Global Plastic Crisis 2026: Rising Costs as War and Naphtha Shake the Industry

Last updated: 5 Apr 2026

5936 Views

Global Plastic Crisis 2026: How War and Naphtha Shook the Industry

Article by SO OK TRADING | April 5, 2026

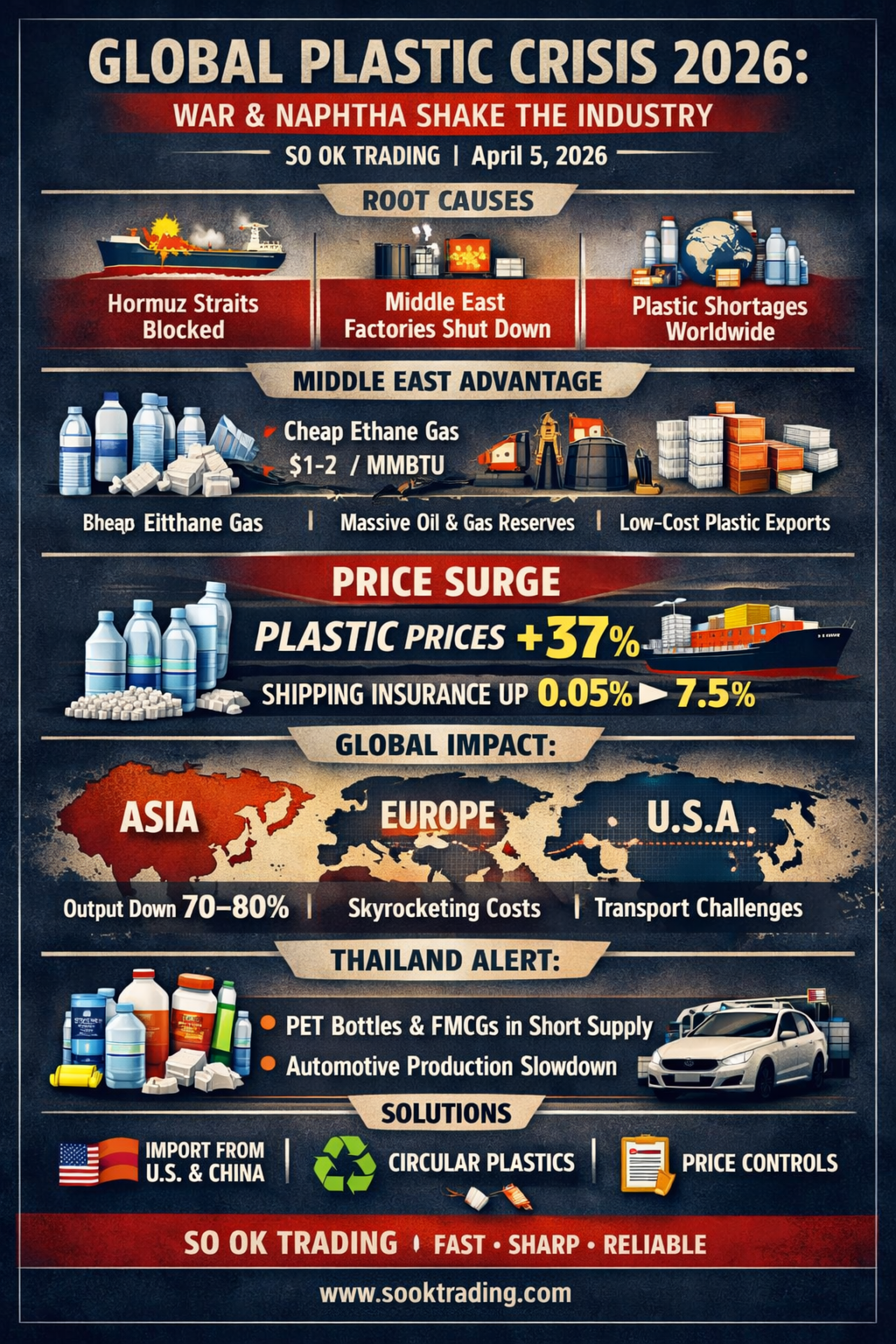

Plastic — once considered a basic raw material of everyday life — has now become a “scarce commodity” shaking the world in April 2026. The Middle East conflict and the global naphtha shortage have delivered a heavy blow to the petrochemical industry, driving plastic prices sharply upward and impacting every sector, from food packaging to automotive components.

Roots of the Crisis

Middle East War: The Hormuz Strait blockade halted over 84% of Polyethylene (PE) export capacity.

Factory Shutdowns: Plants in Iran and neighboring countries ceased operations due to attacks and power shortages.

“Money Can’t Buy It”: Plastic granules disappeared from the market, leaving buyers empty-handed despite soaring prices.

Why the Middle East is the Heart of Plastics

Vast reserves of oil and natural gas

Cheap ethane gas ($1–2/MMBTU) used for plastic production

Heavy investment in midstream industries, making the region the world’s lowest-cost exporter of plastic Yet, once export routes were blocked, shipping and insurance costs skyrocketed, erasing the advantage of low production costs.

Price and Cost Impact

Global plastic prices surged 37–38% in just one month

Shipping insurance jumped from 0.05% to 7.5% of vessel value

Naphtha shortage: Asia and Europe, heavily dependent on naphtha, face costs 5–10 times higher than Middle East ethane-based production

Regional Impact

Asia (Thailand, Japan, South Korea): Petrochemical plants cut output to 70–80%. PET bottles and plastic bags are in severe shortage.

Europe: With Russian imports cut and Middle East supply disrupted, Europe faces the world’s highest plastic prices. Many factories have idled.

United States: Slightly advantaged by ethane use, but still hit by rising transport costs and global volatility.

Thailand’s Situation

Stock Running Out: Experts warn reserves may last only until after Songkran.

Industries Hit Hard:

Food & Beverage Packaging: PET bottles and bags scarce; small producers struggle.

FMCG: Packaging costs rose from 10–15% to nearly 25% of product price; refill packs promoted.

Automotive & Electronics: Engineering-grade plastics short; assembly lines slowed.

Government Measures: “Blue Flag” program to stabilize prices and promote recycled plastics (rPET/rHDPE).

Solutions Moving Forward

Import negotiations with the U.S. and China despite higher transport costs

Circular Plastics: Boosting recycled plastic use to reduce reliance on virgin materials

Price Controls: Ministry of Commerce monitoring to prevent unfair price hikes

Conclusion

This crisis is not just about “rising costs” — it is about “shortages” that are reshaping industries worldwide. Unless the Middle East conflict eases soon, petrochemical recovery may take until the end of 2026, with global production and consumption patterns undergoing dramatic change in the meantime.

SO OK TRADING Your Trusted Business Partner FAST • SHARP • RELIABLE www.sooktrading.com

Article by SO OK TRADING | April 5, 2026

Plastic — once considered a basic raw material of everyday life — has now become a “scarce commodity” shaking the world in April 2026. The Middle East conflict and the global naphtha shortage have delivered a heavy blow to the petrochemical industry, driving plastic prices sharply upward and impacting every sector, from food packaging to automotive components.

Roots of the Crisis

Middle East War: The Hormuz Strait blockade halted over 84% of Polyethylene (PE) export capacity.

Factory Shutdowns: Plants in Iran and neighboring countries ceased operations due to attacks and power shortages.

“Money Can’t Buy It”: Plastic granules disappeared from the market, leaving buyers empty-handed despite soaring prices.

Why the Middle East is the Heart of Plastics

Vast reserves of oil and natural gas

Cheap ethane gas ($1–2/MMBTU) used for plastic production

Heavy investment in midstream industries, making the region the world’s lowest-cost exporter of plastic Yet, once export routes were blocked, shipping and insurance costs skyrocketed, erasing the advantage of low production costs.

Price and Cost Impact

Global plastic prices surged 37–38% in just one month

Shipping insurance jumped from 0.05% to 7.5% of vessel value

Naphtha shortage: Asia and Europe, heavily dependent on naphtha, face costs 5–10 times higher than Middle East ethane-based production

Regional Impact

Asia (Thailand, Japan, South Korea): Petrochemical plants cut output to 70–80%. PET bottles and plastic bags are in severe shortage.

Europe: With Russian imports cut and Middle East supply disrupted, Europe faces the world’s highest plastic prices. Many factories have idled.

United States: Slightly advantaged by ethane use, but still hit by rising transport costs and global volatility.

Thailand’s Situation

Stock Running Out: Experts warn reserves may last only until after Songkran.

Industries Hit Hard:

Food & Beverage Packaging: PET bottles and bags scarce; small producers struggle.

FMCG: Packaging costs rose from 10–15% to nearly 25% of product price; refill packs promoted.

Automotive & Electronics: Engineering-grade plastics short; assembly lines slowed.

Government Measures: “Blue Flag” program to stabilize prices and promote recycled plastics (rPET/rHDPE).

Solutions Moving Forward

Import negotiations with the U.S. and China despite higher transport costs

Circular Plastics: Boosting recycled plastic use to reduce reliance on virgin materials

Price Controls: Ministry of Commerce monitoring to prevent unfair price hikes

Conclusion

This crisis is not just about “rising costs” — it is about “shortages” that are reshaping industries worldwide. Unless the Middle East conflict eases soon, petrochemical recovery may take until the end of 2026, with global production and consumption patterns undergoing dramatic change in the meantime.

SO OK TRADING Your Trusted Business Partner FAST • SHARP • RELIABLE www.sooktrading.com

Related Content

Global Steel Market 2026: Surging Costs Drive Prices Up 10–15%

April 2026 marks a turning point for the global steel industry — a fragile recovery amid soaring raw material and energy costs.

Iron ore averages $90–95 per ton, coking coal $170–190, and carbon tariffs under the EU’s CBAM add another $60–90 per ton, pushing global steel prices higher by 10–15%.

20 Apr 2026

Strong Dollar – U.S. Resilient, China Steadies, Global Pressures Mount, Thailand Faces Dual Impacts

Global Economic Analysis by SO OK TRADING | June 19, 2026

The U.S. dollar continues to strengthen, reflecting the resilience of the American economy which has grown beyond expectations. Meanwhile, China is striving to stabilize its economy through stimulus measures and accommodative monetary policies. The global economy as a whole remains under pressure from rising energy costs and geopolitical uncertainties.

For Thailand, the baht remains on a weakening trend, creating a dual impact: on the one hand, boosting export revenues and tourism inflows; on the other, increasing the burden of higher costs for importers and domestic consumers.

This article explores the global economic landscape with a focus on the U.S., China, and Thailand, while providing insights into the currency outlook for July and risk management strategies that Thai businesses should closely monitor.

✨ SO OK TRADING

Your Trusted Business Partner

FAST • SHARP • RELIABLE

19 Jun 2026

Gold Consolidation: Still a Long-Term Game to Watch

After hitting record highs earlier this year, global gold prices (Gold Spot) are now consolidating within the $4,610 – $4,700 per ounce range. Meanwhile, domestic gold (96.5%) has dropped sharply to 71,100 – 71,750 THB, pressured by a stronger Thai baht.

Despite short-term profit-taking and dollar strength, gold continues to be supported by geopolitical tensions and ongoing central bank purchases, which help sustain its long-term appeal.

15 May 2026