「2026年: グリーン経済とスマート農業への転換期 — グリーンエネルギーは生き残りの道、農業は富の源。タイは木質ペレット、キャッサバ、ドリアンという世界が求めるスター商品で世界市場に挑む」

Last updated: 3 Mar 2026

1759 Views

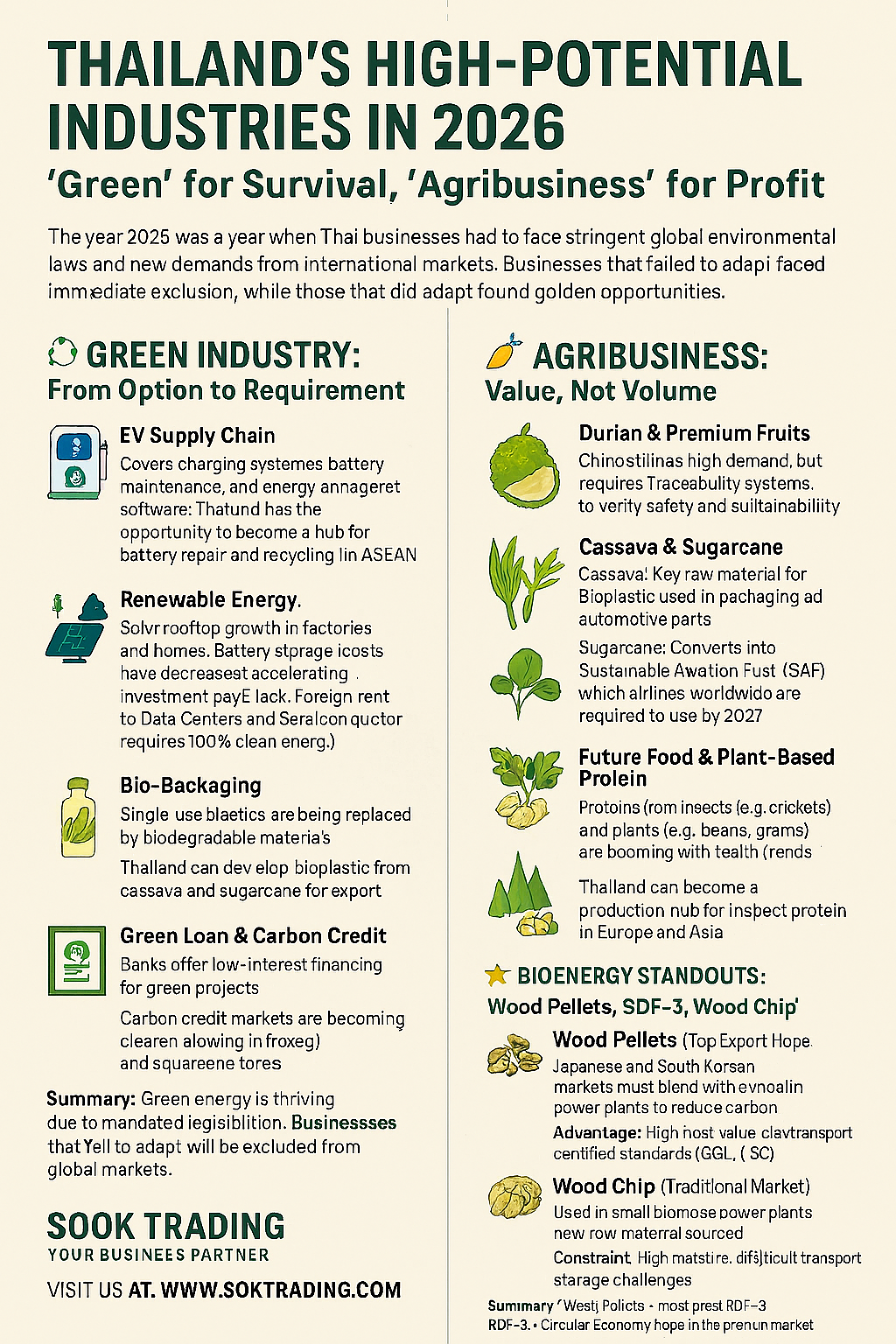

2026年 タイの成長産業: 「グリーン」は生き残り、「農業」は繁栄

グリーンとはグリーンエネルギー、環境に優しいエネルギー。

農業の注目商品は、バイオ燃料用のキャッサバやサトウキビ、そして輸出向けのプレミアムフルーツ(ドリアンなど)。

2026年は、タイのビジネスが厳格な国際環境法と新しい世界市場の需要に直面する年です。

適応できなければ即座に排除されますが、適応できれば産業とビジネスにとって黄金のチャンスとなります。

♻️ グリーン産業 (Green Industry): オプションから必須へ

EVサプライチェーン: 充電システム、バッテリー保守、エネルギー管理ソフトウェア。タイはASEANにおけるバッテリー修理・リサイクルのハブとなる可能性。

再生可能エネルギー: 工場や家庭でのソーラールーフトップ急成長。バッテリーストレージの価格低下で投資回収が早まる。データセンターや半導体投資は100%クリーンエネルギー必須。

バイオパッケージ: 使い捨てプラスチックは生分解性素材に置き換え。キャッサバやサトウキビ由来のバイオプラスチックを輸出可能。

グリーンローン & カーボンクレジット: 銀行は低金利でグリーンプロジェクトを融資。カーボンクレジット市場が明確化し、森林造成やクリーンエネルギーが直接収益化可能。

まとめ: グリーンエネルギーは法律によって義務化。適応しない企業は世界市場から排除される。

農業産業 (Agribusiness): 量より価値

プレミアムフルーツ (ドリアンなど): 中国で高需要。安全性と持続可能性を保証するトレーサビリティが必須。

キャッサバ & サトウキビ: キャッサバはバイオプラスチック原料。サトウキビは持続可能航空燃料(SAF)に加工、2027年までに航空業界で義務化。

フューチャーフード & 植物性タンパク質: 昆虫タンパク質(コオロギなど)、豆類・穀物由来の植物性タンパク質。健康志向市場で急成長。タイは欧州・アジア向け昆虫タンパク質のハブに。

ハーブ & 機能性食品: ウコン、生姜、ツボクサは世界的なサプリ・化粧品市場で需要拡大。

成長の早い樹木 (ユーカリ、アカシア): 木質ペレット生産、さらにカーボンクレジット販売も可能。

バイオマス燃料のスター: Wood Pellets, RDF-3, Wood Chip

Wood Pellets (輸出の希望): 日本・韓国市場で石炭混焼に必須。高発熱量、輸送容易、国際認証あり。タイ政府は早成樹の植林を支援。

RDF-3 (国内市場): セメント工場や廃棄物発電で使用。循環型経済に貢献し、石炭依存を削減。ただし品質の不安定さと廃棄物分別の課題あり。

Wood Chip (従来市場): 小規模バイオマス発電で利用。湿度が高く輸送・保管が難しい。プレミアム市場ではWood Pelletsに押されつつある。

まとめ:

Wood Pellets = 輸出のスター

RDF-3 = 国内循環型経済の希望

Wood Chip = 依然利用可能だが新しいバイオ燃料に押される

2026年戦略の結論

グリーン産業 = 生き残りの道 → 適応しない企業は世界市場から排除

バイオ農業 = 富の源 → タイ農業は「生産物販売」から「産業原料」へ転換

Wood Pellets, RDF-3, Wood Chip = 循環型経済への移行の指標

キャッサバ & サトウキビ = バイオリファイナリーの中心、タイ農業を世界市場へ

✨ 2026年は「大量生産の競争」ではなく、「世界トレンドと持続可能基準に沿った生産の競争」

SO OK TRADING: あなたのビジネスパートナー VISIT US AT: WWW.SOOKTRADING.COM

グリーンとはグリーンエネルギー、環境に優しいエネルギー。

農業の注目商品は、バイオ燃料用のキャッサバやサトウキビ、そして輸出向けのプレミアムフルーツ(ドリアンなど)。

2026年は、タイのビジネスが厳格な国際環境法と新しい世界市場の需要に直面する年です。

適応できなければ即座に排除されますが、適応できれば産業とビジネスにとって黄金のチャンスとなります。

♻️ グリーン産業 (Green Industry): オプションから必須へ

EVサプライチェーン: 充電システム、バッテリー保守、エネルギー管理ソフトウェア。タイはASEANにおけるバッテリー修理・リサイクルのハブとなる可能性。

再生可能エネルギー: 工場や家庭でのソーラールーフトップ急成長。バッテリーストレージの価格低下で投資回収が早まる。データセンターや半導体投資は100%クリーンエネルギー必須。

バイオパッケージ: 使い捨てプラスチックは生分解性素材に置き換え。キャッサバやサトウキビ由来のバイオプラスチックを輸出可能。

グリーンローン & カーボンクレジット: 銀行は低金利でグリーンプロジェクトを融資。カーボンクレジット市場が明確化し、森林造成やクリーンエネルギーが直接収益化可能。

まとめ: グリーンエネルギーは法律によって義務化。適応しない企業は世界市場から排除される。

農業産業 (Agribusiness): 量より価値

プレミアムフルーツ (ドリアンなど): 中国で高需要。安全性と持続可能性を保証するトレーサビリティが必須。

キャッサバ & サトウキビ: キャッサバはバイオプラスチック原料。サトウキビは持続可能航空燃料(SAF)に加工、2027年までに航空業界で義務化。

フューチャーフード & 植物性タンパク質: 昆虫タンパク質(コオロギなど)、豆類・穀物由来の植物性タンパク質。健康志向市場で急成長。タイは欧州・アジア向け昆虫タンパク質のハブに。

ハーブ & 機能性食品: ウコン、生姜、ツボクサは世界的なサプリ・化粧品市場で需要拡大。

成長の早い樹木 (ユーカリ、アカシア): 木質ペレット生産、さらにカーボンクレジット販売も可能。

バイオマス燃料のスター: Wood Pellets, RDF-3, Wood Chip

Wood Pellets (輸出の希望): 日本・韓国市場で石炭混焼に必須。高発熱量、輸送容易、国際認証あり。タイ政府は早成樹の植林を支援。

RDF-3 (国内市場): セメント工場や廃棄物発電で使用。循環型経済に貢献し、石炭依存を削減。ただし品質の不安定さと廃棄物分別の課題あり。

Wood Chip (従来市場): 小規模バイオマス発電で利用。湿度が高く輸送・保管が難しい。プレミアム市場ではWood Pelletsに押されつつある。

まとめ:

Wood Pellets = 輸出のスター

RDF-3 = 国内循環型経済の希望

Wood Chip = 依然利用可能だが新しいバイオ燃料に押される

2026年戦略の結論

グリーン産業 = 生き残りの道 → 適応しない企業は世界市場から排除

バイオ農業 = 富の源 → タイ農業は「生産物販売」から「産業原料」へ転換

Wood Pellets, RDF-3, Wood Chip = 循環型経済への移行の指標

キャッサバ & サトウキビ = バイオリファイナリーの中心、タイ農業を世界市場へ

✨ 2026年は「大量生産の競争」ではなく、「世界トレンドと持続可能基準に沿った生産の競争」

SO OK TRADING: あなたのビジネスパートナー VISIT US AT: WWW.SOOKTRADING.COM

関連コンテンツ

タイの果物が中国市場を席巻!2024–2027 黄金の輸出時代

タイは依然として中国への生鮮果物輸出第1位を維持し、ドリアン・マンゴスチン・ロンガン・ココナッツ・ナムドクマイマンゴーなど幅広い人気を獲得。さらに乾燥果物や急成長するEC市場の新トレンドも加わり、需要はますます拡大しています。

11 Feb 2026

Copper prices are expected to remain elevated and bullish in 2026, driven by strong demand from the green energy transition (EVs, renewables, grid upgrades) and persistent mine supply constraints/disruptions, with forecasts generally placing prices in the $10,000 to over $12,000 per tonne range, although some analysts foresee a slight cooling to $10,000-$11,000 as market balances tighten. Key factors include IRA spending, AI infrastructure needs, constrained new mine supply, and potential Chinese economic recovery, creating tight markets despite some projected minor surpluses.

Key Price Predictions (2026):

Goldman Sachs: $10,000 - $11,000/tonne range, averaging $10,710/tonne in H1 2026.

J.P. Morgan: Averaging around $12,075/tonne, with potential spikes to $12,500/tonne in Q2.

Bank of America: Average of $11,313/tonne, with potential for $15,000/tonne spikes.

UBS: $11,000/tonne by Sept 2026.

World Bank: Average of $9,800/tonne.

Bullish Drivers:

Energy Transition: Massive demand for grid expansion, EVs, and renewable infrastructure.

AI Infrastructure: Increased demand for data centers.

Supply Deficit: Mine disruptions (Grasberg, Kamoa-Kakula, etc.) and difficulty bringing new mines online.

China: Potential economic rebound acting as a catalyst.

Potential Headwinds/Volatility:

Policy-induced Surpluses: E.g., from IRA incentives or scrap availability.

Stronger USD: Can weigh on commodity prices.

Slower Demand: If China's recovery falters.

Overall Outlook:

Expect a tight market with strong underlying demand, leading to high prices, but with significant volatility due to policy shifts and mine output fluctuations. The market is moving towards a structural deficit, supporting higher prices long-term

30 Dec 2025

An analysis of the aluminum market in 2026 indicates a likely continued market deficit and upward price pressure, driven by constrained supply and resilient demand from green energy sectors. However, significant volatility is expected due to policy uncertainties and the potential for new Indonesian supply to eventually balance the market.

Key Drivers and Projections for 2026

Supply Side Analysis

Capacity Constraints: China's primary aluminum output is approaching its self-imposed 45 million-tonne capacity cap, limiting global supply growth.

Power Challenges: Smelters outside of China face intense competition for power from energy-intensive sectors like AI data centers, which are willing to pay higher prices for long-term contracts. This has kept significant capacity offline in Europe and the US.

Production Disruptions: Outages and potential shutdowns at existing smelters in Iceland and Mozambique further tighten the market.

Scrap Supply Pressure: The EU's planned implementation of the Carbon Border Adjustment Mechanism (CBAM) and potential scrap export tariffs in spring 2026 are expected to impact global scrap flows, creating regional shortages and price volatility.

New Capacity: Indonesia is a key source of new supply, with several projects in the pipeline. However, analysts suggest the pace of the ramp-up may be slower than expected due to infrastructure and policy challenges, meaning it is unlikely to fully offset near-term tightness.

Demand Side Analysis

Green Transition Demand: Demand from "green" sectors such as solar panels, new energy vehicles, and energy transition infrastructure remains strong, providing fundamental support for the market.

Substitution Effect: Aluminum's wide price discount relative to copper has encouraged substitution in electrical applications, acting as a tailwind for demand and prices.

Construction and Automotive: The construction and automotive industries continue to be major consumers, with growing demand for lightweight, low-carbon aluminum products.

Price Forecasts and Volatility

The market is expected to remain in a deficit in 2026, with estimates ranging from 200,000 to 600,000 tonnes. This structural tightness is leading most analysts to forecast sustained or rising prices.

Bullish Views: Analysts at Bank of America project prices of $3,000/tonne as early as 2026. J.P. Morgan also expects prices to approach $3,000/tonne in Q1 2026. ING forecasts an average price of $2,900/tonne for the year.

Bearish/Conservative Views: Goldman Sachs is an outlier, forecasting prices to decline to $2,350/tonne by Q4 2026, anticipating a market surplus later in the year. SMM forecasts a "high first, then lower" pattern, with prices finding equilibrium in the $2,700–$2,800/tonne range by year-end.

Premiums: Regional premiums, particularly the US Midwest premium, are expected to remain high and volatile due to tariffs and regional supply dynamics, creating a disconnect from the LME benchmark price.

In essence, 2026 is projected to be a year of high volatility where participants need to focus on scenario readiness rather than relying on a single price forecast, as geopolitical and energy policies significantly influence regional supply and costs

31 Dec 2025