求产量”转向“符合全球趋势的生产”。

能够转型为清洁能源和生物农业的企业,将在出口和融资方面获得巨大优势。

3 Mar 2026