SO OK TRADING 洞察:2026年2月铜价展望 全球最需要的战略金属——铜

Last updated: 1 Feb 2026

2543 Views

2026年2月铜价趋势

AI与电动车时代的战略资产:铜

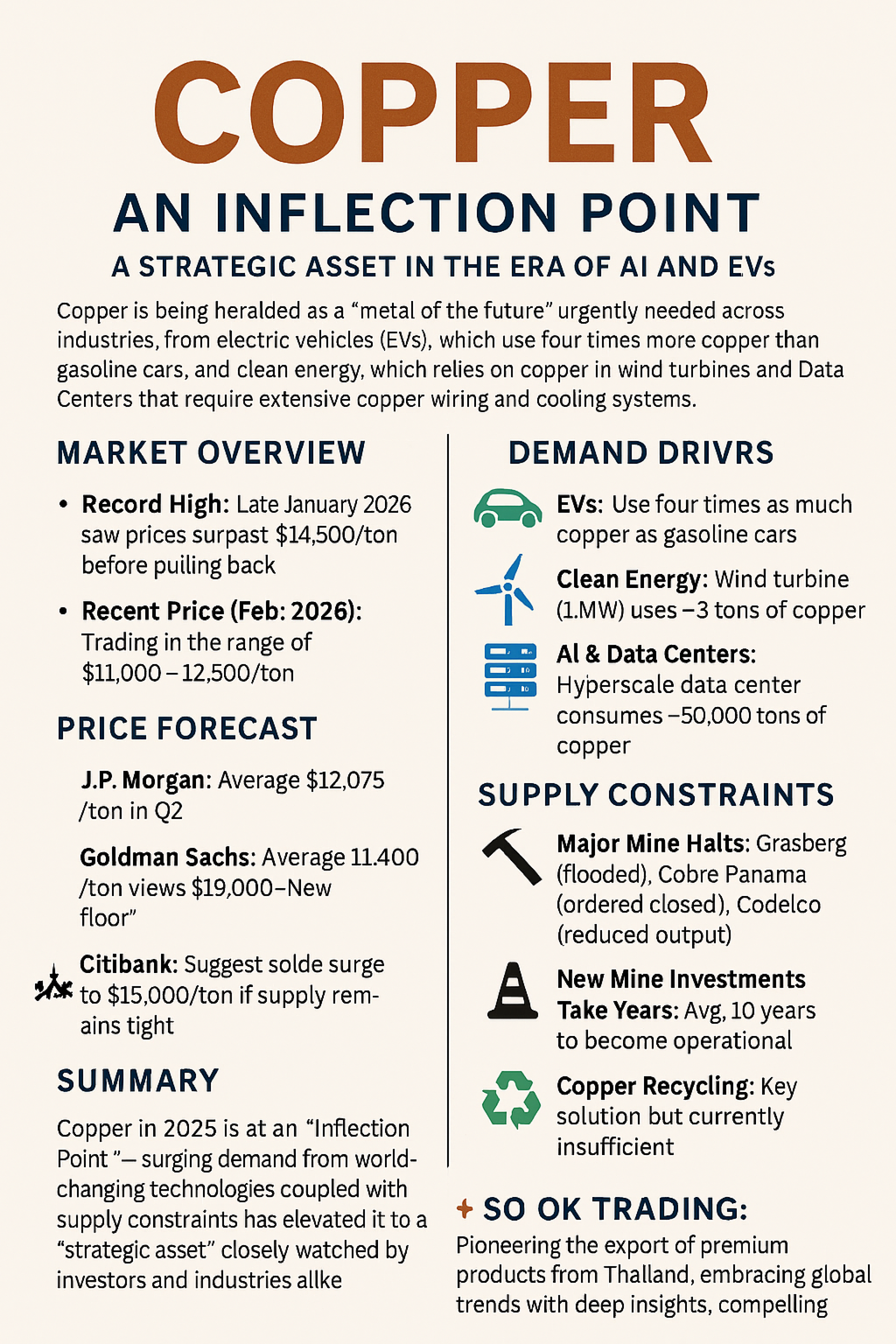

铜正在被誉为“未来的金属”,几乎所有产业都迫切需要它。电动车(EV)使用的铜是燃油车的4倍;清洁能源依赖铜来制造风力发电机和升级电网;人工智能与数据中心的建设更需要大量铜线和冷却系统。铜已不仅仅是工业金属,而是全球战略资产,象征着能源与科技的未来转型。

市场概况

历史最高价:2026年1月底,铜价突破14,500美元/吨后回落

最新价格(2月):在11,000–12,500美元/吨区间波动

金融机构预测

J.P. Morgan:平均12,075美元/吨,预计第二季度可能创下新高

Goldman Sachs:平均11,400美元/吨,认为10,000–11,000美元是“新底部”

Citibank:若供应持续紧张,可能飙升至15,000美元/吨

SO OK TRADING 的观点

保守预测:平均12,500 底部12,000 顶部13,750

现实预测:平均12,800 底部12,350 顶部14,000

采购策略:在12,400–12,600美元区间逢低买入,有助于增加利润并降低风险

推动价格的因素

电动车:使用铜量是燃油车的4倍

清洁能源:风力发电机1MW需约3吨铜

️ AI与数据中心:一个超大规模数据中心需约50,000吨铜

⚔️ 国防工业:地缘政治紧张推高需求

供应限制

⛏️ 大型矿山停产:Grasberg(洪水)、Cobre Panama(关闭)、Codelco(减产)

️ 新矿开发需时长:平均10年才能投产

♻️ 铜回收:虽是重要解决方案,但目前仍不足以满足需求

总结

2026年的铜市场正处于**“关键转折点”。全球性技术变革带来的需求激增与供应紧张叠加,使铜成为投资者和产业界高度关注的战略资产**。

✨ SO OK TRADING:作为泰国优质产品出口的先驱,我们涵盖水果、稻米、金属及清洁能源。我们坚信,要让泰国品牌走向世界,必须依靠深度洞察、强有力的故事叙述以及对国际市场的适应能力。

铜是未来转型的象征。SO OK TRADING 正与世界同行,共同迈向这一新时代。

AI与电动车时代的战略资产:铜

铜正在被誉为“未来的金属”,几乎所有产业都迫切需要它。电动车(EV)使用的铜是燃油车的4倍;清洁能源依赖铜来制造风力发电机和升级电网;人工智能与数据中心的建设更需要大量铜线和冷却系统。铜已不仅仅是工业金属,而是全球战略资产,象征着能源与科技的未来转型。

市场概况

历史最高价:2026年1月底,铜价突破14,500美元/吨后回落

最新价格(2月):在11,000–12,500美元/吨区间波动

金融机构预测

J.P. Morgan:平均12,075美元/吨,预计第二季度可能创下新高

Goldman Sachs:平均11,400美元/吨,认为10,000–11,000美元是“新底部”

Citibank:若供应持续紧张,可能飙升至15,000美元/吨

SO OK TRADING 的观点

保守预测:平均12,500 底部12,000 顶部13,750

现实预测:平均12,800 底部12,350 顶部14,000

采购策略:在12,400–12,600美元区间逢低买入,有助于增加利润并降低风险

推动价格的因素

电动车:使用铜量是燃油车的4倍

清洁能源:风力发电机1MW需约3吨铜

️ AI与数据中心:一个超大规模数据中心需约50,000吨铜

⚔️ 国防工业:地缘政治紧张推高需求

供应限制

⛏️ 大型矿山停产:Grasberg(洪水)、Cobre Panama(关闭)、Codelco(减产)

️ 新矿开发需时长:平均10年才能投产

♻️ 铜回收:虽是重要解决方案,但目前仍不足以满足需求

总结

2026年的铜市场正处于**“关键转折点”。全球性技术变革带来的需求激增与供应紧张叠加,使铜成为投资者和产业界高度关注的战略资产**。

✨ SO OK TRADING:作为泰国优质产品出口的先驱,我们涵盖水果、稻米、金属及清洁能源。我们坚信,要让泰国品牌走向世界,必须依靠深度洞察、强有力的故事叙述以及对国际市场的适应能力。

铜是未来转型的象征。SO OK TRADING 正与世界同行,共同迈向这一新时代。

Related Content

ADC12:电动车时代与能源高涨的战略材料

ADC12(A383)不仅仅是普通的铝合金,它是全球压铸工厂首选的“英雄规格”。在需要降低能源成本并生产轻量化、高强度和高精度电动车零部件的时代,ADC12正成为不可替代的战略材料。

27 Mar 2026

UBC废铝罐:未来的绿色黄金

UBC(饮料用过铝罐)正从“可回收垃圾”跃升为全球循环经济的战略资源。纯度高达99%以上,能耗比原铝低95%,成为低碳制造的关键原料。

11 Feb 2026