镍:推动电动车产业的新力量 —— 从硬币到清洁能源,镍正在改变世界

Last updated: 7 Feb 2026

1598 Views

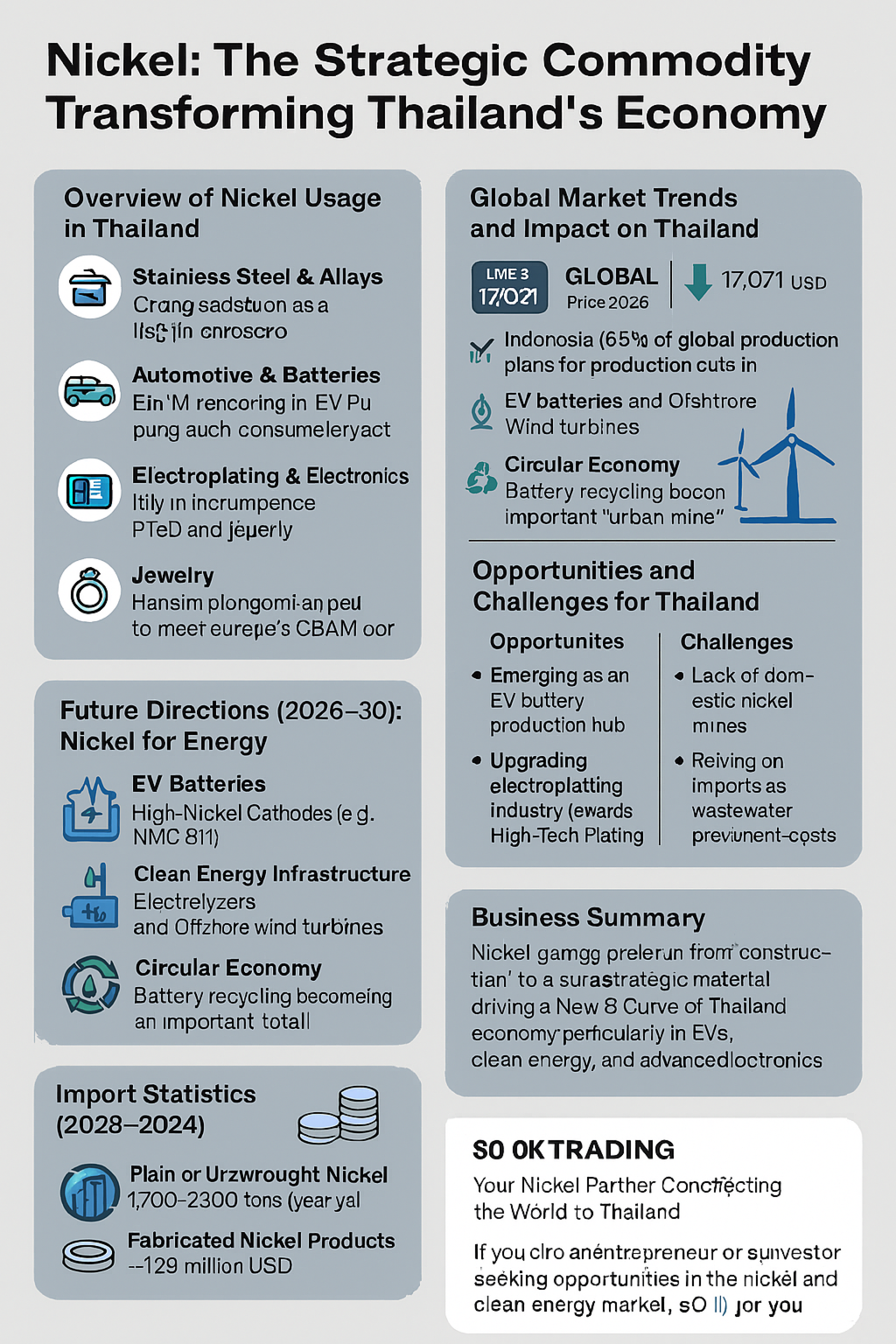

镍:正在重塑泰国经济的战略性原材料

镍(Nickel)不再只是用于厨具或硬币的普通金属。

如今,它已成为推动泰国经济迈向清洁能源和新兴产业的“核心动力”。

泰国镍的应用概览

不锈钢与合金:在厨具、建筑材料和建筑设计中占最大使用比例

汽车与电池:随着EV投资和电池工厂建设,硫酸镍需求激增

电镀与电子产业:用于PCB电路板和物联网传感器、智能汽车零部件的高精度电镀

珠宝首饰:用于白金和时尚饰品(需控制标准以避免皮肤过敏)

硬币:泰国财政部仍以镍为主要流通硬币材料

全球市场趋势及对泰国的影响

LME价格(2026年2月初):17,071美元/吨(较1月末的19,137美元/吨有所下降)

印尼(占全球产量65%)计划在2026年减产 → 长期可能推高价格

EV电池与不锈钢需求仍是主要驱动力

未来展望(2026–2030):Nickel for Energy

EV电池:高镍正极材料(NMC 811)逐步取代钴

清洁能源基础设施:用于绿色氢能电解槽和海上风电结构

循环经济:废旧电池回收成为重要的“城市矿山”

全球供应链:各国减少对印尼和俄罗斯的依赖,泰国有望成为前驱体生产中心

泰国的机遇与挑战

机遇

成为东盟EV电池生产基地

升级电镀产业至高科技电镀

利用再生镍以满足欧洲CBAM要求

挑战

泰国无镍矿,依赖进口

环境法规趋严,迫使工厂投资废水处理系统

全球镍价波动直接影响生产成本

进口统计(2023–2024)

未加工镍:每年1,700–2,200吨,约2,900万美元

加工镍制品:约1.29亿美元

主要进口来源:日本(36%)、加拿大、挪威、中国

商业总结

镍正在从“建筑材料”转变为“战略性原材料”,推动泰国经济新的增长曲线(New S-Curve),尤其在EV、清洁能源和先进电子产业中发挥关键作用。

SO OK TRADING:连接全球与泰国镍产业的合作伙伴

对于寻求镍与清洁能源市场机遇的企业与投资者而言,泰国正敞开大门。

SO OK TRADING 将成为您值得信赖的合作伙伴,共同迈向未来。

镍(Nickel)不再只是用于厨具或硬币的普通金属。

如今,它已成为推动泰国经济迈向清洁能源和新兴产业的“核心动力”。

泰国镍的应用概览

不锈钢与合金:在厨具、建筑材料和建筑设计中占最大使用比例

汽车与电池:随着EV投资和电池工厂建设,硫酸镍需求激增

电镀与电子产业:用于PCB电路板和物联网传感器、智能汽车零部件的高精度电镀

珠宝首饰:用于白金和时尚饰品(需控制标准以避免皮肤过敏)

硬币:泰国财政部仍以镍为主要流通硬币材料

全球市场趋势及对泰国的影响

LME价格(2026年2月初):17,071美元/吨(较1月末的19,137美元/吨有所下降)

印尼(占全球产量65%)计划在2026年减产 → 长期可能推高价格

EV电池与不锈钢需求仍是主要驱动力

未来展望(2026–2030):Nickel for Energy

EV电池:高镍正极材料(NMC 811)逐步取代钴

清洁能源基础设施:用于绿色氢能电解槽和海上风电结构

循环经济:废旧电池回收成为重要的“城市矿山”

全球供应链:各国减少对印尼和俄罗斯的依赖,泰国有望成为前驱体生产中心

泰国的机遇与挑战

机遇

成为东盟EV电池生产基地

升级电镀产业至高科技电镀

利用再生镍以满足欧洲CBAM要求

挑战

泰国无镍矿,依赖进口

环境法规趋严,迫使工厂投资废水处理系统

全球镍价波动直接影响生产成本

进口统计(2023–2024)

未加工镍:每年1,700–2,200吨,约2,900万美元

加工镍制品:约1.29亿美元

主要进口来源:日本(36%)、加拿大、挪威、中国

商业总结

镍正在从“建筑材料”转变为“战略性原材料”,推动泰国经济新的增长曲线(New S-Curve),尤其在EV、清洁能源和先进电子产业中发挥关键作用。

SO OK TRADING:连接全球与泰国镍产业的合作伙伴

对于寻求镍与清洁能源市场机遇的企业与投资者而言,泰国正敞开大门。

SO OK TRADING 将成为您值得信赖的合作伙伴,共同迈向未来。

Related Content

2026年的锌市场,已经不仅仅是价格与供需的故事。锌正在经历一场重大转型:从传统的基础工业金属,逐步迈向支撑全球清洁能源与新技术的战略性金属。

它不再只是用于防锈和建筑的材料,而是成为电动车锌空气电池的核心,以及太阳能与风能基础设施不可或缺的一环。尽管短期内市场面临供过于求的挑战,但在背后,锌正打开一扇通往未来的窗口 —— 一个以可持续发展和零碳目标为核心的新时代。

3 Apr 2026

An analysis of the aluminum market in 2026 indicates a likely continued market deficit and upward price pressure, driven by constrained supply and resilient demand from green energy sectors. However, significant volatility is expected due to policy uncertainties and the potential for new Indonesian supply to eventually balance the market.

Key Drivers and Projections for 2026

Supply Side Analysis

Capacity Constraints: China's primary aluminum output is approaching its self-imposed 45 million-tonne capacity cap, limiting global supply growth.

Power Challenges: Smelters outside of China face intense competition for power from energy-intensive sectors like AI data centers, which are willing to pay higher prices for long-term contracts. This has kept significant capacity offline in Europe and the US.

Production Disruptions: Outages and potential shutdowns at existing smelters in Iceland and Mozambique further tighten the market.

Scrap Supply Pressure: The EU's planned implementation of the Carbon Border Adjustment Mechanism (CBAM) and potential scrap export tariffs in spring 2026 are expected to impact global scrap flows, creating regional shortages and price volatility.

New Capacity: Indonesia is a key source of new supply, with several projects in the pipeline. However, analysts suggest the pace of the ramp-up may be slower than expected due to infrastructure and policy challenges, meaning it is unlikely to fully offset near-term tightness.

Demand Side Analysis

Green Transition Demand: Demand from "green" sectors such as solar panels, new energy vehicles, and energy transition infrastructure remains strong, providing fundamental support for the market.

Substitution Effect: Aluminum's wide price discount relative to copper has encouraged substitution in electrical applications, acting as a tailwind for demand and prices.

Construction and Automotive: The construction and automotive industries continue to be major consumers, with growing demand for lightweight, low-carbon aluminum products.

Price Forecasts and Volatility

The market is expected to remain in a deficit in 2026, with estimates ranging from 200,000 to 600,000 tonnes. This structural tightness is leading most analysts to forecast sustained or rising prices.

Bullish Views: Analysts at Bank of America project prices of $3,000/tonne as early as 2026. J.P. Morgan also expects prices to approach $3,000/tonne in Q1 2026. ING forecasts an average price of $2,900/tonne for the year.

Bearish/Conservative Views: Goldman Sachs is an outlier, forecasting prices to decline to $2,350/tonne by Q4 2026, anticipating a market surplus later in the year. SMM forecasts a "high first, then lower" pattern, with prices finding equilibrium in the $2,700–$2,800/tonne range by year-end.

Premiums: Regional premiums, particularly the US Midwest premium, are expected to remain high and volatile due to tariffs and regional supply dynamics, creating a disconnect from the LME benchmark price.

In essence, 2026 is projected to be a year of high volatility where participants need to focus on scenario readiness rather than relying on a single price forecast, as geopolitical and energy policies significantly influence regional supply and costs

31 Dec 2025