锡:从普通金属到战略资源 —— 连接人工智能与清洁能源的未来之胶

Last updated: 27 Feb 2026

2234 Views

✨ 锡:从普通金属到“未来之金属” ✨

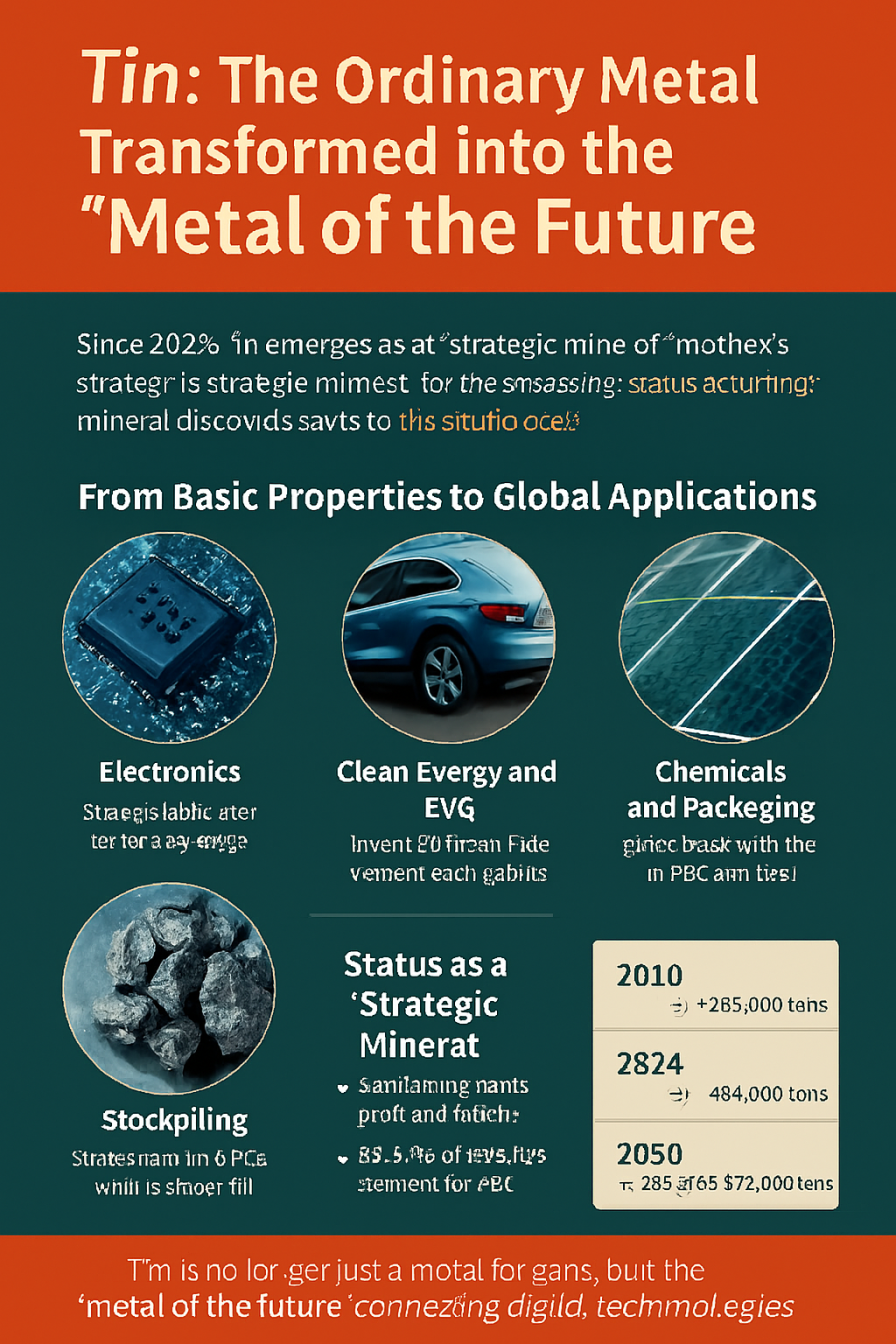

曾经,锡(Sn)只是用于涂覆罐头的材料。

但在2026年,世界开始将其视为 战略资源,它正在重塑数字经济与清洁能源的格局。

从基本特性到全球应用

锡柔软易加工,熔点低,耐腐蚀。

因此,它被广泛应用于食品工业的金属涂层,以及电子电路的焊接。

目前全球主要用途分为三大类:

电子产业:占全球需求的50%以上,是智能手机、AI芯片和5G设备的“胶水”。

清洁能源与电动车:电动车使用的锡是燃油车的2–3倍,应用于电池和太阳能电池板。

化工与包装:仍然重要,用于PVC、牙膏、玻璃和食品包装。

价格飙升与需求驱动

2026年2月,锡的国际价格飙升至 53,698美元/吨(约190万元人民币),同比上涨65%。

主要原因是半导体和电动车产业需求激增,同时印尼和缅甸的供应紧张。

AI时代的锡

锡成为数字世界的“胶水”:

先进封装:AI芯片和GPU需要高密度锡焊点。

数据中心:为AI扩展的服务器和网络设备带来巨大的锡需求。

下一代电池创新

锡不仅是焊料,还正在成为电池阳极材料:

锂离子+硅阳极:添加2%的锡可提升容量并加快充电速度。

钠离子电池:解决低能量密度问题,降低清洁能源储能成本。

太阳能焊带:预计到2030年需求将翻倍。

战略资源地位

战略储备:大国已将锡纳入战略矿产储备。

回收利用:电子废料回收预计可满足市场需求的20–25%。

成长轨迹

2010年:约35万吨

2024年:49.5万吨(5G与电动车推动)

2030年:42–57万吨(预测)

2040年:70万吨以上(AI与清洁能源黄金期)

锡资源与挑战

目前已探明的储量约 430–490万吨:

中国(15%):最大储量与消费国

印尼(17%):世界最重要的海底矿床

缅甸:高品位矿石逐渐减少

巴西与澳大利亚:具备新矿开发潜力

2040年的主要玩家:中国、印尼、非洲(刚果/尼日利亚)、欧洲、澳大利亚。

真正的挑战不是“储量不足”,而是“生产困难”。高品位矿石枯竭,低品位矿石开采需要更高成本和复杂技术。

结论

锡已不再是普通的基础金属。

它是连接 AI、电动车与清洁能源的未来战略资源,将在未来20年决定全球经济的走向。

曾经,锡(Sn)只是用于涂覆罐头的材料。

但在2026年,世界开始将其视为 战略资源,它正在重塑数字经济与清洁能源的格局。

从基本特性到全球应用

锡柔软易加工,熔点低,耐腐蚀。

因此,它被广泛应用于食品工业的金属涂层,以及电子电路的焊接。

目前全球主要用途分为三大类:

电子产业:占全球需求的50%以上,是智能手机、AI芯片和5G设备的“胶水”。

清洁能源与电动车:电动车使用的锡是燃油车的2–3倍,应用于电池和太阳能电池板。

化工与包装:仍然重要,用于PVC、牙膏、玻璃和食品包装。

价格飙升与需求驱动

2026年2月,锡的国际价格飙升至 53,698美元/吨(约190万元人民币),同比上涨65%。

主要原因是半导体和电动车产业需求激增,同时印尼和缅甸的供应紧张。

AI时代的锡

锡成为数字世界的“胶水”:

先进封装:AI芯片和GPU需要高密度锡焊点。

数据中心:为AI扩展的服务器和网络设备带来巨大的锡需求。

下一代电池创新

锡不仅是焊料,还正在成为电池阳极材料:

锂离子+硅阳极:添加2%的锡可提升容量并加快充电速度。

钠离子电池:解决低能量密度问题,降低清洁能源储能成本。

太阳能焊带:预计到2030年需求将翻倍。

战略资源地位

战略储备:大国已将锡纳入战略矿产储备。

回收利用:电子废料回收预计可满足市场需求的20–25%。

成长轨迹

2010年:约35万吨

2024年:49.5万吨(5G与电动车推动)

2030年:42–57万吨(预测)

2040年:70万吨以上(AI与清洁能源黄金期)

锡资源与挑战

目前已探明的储量约 430–490万吨:

中国(15%):最大储量与消费国

印尼(17%):世界最重要的海底矿床

缅甸:高品位矿石逐渐减少

巴西与澳大利亚:具备新矿开发潜力

2040年的主要玩家:中国、印尼、非洲(刚果/尼日利亚)、欧洲、澳大利亚。

真正的挑战不是“储量不足”,而是“生产困难”。高品位矿石枯竭,低品位矿石开采需要更高成本和复杂技术。

结论

锡已不再是普通的基础金属。

它是连接 AI、电动车与清洁能源的未来战略资源,将在未来20年决定全球经济的走向。

Related Content

2026 年石脑油危机 – 最新情况更新

积极展望 | SO OK TRADING

自2月下旬中东战争爆发以来,全球能源市场剧烈震荡。原油价格突破每桶150美元,亚洲石脑油价格几乎翻倍。随后在5月中旬回落至 897美元/吨,但仍比去年高出 62.54%。

尽管价格开始下降,供应链的“滞后效应”依然存在 —— 运输延迟15–20天,港口因中东原料运输排队而严重拥堵,迫使亚洲产业界面临巨大挑战。

在泰国,SCGC 宣布不可抗力并暂时停产罗勇烯烃工厂;与此同时,PTTGC 与 SCGC 正在研究成立合资企业,以提升灵活性并降低长期成本。

在日本,知名品牌 Calbee 为应对油墨和树脂短缺,宣布将14款产品的包装印刷简化为黑白设计 —— 危机下的“极简设计”正成为新的趋势。

同时,复苏信号开始显现:

石脑油价格从最高1,020美元降至897美元/吨

价差回升:乙烯-石脑油 +250–280 / 丙烯-石脑油 +310–330

塑料价格仍处高位,但已有趋稳迹象

若中东局势不再恶化,预计该危机将在 6月底至7月初 开始缓解。

SO OK TRADING

FAST • SHARP • RELIABLE

您的商业合作伙伴

18 May 2026

世界正步入“长期高利率时代”

美国联邦储备委员会(Fed)在通胀居高不下、中东战争导致能源价格飙升的背景下,连续第三次决定将政策利率维持在 3.50–3.75%。

结果是,全球经济逐渐陷入 “高价不增长” 的陷阱,即 滞胀 (Stagflation),投资者和企业都必须更加谨慎应对。

股市剧烈波动,美元走强,原油价格飙升,债务负担依旧沉重——

这清楚地表明,世界正在从“等待降息”转向“咬牙维持高利率”来对抗顽固的通胀。

请阅读 SO OK TRADING 整理的 2026年4月全球经济概览,

了解利率走向与滞胀风险的最新视角,这是每一位投资者和企业都必须掌握的重要信息。

30 Apr 2026

「中东战争后的全球经济:谁在适应,谁在脆弱」

原油价格突破100美元,震撼全球经济——从把危机转化为机遇的中国,到必须加快能源结构改革的日本和欧洲。

SO OK TRADING 总结了在这场新经济博弈中“适应者”与“脆弱者”的全景图。能源不仅是燃料,更是推动全球经济结构变革的加速器。

FAST • SHARP • RELIABLE

27 Apr 2026