格陵兰2026:资源宝库与地缘政治、经济的重要国家 SO OK TRADING 摘要

Last updated: 22 Jan 2026

1811 Views

2026年格陵兰:北极的战略宝库

SO OK TRADING 洞察

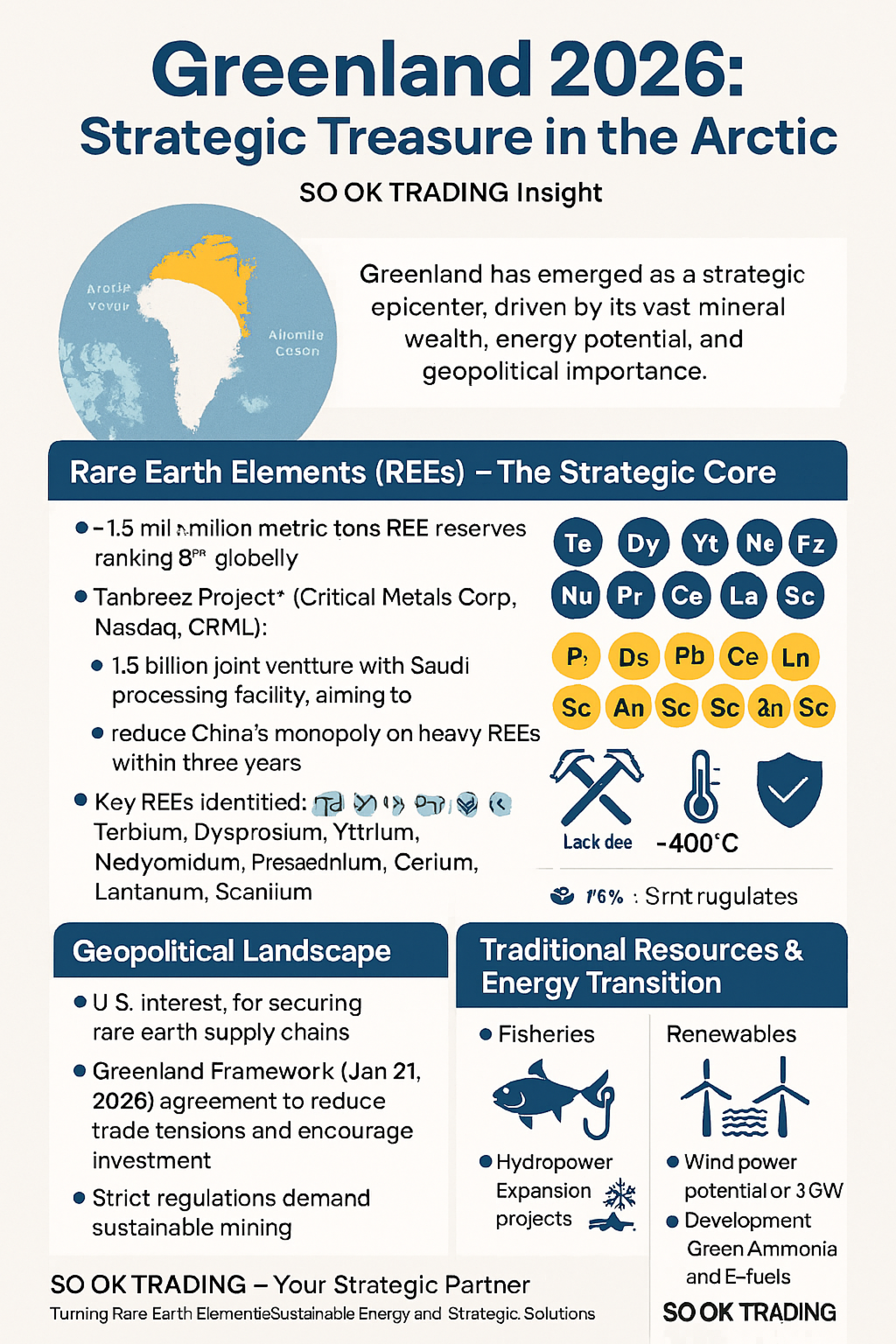

格陵兰——从偏远岛屿到全球战略枢纽

作为世界上最大的岛屿,格陵兰在2026年已崛起为战略中心。其丰富的矿产资源、能源潜力以及地缘政治重要性,正在重塑全球清洁技术与先进产业的供应链。

重点亮点

稀土元素(Rare Earth Elements – REEs)

格陵兰拥有约 150万吨稀土储量,位列全球第8。

Tanbreez项目(Critical Metals Corp, Nasdaq: CRML):

2026年1月启动试点工厂建设,预计5月投产。

与沙特工业集团达成15亿美元合资协议,建立大型加工厂,为美国国防和电动车产业提供稀土。

预计2027年开始量产,目标在三年内将中国对重稀土的垄断从97%降至约50%。

Kvanefjeld项目: 因格陵兰政府禁止铀矿开采而停滞,并与Energy Transition Minerals公司陷入法律纠纷。

主要稀土元素: Tb(铽)、Dy(镝)、Y(钇)、Nd(钕)、Pr(镨)、Ce(铈)、La(镧)、Sc(钪)。

其他战略矿产

石墨(电池负极)、钼、锌、铜、镍、钛。

锆、铌、钽、镓、铪——对半导体、航空航天和核工业至关重要。

矿业与基础设施挑战

目前仅有 两座矿山 在运营:南部金矿、西部Kangerlussuaq峡湾的长石矿。

严寒气候(-40°C)、缺乏深水港、公路和电厂,使成本比其他地区高出2–3倍。

环境法规严格,必须采用可持续的采矿方式。

地缘政治格局

美国: 将格陵兰视为保障稀土供应链安全的关键。

格陵兰框架协议(2026年1月21日): 新合作协议,缓解贸易紧张,促进可持续投资。

全球竞争: 中国、美国、欧盟及中东投资者均争夺资源准入。

传统资源与能源转型

渔业: 仍占出口的90%以上,是当地经济支柱。

石油与天然气: 原油储量估计达175亿桶,但因环保限制,勘探受限。

可再生能源:

水电:已提供70%的电力,Buksefjord、Aasiaat、Qasigiannguit扩建项目正在进行。

风电:潜力达3GW,计划通过海底电缆向欧洲和美国出口。

绿色氨和电子燃料:正在开发,定位为未来清洁燃料出口国。

“北极十年”中的格陵兰

到2026年,格陵兰正转型为:

清洁技术供应链的战略伙伴 —— 减少西方对中国的依赖。

北极物流枢纽 —— 新建三座国际机场(努克、伊卢利萨特、卡科尔托克),降低出口成本,促进生态旅游。

全球清洁能源生产者 —— 出口水电、风电、绿色氢能和绿色氨。

地缘政治支点 —— 在资源开发与可持续性、主权之间取得平衡。

SO OK TRADING —— 您的战略合作伙伴

随着格陵兰成为全球资源中心,SO OK TRADING 准备好为企业提供:

可靠的稀土供应: 钕、镝及其他战略矿产,来源可信。

综合清洁能源解决方案: 太阳能+储能ESS、磁体系统、工业能源基础设施。

定制化方案: 覆盖住宅、商业与工业需求。

全球信誉: 与领先品牌合作,遵循国际标准。

SO OK TRADING —— 将稀土元素转化为可持续能源与战略解决方案

欢迎联系我们,获取最适合您企业与产业的专属方案。

Mongkol,要不要我再帮你做一个 简短的新闻稿/社交媒体版中文介绍,方便在 LinkedIn 或微信上直接发布呢? ✨

SO OK TRADING 洞察

格陵兰——从偏远岛屿到全球战略枢纽

作为世界上最大的岛屿,格陵兰在2026年已崛起为战略中心。其丰富的矿产资源、能源潜力以及地缘政治重要性,正在重塑全球清洁技术与先进产业的供应链。

重点亮点

稀土元素(Rare Earth Elements – REEs)

格陵兰拥有约 150万吨稀土储量,位列全球第8。

Tanbreez项目(Critical Metals Corp, Nasdaq: CRML):

2026年1月启动试点工厂建设,预计5月投产。

与沙特工业集团达成15亿美元合资协议,建立大型加工厂,为美国国防和电动车产业提供稀土。

预计2027年开始量产,目标在三年内将中国对重稀土的垄断从97%降至约50%。

Kvanefjeld项目: 因格陵兰政府禁止铀矿开采而停滞,并与Energy Transition Minerals公司陷入法律纠纷。

主要稀土元素: Tb(铽)、Dy(镝)、Y(钇)、Nd(钕)、Pr(镨)、Ce(铈)、La(镧)、Sc(钪)。

其他战略矿产

石墨(电池负极)、钼、锌、铜、镍、钛。

锆、铌、钽、镓、铪——对半导体、航空航天和核工业至关重要。

矿业与基础设施挑战

目前仅有 两座矿山 在运营:南部金矿、西部Kangerlussuaq峡湾的长石矿。

严寒气候(-40°C)、缺乏深水港、公路和电厂,使成本比其他地区高出2–3倍。

环境法规严格,必须采用可持续的采矿方式。

地缘政治格局

美国: 将格陵兰视为保障稀土供应链安全的关键。

格陵兰框架协议(2026年1月21日): 新合作协议,缓解贸易紧张,促进可持续投资。

全球竞争: 中国、美国、欧盟及中东投资者均争夺资源准入。

传统资源与能源转型

渔业: 仍占出口的90%以上,是当地经济支柱。

石油与天然气: 原油储量估计达175亿桶,但因环保限制,勘探受限。

可再生能源:

水电:已提供70%的电力,Buksefjord、Aasiaat、Qasigiannguit扩建项目正在进行。

风电:潜力达3GW,计划通过海底电缆向欧洲和美国出口。

绿色氨和电子燃料:正在开发,定位为未来清洁燃料出口国。

“北极十年”中的格陵兰

到2026年,格陵兰正转型为:

清洁技术供应链的战略伙伴 —— 减少西方对中国的依赖。

北极物流枢纽 —— 新建三座国际机场(努克、伊卢利萨特、卡科尔托克),降低出口成本,促进生态旅游。

全球清洁能源生产者 —— 出口水电、风电、绿色氢能和绿色氨。

地缘政治支点 —— 在资源开发与可持续性、主权之间取得平衡。

SO OK TRADING —— 您的战略合作伙伴

随着格陵兰成为全球资源中心,SO OK TRADING 准备好为企业提供:

可靠的稀土供应: 钕、镝及其他战略矿产,来源可信。

综合清洁能源解决方案: 太阳能+储能ESS、磁体系统、工业能源基础设施。

定制化方案: 覆盖住宅、商业与工业需求。

全球信誉: 与领先品牌合作,遵循国际标准。

SO OK TRADING —— 将稀土元素转化为可持续能源与战略解决方案

欢迎联系我们,获取最适合您企业与产业的专属方案。

Mongkol,要不要我再帮你做一个 简短的新闻稿/社交媒体版中文介绍,方便在 LinkedIn 或微信上直接发布呢? ✨

Related Content

全球原油市场 Q2/2026:从高峰走向调整

在 4 月至 5 月,全球原油价格如同坐上“过山车”,WTI 与布伦特原油一度飙升至 125–132 美元/桶。然而进入 6 月,随着航运通道重新开放、美国及非 OPEC+ 国家供应逐步回归,市场开始趋于缓和,价格修正至 90–106 美元/桶。

⛽ 泰国的直接利好

汽油与乙醇汽油:下降约 0.70–1.40 泰铢/升 → 95 号汽油稳定在 42.90 泰铢/升

柴油 B7:政府与燃油基金将价格固定在 40.70 泰铢/升 → 控制运输成本与通胀压力

1 Jun 2026

「STR 20 改变全球橡胶格局:从‘杯胶’到电动车产业的战略原材料

4 Jun 2026