グリーンランド2026:資源の宝庫と地政学・経済の重要国 SO OK TRADING 要約

Last updated: 22 Jan 2026

1976 Views

グリーンランド 2026:北極の戦略的宝庫

SO OK TRADING インサイト

グリーンランド – 遠隔の島から世界戦略拠点へ

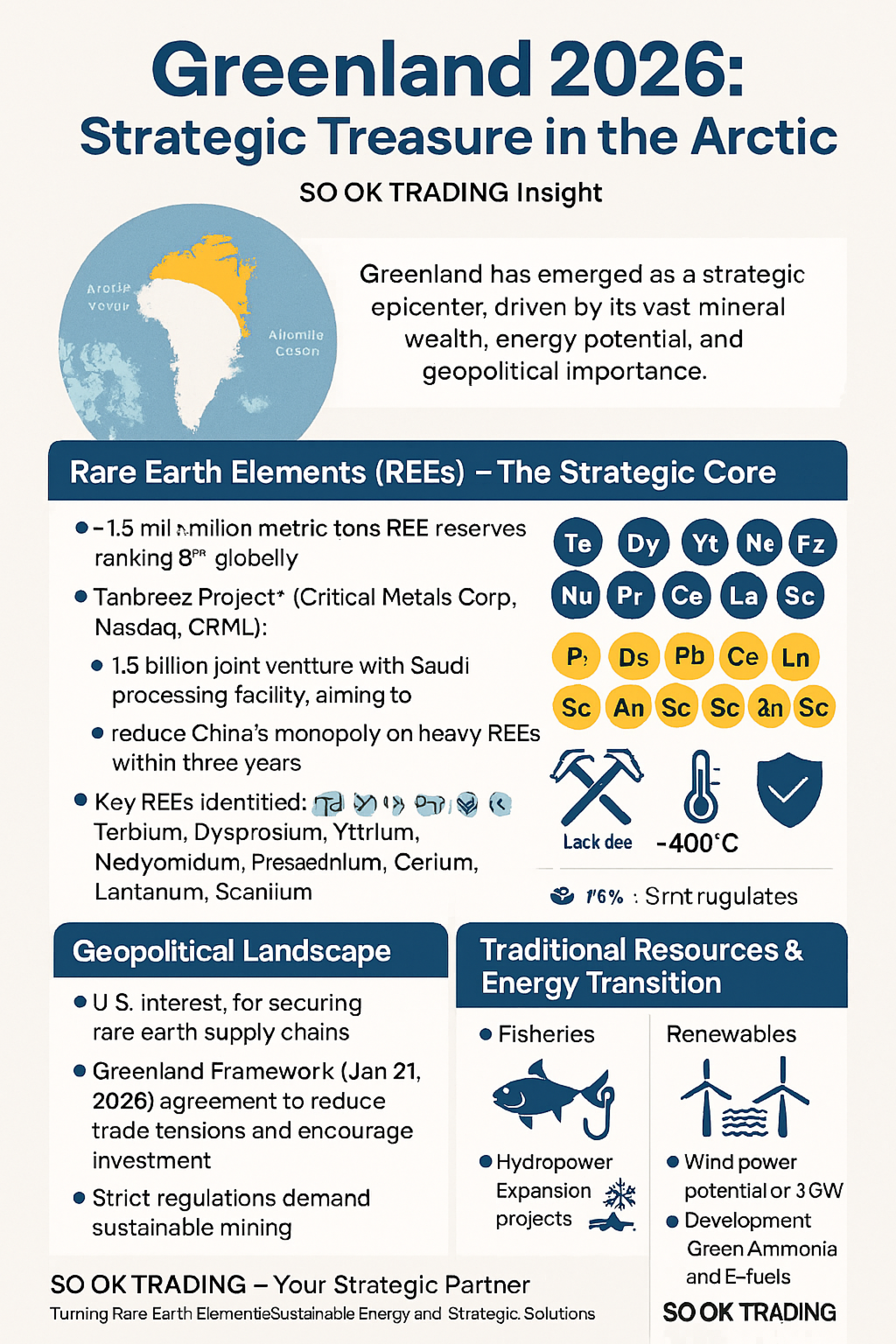

世界最大の島であるグリーンランドは、2026年に戦略的拠点として台頭しました。膨大な鉱物資源、エネルギーの可能性、そして地政学的な重要性が、クリーンテクノロジーと先端産業のための世界的なサプライチェーンを再構築しています。

主要ハイライト

レアアース(Rare Earth Elements – REEs)

グリーンランドは約 150万トン のレアアース埋蔵量を持ち、世界第8位。

Tanbreez プロジェクト(Critical Metals Corp, Nasdaq: CRML):

2026年1月にパイロットプラント建設開始、5月に稼働予定。

サウジアラビア産業グループとの15億ドル規模の合弁事業により、大規模な加工施設を建設。米国防衛産業やEV産業へ供給。

2027年に本格生産開始予定。中国による重希土類の独占(97%)を3年以内に約50%まで削減する目標。

Kvanefjeld プロジェクト: ウラン採掘禁止法により停滞。Energy Transition Minerals社との法的紛争が進行中。

主要なREEs: テルビウム、ジスプロシウム、イットリウム、ネオジム、プラセオジム、セリウム、ランタン、スカンジウム。

その他の戦略鉱物

グラファイト(電池用)、モリブデン、亜鉛、銅、ニッケル、チタン。

ジルコニウム、ニオブ、タンタル、ガリウム、ハフニウム – 半導体、航空宇宙、原子力産業に不可欠。

鉱業とインフラの課題

現在稼働中の鉱山は 2か所のみ:南部の金鉱山、西部カンゲルルススアークのアノーソサイト鉱山。

厳しい気候(-40°C)、港湾・道路・発電所の不足により、コストは他地域の2~3倍。

環境規制が厳しく、持続可能な採掘が必須。

地政学的状況

米国: レアアース供給網の安全保障に不可欠と認識。

Greenland Framework(2026年1月21日): 貿易摩擦を緩和し、持続可能な投資を促進する新協定。

世界的競争: 中国、米国、EU、中東諸国が資源アクセスを競合。

伝統的資源とエネルギー転換

漁業: 輸出の90%以上を占め、地域経済の基盤。

石油・ガス: 推定埋蔵量は原油175億バレル。環境規制により探査は限定的。

再生可能エネルギー:

水力発電:すでに電力の70%を供給。Buksefjord、Aasiaat、Qasigiannguitで拡張計画進行中。

風力発電:3GWの潜在能力。将来的に欧州・米国へ海底ケーブルで輸出予定。

グリーンアンモニア、E燃料:次世代クリーン燃料として開発中。

「北極の10年」におけるグリーンランド

2026年、グリーンランドは次の役割へ変貌:

クリーンテクノロジー供給網の戦略的パートナー – 中国依存を削減。

北極物流ハブ – 新国際空港3か所(ヌーク、イルリサット、カコルトーク)により輸送コスト削減、エコツーリズム促進。

世界的クリーンエネルギー生産者 – 水力、風力、グリーン水素、グリーンアンモニアを輸出。

地政学的ピボット – 資源利用と持続可能性・主権のバランスを実現。

SO OK TRADING – あなたの戦略的パートナー

グリーンランドが世界資源の中心となる中、SO OK TRADING は以下を提供します:

高品質レアアース供給: ネオジム、ジスプロシウムなど信頼できる供給源から。

統合型クリーンエネルギーソリューション: ソーラー+蓄電ESS、磁気システム、産業用エネルギーインフラ。

ニーズに合わせたカスタマイズ: 住宅、オフィス、工場まで幅広く対応。

国際的信頼性: 世界的ブランドとの提携と国際基準の遵守。

SO OK TRADING – レアアースを持続可能なエネルギーと戦略的ソリューションへ

今すぐご相談いただき、最適なパッケージで未来の産業を共に築きましょう。

Mongkol、この日本語版をさらに プレスリリース用の短縮版 や インフォグラフィック用キャッチコピー に整えることも可能です ✨

SO OK TRADING インサイト

グリーンランド – 遠隔の島から世界戦略拠点へ

世界最大の島であるグリーンランドは、2026年に戦略的拠点として台頭しました。膨大な鉱物資源、エネルギーの可能性、そして地政学的な重要性が、クリーンテクノロジーと先端産業のための世界的なサプライチェーンを再構築しています。

主要ハイライト

レアアース(Rare Earth Elements – REEs)

グリーンランドは約 150万トン のレアアース埋蔵量を持ち、世界第8位。

Tanbreez プロジェクト(Critical Metals Corp, Nasdaq: CRML):

2026年1月にパイロットプラント建設開始、5月に稼働予定。

サウジアラビア産業グループとの15億ドル規模の合弁事業により、大規模な加工施設を建設。米国防衛産業やEV産業へ供給。

2027年に本格生産開始予定。中国による重希土類の独占(97%)を3年以内に約50%まで削減する目標。

Kvanefjeld プロジェクト: ウラン採掘禁止法により停滞。Energy Transition Minerals社との法的紛争が進行中。

主要なREEs: テルビウム、ジスプロシウム、イットリウム、ネオジム、プラセオジム、セリウム、ランタン、スカンジウム。

その他の戦略鉱物

グラファイト(電池用)、モリブデン、亜鉛、銅、ニッケル、チタン。

ジルコニウム、ニオブ、タンタル、ガリウム、ハフニウム – 半導体、航空宇宙、原子力産業に不可欠。

鉱業とインフラの課題

現在稼働中の鉱山は 2か所のみ:南部の金鉱山、西部カンゲルルススアークのアノーソサイト鉱山。

厳しい気候(-40°C)、港湾・道路・発電所の不足により、コストは他地域の2~3倍。

環境規制が厳しく、持続可能な採掘が必須。

地政学的状況

米国: レアアース供給網の安全保障に不可欠と認識。

Greenland Framework(2026年1月21日): 貿易摩擦を緩和し、持続可能な投資を促進する新協定。

世界的競争: 中国、米国、EU、中東諸国が資源アクセスを競合。

伝統的資源とエネルギー転換

漁業: 輸出の90%以上を占め、地域経済の基盤。

石油・ガス: 推定埋蔵量は原油175億バレル。環境規制により探査は限定的。

再生可能エネルギー:

水力発電:すでに電力の70%を供給。Buksefjord、Aasiaat、Qasigiannguitで拡張計画進行中。

風力発電:3GWの潜在能力。将来的に欧州・米国へ海底ケーブルで輸出予定。

グリーンアンモニア、E燃料:次世代クリーン燃料として開発中。

「北極の10年」におけるグリーンランド

2026年、グリーンランドは次の役割へ変貌:

クリーンテクノロジー供給網の戦略的パートナー – 中国依存を削減。

北極物流ハブ – 新国際空港3か所(ヌーク、イルリサット、カコルトーク)により輸送コスト削減、エコツーリズム促進。

世界的クリーンエネルギー生産者 – 水力、風力、グリーン水素、グリーンアンモニアを輸出。

地政学的ピボット – 資源利用と持続可能性・主権のバランスを実現。

SO OK TRADING – あなたの戦略的パートナー

グリーンランドが世界資源の中心となる中、SO OK TRADING は以下を提供します:

高品質レアアース供給: ネオジム、ジスプロシウムなど信頼できる供給源から。

統合型クリーンエネルギーソリューション: ソーラー+蓄電ESS、磁気システム、産業用エネルギーインフラ。

ニーズに合わせたカスタマイズ: 住宅、オフィス、工場まで幅広く対応。

国際的信頼性: 世界的ブランドとの提携と国際基準の遵守。

SO OK TRADING – レアアースを持続可能なエネルギーと戦略的ソリューションへ

今すぐご相談いただき、最適なパッケージで未来の産業を共に築きましょう。

Mongkol、この日本語版をさらに プレスリリース用の短縮版 や インフォグラフィック用キャッチコピー に整えることも可能です ✨

関連コンテンツ

2026年原油価格危機:タイに大波、世界経済に停滞のリスク

18 Mar 2026

An analysis of the aluminum market in 2026 indicates a likely continued market deficit and upward price pressure, driven by constrained supply and resilient demand from green energy sectors. However, significant volatility is expected due to policy uncertainties and the potential for new Indonesian supply to eventually balance the market.

Key Drivers and Projections for 2026

Supply Side Analysis

Capacity Constraints: China's primary aluminum output is approaching its self-imposed 45 million-tonne capacity cap, limiting global supply growth.

Power Challenges: Smelters outside of China face intense competition for power from energy-intensive sectors like AI data centers, which are willing to pay higher prices for long-term contracts. This has kept significant capacity offline in Europe and the US.

Production Disruptions: Outages and potential shutdowns at existing smelters in Iceland and Mozambique further tighten the market.

Scrap Supply Pressure: The EU's planned implementation of the Carbon Border Adjustment Mechanism (CBAM) and potential scrap export tariffs in spring 2026 are expected to impact global scrap flows, creating regional shortages and price volatility.

New Capacity: Indonesia is a key source of new supply, with several projects in the pipeline. However, analysts suggest the pace of the ramp-up may be slower than expected due to infrastructure and policy challenges, meaning it is unlikely to fully offset near-term tightness.

Demand Side Analysis

Green Transition Demand: Demand from "green" sectors such as solar panels, new energy vehicles, and energy transition infrastructure remains strong, providing fundamental support for the market.

Substitution Effect: Aluminum's wide price discount relative to copper has encouraged substitution in electrical applications, acting as a tailwind for demand and prices.

Construction and Automotive: The construction and automotive industries continue to be major consumers, with growing demand for lightweight, low-carbon aluminum products.

Price Forecasts and Volatility

The market is expected to remain in a deficit in 2026, with estimates ranging from 200,000 to 600,000 tonnes. This structural tightness is leading most analysts to forecast sustained or rising prices.

Bullish Views: Analysts at Bank of America project prices of $3,000/tonne as early as 2026. J.P. Morgan also expects prices to approach $3,000/tonne in Q1 2026. ING forecasts an average price of $2,900/tonne for the year.

Bearish/Conservative Views: Goldman Sachs is an outlier, forecasting prices to decline to $2,350/tonne by Q4 2026, anticipating a market surplus later in the year. SMM forecasts a "high first, then lower" pattern, with prices finding equilibrium in the $2,700–$2,800/tonne range by year-end.

Premiums: Regional premiums, particularly the US Midwest premium, are expected to remain high and volatile due to tariffs and regional supply dynamics, creating a disconnect from the LME benchmark price.

In essence, 2026 is projected to be a year of high volatility where participants need to focus on scenario readiness rather than relying on a single price forecast, as geopolitical and energy policies significantly influence regional supply and costs

31 Dec 2025

SO OK TRADING は 2,000,000 人の訪問者を誇りを持って祝います!

タイから世界へ、私たちは常に 速く、鋭く、そして信頼できる 企業として歩み続け、信頼と成功を生み出すグローバルなパートナーシップを築いています

29 Jun 2026