黄金市场大逆转——机会还是风险 : Article By SO OK TRADING

Last updated: 3 Feb 2026

2756 Views

黄金市场动向概览(2026年1月末至2月初)

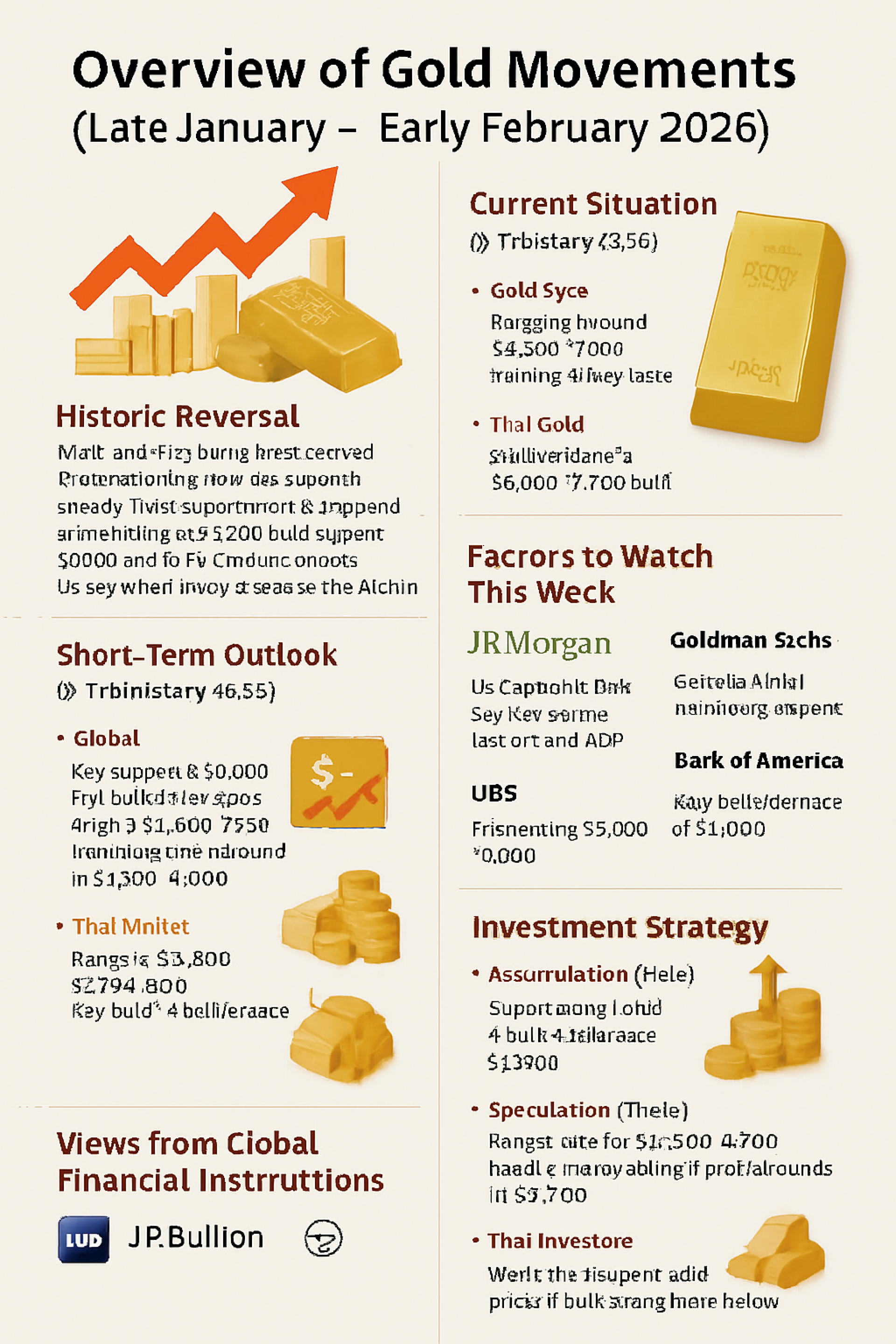

全球黄金市场刚刚经历了数十年来最大的一次 历史性反转 (Historic Reversal)。在1月末,金价首次突破每盎司 5,500美元,泰国黄金价格也飙升至 80,000泰铢 的历史新高。

然而仅仅几天之后,大型机构和基金的获利了结抛售潮汹涌而至,全球金价在不到一周的时间里急跌 800–900美元,泰国金价也下跌超过 10,000泰铢。不过,由于泰铢贬值至 31.60–32.00泰铢/美元 区间,国内金价的跌幅没有全球市场那么剧烈。

最新情况(2026年2月3日)

全球金价(Gold Spot):4,664–4,700美元/盎司

泰国黄金(96.5%金条):70,000–71,000泰铢

短期走势展望(2月3日–10日)

全球市场:

当前处于“蓄势”阶段。关键支撑位在 4,600美元,若跌破可能下探 4,400–4,550美元。若企稳并反弹,首个目标为 4,900–5,000美元。

泰国市场:

预计在 69,500–72,500泰铢 区间波动。若泰铢升值至 31.50泰铢/美元 以下,国内金价可能进一步走低。

本周需关注的因素

美国非农就业数据 (NFP) 与 ADP就业报告

高位后的获利了结卖压

美联储 (Fed) 的利率与通胀政策

中东地区的地缘政治紧张局势

全球金融机构观点

摩根大通 (J.P. Morgan): 预计年底目标 6,300美元,认为此次下跌只是市场过度投机后的调整。

高盛 (Goldman Sachs): 目标 4,900–5,400美元,强调各国央行持续买入黄金。

瑞银 (UBS): 预测 5,400–6,200美元,供应不足与地缘政治风险可能推高价格。

美国银行 (Bank of America): 预计全年平均价格约 5,000美元。

泰国分析师观点

YLG Bullion: 认为黄金仍有上涨空间,目标 4,900美元,但提醒2月波动性极高。

SO OK TRADING: 预计2月金价在 4,500–5,250美元/盎司 区间波动,均值约 5,000美元。泰国黄金价格预计在 70,000–76,000泰铢,均值约 73,500泰铢,但需密切关注汇率变化。

投资策略(SO OK TRADING总结)

长期持有: 若金价稳于 4,600美元 以上,是加仓的良机。

短线交易: 在 4,600–4,900美元 区间操作,但若逼近 5,000美元,需警惕强烈的抛压。

泰国投资者: 若泰铢升值至 31.50泰铢/美元 以下,是在国内低价买入黄金的机会。

总结

黄金市场在1月的急涨后进入了大幅调整阶段。短期内波动性依然很高,但中长期仍被全球金融机构普遍看好。对于长期投资者而言,这是一个逐步加仓的机会;而短线交易者则需谨慎应对可能出现的强烈卖压。

全球黄金市场刚刚经历了数十年来最大的一次 历史性反转 (Historic Reversal)。在1月末,金价首次突破每盎司 5,500美元,泰国黄金价格也飙升至 80,000泰铢 的历史新高。

然而仅仅几天之后,大型机构和基金的获利了结抛售潮汹涌而至,全球金价在不到一周的时间里急跌 800–900美元,泰国金价也下跌超过 10,000泰铢。不过,由于泰铢贬值至 31.60–32.00泰铢/美元 区间,国内金价的跌幅没有全球市场那么剧烈。

最新情况(2026年2月3日)

全球金价(Gold Spot):4,664–4,700美元/盎司

泰国黄金(96.5%金条):70,000–71,000泰铢

短期走势展望(2月3日–10日)

全球市场:

当前处于“蓄势”阶段。关键支撑位在 4,600美元,若跌破可能下探 4,400–4,550美元。若企稳并反弹,首个目标为 4,900–5,000美元。

泰国市场:

预计在 69,500–72,500泰铢 区间波动。若泰铢升值至 31.50泰铢/美元 以下,国内金价可能进一步走低。

本周需关注的因素

美国非农就业数据 (NFP) 与 ADP就业报告

高位后的获利了结卖压

美联储 (Fed) 的利率与通胀政策

中东地区的地缘政治紧张局势

全球金融机构观点

摩根大通 (J.P. Morgan): 预计年底目标 6,300美元,认为此次下跌只是市场过度投机后的调整。

高盛 (Goldman Sachs): 目标 4,900–5,400美元,强调各国央行持续买入黄金。

瑞银 (UBS): 预测 5,400–6,200美元,供应不足与地缘政治风险可能推高价格。

美国银行 (Bank of America): 预计全年平均价格约 5,000美元。

泰国分析师观点

YLG Bullion: 认为黄金仍有上涨空间,目标 4,900美元,但提醒2月波动性极高。

SO OK TRADING: 预计2月金价在 4,500–5,250美元/盎司 区间波动,均值约 5,000美元。泰国黄金价格预计在 70,000–76,000泰铢,均值约 73,500泰铢,但需密切关注汇率变化。

投资策略(SO OK TRADING总结)

长期持有: 若金价稳于 4,600美元 以上,是加仓的良机。

短线交易: 在 4,600–4,900美元 区间操作,但若逼近 5,000美元,需警惕强烈的抛压。

泰国投资者: 若泰铢升值至 31.50泰铢/美元 以下,是在国内低价买入黄金的机会。

总结

黄金市场在1月的急涨后进入了大幅调整阶段。短期内波动性依然很高,但中长期仍被全球金融机构普遍看好。对于长期投资者而言,这是一个逐步加仓的机会;而短线交易者则需谨慎应对可能出现的强烈卖压。

Related Content

铜板:战略性原材料与2026年全球铜价展望

来自 SO OK TRADING

2026年,铜从普通的大宗商品升级为“战略性资产”。随着人工智能(AI)、电动汽车(EV)以及清洁能源的快速发展,铜的需求达到前所未有的高度,价格突破每吨 13,000 美元,创下历史新高。

在供应方面,全球市场正面临严重短缺,预计缺口约 15万至33万吨。主要原因包括印尼、智利和刚果的大型矿山停产,以及新矿开发的延迟。

SO OK TRADING 专注于提供高品质的铜板(阴极铜 99.99%),广泛应用于:

- 电动汽车用母排(EV Busbars)

- 印刷电路板(PCB)

- 热交换器(Heat Exchangers)

- 配电柜与开关板(Switchboards)

- 高端建筑装饰材料

26 Jan 2026