アルミニウム価格動向 – 2026年2月 SO OK TRADING Insight

Last updated: 1 Feb 2026

3397 Views

アルミニウム価格動向 – 2026年2月

SO OK TRADING Insight

世界市場の概況

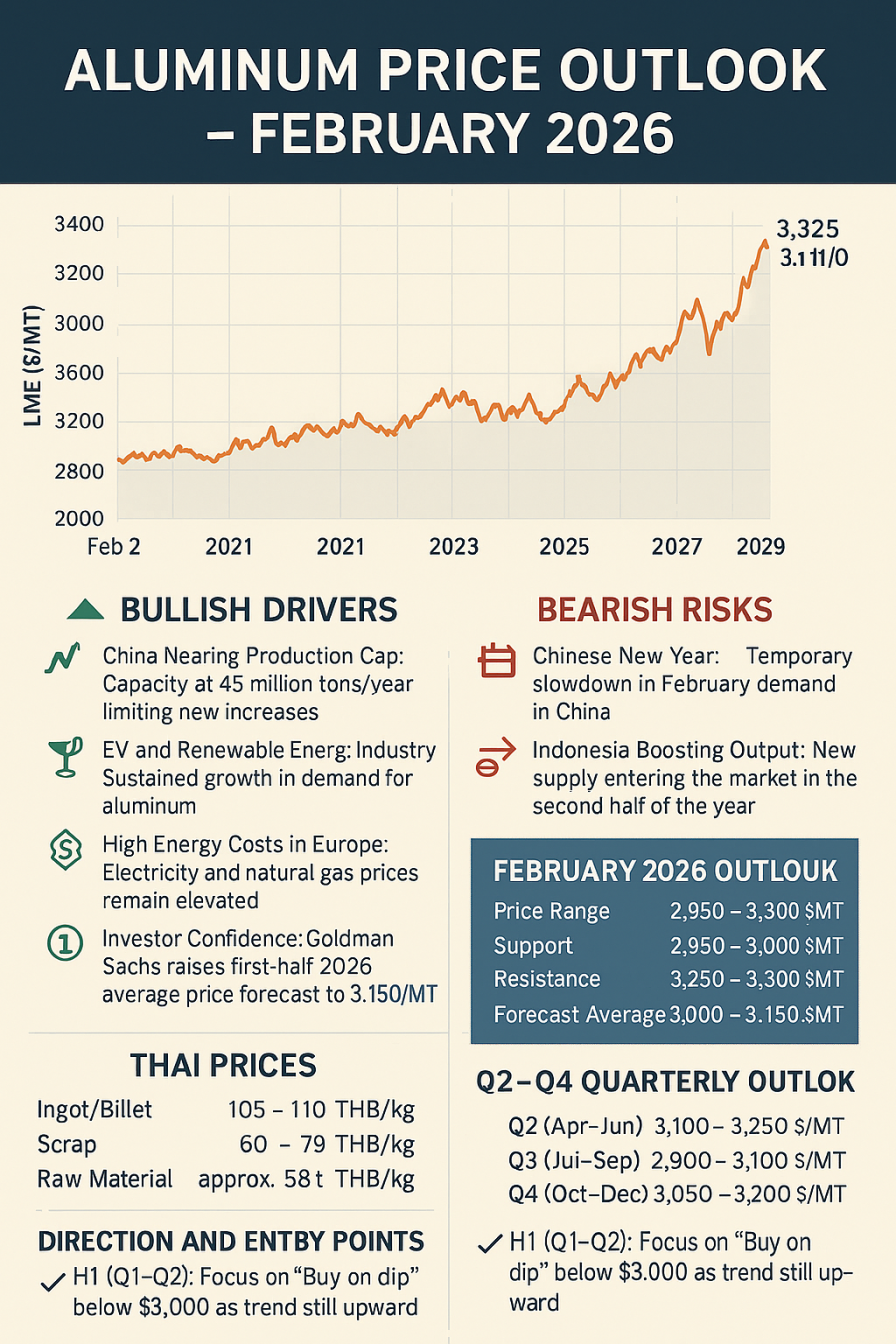

アルミニウム価格は依然として高水準を維持しています。1月29日には 3,325 USD/MT に達し、過去4年間で最高値を更新しました。1月30日の最新終値は 3,110 USD/MT で、わずか4週間で +8.78% の上昇を記録しました。これは供給制約と投資家の強い信頼感を反映しています。

強気要因 (Bullish Drivers)

中国の生産能力制限:年間4,500万トンに近づき、新規供給が制限されている

EV・再生可能エネルギー需要:電気自動車や再生可能エネルギー分野からの需要が継続的に増加

欧州の高いエネルギーコスト:電力・天然ガス価格が高止まりし、製錬コストを押し上げている

投資家信頼感:ゴールドマン・サックスが2026年上半期の平均価格予測を 3,150 USD/MT に引き上げ

弱気要因 (Bearish Risks)

春節による需要減速:2月は中国国内需要が一時的に減少

インドネシアの新規供給:年後半に新しい供給が市場に流入し、在庫逼迫を緩和する可能性

2026年2月の価格見通し

価格レンジ:2,950 – 3,300 USD/MT

サポート:2,950 – 3,000 USD/MT

レジスタンス:3,250 – 3,300 USD/MT

予測平均:3,000 – 3,150 USD/MT

タイ市場参考価格:インゴット 105–110 THB/kg スクラップ 60–70 THB/kg 原材料コスト 約98 THB/kg

四半期ごとの見通し (2026年)

Q1 (1–3月):3,000 – 3,150 USD/MT → 高水準だが調整局面

Q2 (4–6月):3,100 – 3,250 USD/MT → 中国需要回復 + EV/再エネ需要ピーク

Q3 (7–9月):2,900 – 3,100 USD/MT → インドネシア供給が市場に参入

Q4 (10–12月):3,050 – 3,200 USD/MT → 冬季需要 + 年末生産増

戦略的エントリーポイント

上半期 (Q1–Q2):価格が3,000 USD以下に調整した際に「Buy on dip」を狙う

下半期 (Q3–Q4):インドネシア・中国の新規供給を注視し、供給増加が顕著な場合は長期契約を検討

✨ まとめ:2026年2月のアルミニウム価格は 3,000 USD/MT以上 を維持しつつ、短期的には「調整局面」に入る可能性があります。EVや再生可能エネルギー分野の需要が強く、供給制約が続くため、市場は依然として堅調です。価格が3,000 USDを下回る場面は、在庫確保の好機となるでしょう。

SO OK TRADING Insight

世界市場の概況

アルミニウム価格は依然として高水準を維持しています。1月29日には 3,325 USD/MT に達し、過去4年間で最高値を更新しました。1月30日の最新終値は 3,110 USD/MT で、わずか4週間で +8.78% の上昇を記録しました。これは供給制約と投資家の強い信頼感を反映しています。

強気要因 (Bullish Drivers)

中国の生産能力制限:年間4,500万トンに近づき、新規供給が制限されている

EV・再生可能エネルギー需要:電気自動車や再生可能エネルギー分野からの需要が継続的に増加

欧州の高いエネルギーコスト:電力・天然ガス価格が高止まりし、製錬コストを押し上げている

投資家信頼感:ゴールドマン・サックスが2026年上半期の平均価格予測を 3,150 USD/MT に引き上げ

弱気要因 (Bearish Risks)

春節による需要減速:2月は中国国内需要が一時的に減少

インドネシアの新規供給:年後半に新しい供給が市場に流入し、在庫逼迫を緩和する可能性

2026年2月の価格見通し

価格レンジ:2,950 – 3,300 USD/MT

サポート:2,950 – 3,000 USD/MT

レジスタンス:3,250 – 3,300 USD/MT

予測平均:3,000 – 3,150 USD/MT

タイ市場参考価格:インゴット 105–110 THB/kg スクラップ 60–70 THB/kg 原材料コスト 約98 THB/kg

四半期ごとの見通し (2026年)

Q1 (1–3月):3,000 – 3,150 USD/MT → 高水準だが調整局面

Q2 (4–6月):3,100 – 3,250 USD/MT → 中国需要回復 + EV/再エネ需要ピーク

Q3 (7–9月):2,900 – 3,100 USD/MT → インドネシア供給が市場に参入

Q4 (10–12月):3,050 – 3,200 USD/MT → 冬季需要 + 年末生産増

戦略的エントリーポイント

上半期 (Q1–Q2):価格が3,000 USD以下に調整した際に「Buy on dip」を狙う

下半期 (Q3–Q4):インドネシア・中国の新規供給を注視し、供給増加が顕著な場合は長期契約を検討

✨ まとめ:2026年2月のアルミニウム価格は 3,000 USD/MT以上 を維持しつつ、短期的には「調整局面」に入る可能性があります。EVや再生可能エネルギー分野の需要が強く、供給制約が続くため、市場は依然として堅調です。価格が3,000 USDを下回る場面は、在庫確保の好機となるでしょう。

関連コンテンツ

アルミニウム沸騰!LME急騰 – プレミアムは過去10年で最高水準

2026年5月、世界のアルミニウム市場は「ここ数年で最も熱い」状況が続いています。価格は1トンあたり3,600ドルを突破し、中東の供給危機とEV・クリーンエネルギー産業からの旺盛な需要に支えられています。

12 May 2026

ニッケルはもはや単なる金属ではありません。

今日、それはタイ経済をクリーンエネルギーと先端技術の時代へと導く戦略的な原材料となっています。

電気自動車用バッテリーから洋上風力発電の構造物まで――ニッケルは大きな転換の中心にあります。

7 Feb 2026