「ANTIMONY AWAKENING:锑——绿色经济与全球能源革命的新动脉」 2026年4月22日 · SO OK TRADING

Last updated: 22 Apr 2026

1718 Views

锑:颠覆全球能源格局的战略矿物 —— 不仅供应紧缺,更是未来产业不可或缺的资源 SO OK TRADING · 2026年4月22日

在世界加速迈向清洁能源与先进技术的时代,锑 (Antimony) 正逐渐成为全球瞩目的焦点。它不仅因价格波动而备受关注,更因被列为“关键矿物 (Critical Mineral)”——在多个产业中不可或缺的战略资源。

从矿山到全球市场

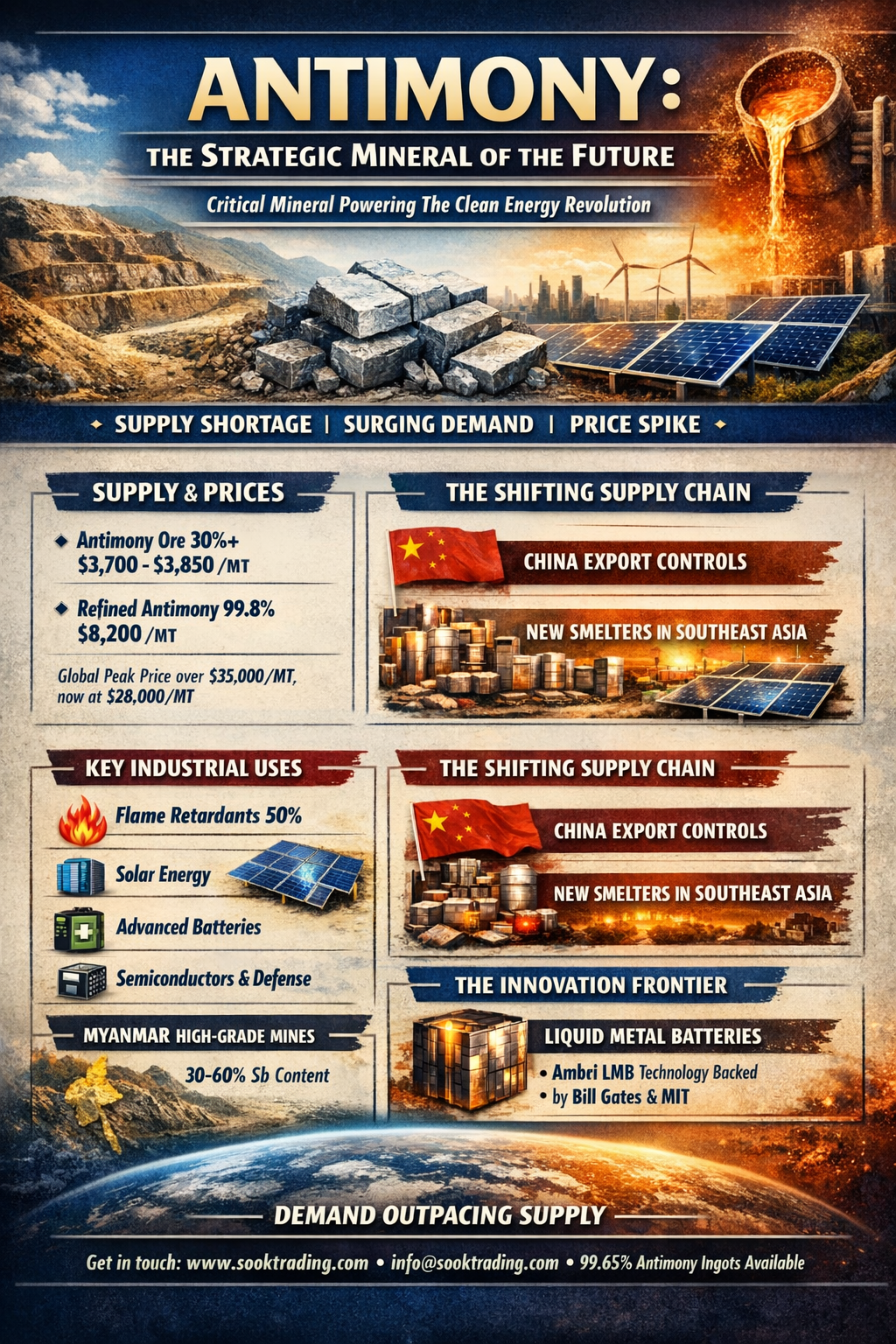

2026年4月,锑矿石与锑锭价格依然维持高位:

锑矿石 (品位30%以上):130,000 – 135,000泰铢/吨

精炼锑 (99.8%):约150,000泰铢/吨 全球市场在2025年曾创下35,000美元/吨的高点,目前回落至28,000美元/吨(约820,000泰铢),但仍远高于历史平均水平。

永不减退的需求

锑广泛应用于以下产业:

阻燃剂:占市场约50%

太阳能电池板:提升玻璃透光率

电池:耐用的铅酸电池与新型液态金属电池 (LMB)

军工与半导体:红外设备与先进芯片的重要组成部分

中国的生产转移

自2024年底中国加强出口管制以来,中国资本将冶炼厂转移至老挝与柬埔寨,以规避配额限制,导致全球市场锑锭供应增加。

泰国的机遇与挑战

机遇:更容易将原矿输送至边境冶炼厂

挑战:需严格管理许可证与原产地证明,避免被认定为“非法矿石”

缅甸:强劲的新供应源

掸邦及中缅边境的Tha Byu矿山出产品位高达30–60%的锑矿石。2025–2026年间,泰国进口量增长超过300%。

⚡ 锑电池创新 MIT孵化企业Ambri(比尔·盖茨投资)研发的液态金属电池 (LMB):

使用寿命超过20年

安全,无火灾风险

成本低于锂电池

此外,莱斯大学开发的锑-石墨技术解决了电池老化问题,使锑在锂电与钠电中均发挥关键作用。

市场趋势总结

需求 > 供应:未来数年仍将持续

亚太地区:占全球市场64.4%,为太阳能与电子产业中心

回收利用:尚不足以满足清洁能源的快速增长需求

工业国的未来布局

锑正被提升为绿色经济与先进技术的核心:

清洁能源储能:液态金属电池用于电网级储能

安全标准提升:阻燃剂广泛应用于电子产品与建筑材料

电动车电池:耐用铅酸电池与新型高稳定性电池

军工与航天:红外传感器与特殊半导体不可或缺

♻️ 锑的回收与循环经济 美国与欧洲加大投资,从废旧电池与电子垃圾中回收锑,以减少对中国的依赖,建立稳定供应链。

未来展望

全球市场规模:2026年12.2亿美元 → 2037年20.1亿美元 (CAGR 5.8%)

亚太地区仍为核心(中国、日本、韩国)

工业国加快新矿投资、回收利用及在中国以外设立冶炼厂

结论

锑不仅是一种矿物,更是全球经济的新动脉。它将在清洁能源、电动车、军工与航天等领域发挥不可替代的作用,成为未来产业结构的战略支柱。

联系我们:

www.sooktrading.com

✉️ sooktrading@outlook.com

SO OK TRADING – FAST • SHARP • RELIABLE

在世界加速迈向清洁能源与先进技术的时代,锑 (Antimony) 正逐渐成为全球瞩目的焦点。它不仅因价格波动而备受关注,更因被列为“关键矿物 (Critical Mineral)”——在多个产业中不可或缺的战略资源。

从矿山到全球市场

2026年4月,锑矿石与锑锭价格依然维持高位:

锑矿石 (品位30%以上):130,000 – 135,000泰铢/吨

精炼锑 (99.8%):约150,000泰铢/吨 全球市场在2025年曾创下35,000美元/吨的高点,目前回落至28,000美元/吨(约820,000泰铢),但仍远高于历史平均水平。

永不减退的需求

锑广泛应用于以下产业:

阻燃剂:占市场约50%

太阳能电池板:提升玻璃透光率

电池:耐用的铅酸电池与新型液态金属电池 (LMB)

军工与半导体:红外设备与先进芯片的重要组成部分

中国的生产转移

自2024年底中国加强出口管制以来,中国资本将冶炼厂转移至老挝与柬埔寨,以规避配额限制,导致全球市场锑锭供应增加。

泰国的机遇与挑战

机遇:更容易将原矿输送至边境冶炼厂

挑战:需严格管理许可证与原产地证明,避免被认定为“非法矿石”

缅甸:强劲的新供应源

掸邦及中缅边境的Tha Byu矿山出产品位高达30–60%的锑矿石。2025–2026年间,泰国进口量增长超过300%。

⚡ 锑电池创新 MIT孵化企业Ambri(比尔·盖茨投资)研发的液态金属电池 (LMB):

使用寿命超过20年

安全,无火灾风险

成本低于锂电池

此外,莱斯大学开发的锑-石墨技术解决了电池老化问题,使锑在锂电与钠电中均发挥关键作用。

市场趋势总结

需求 > 供应:未来数年仍将持续

亚太地区:占全球市场64.4%,为太阳能与电子产业中心

回收利用:尚不足以满足清洁能源的快速增长需求

工业国的未来布局

锑正被提升为绿色经济与先进技术的核心:

清洁能源储能:液态金属电池用于电网级储能

安全标准提升:阻燃剂广泛应用于电子产品与建筑材料

电动车电池:耐用铅酸电池与新型高稳定性电池

军工与航天:红外传感器与特殊半导体不可或缺

♻️ 锑的回收与循环经济 美国与欧洲加大投资,从废旧电池与电子垃圾中回收锑,以减少对中国的依赖,建立稳定供应链。

未来展望

全球市场规模:2026年12.2亿美元 → 2037年20.1亿美元 (CAGR 5.8%)

亚太地区仍为核心(中国、日本、韩国)

工业国加快新矿投资、回收利用及在中国以外设立冶炼厂

结论

锑不仅是一种矿物,更是全球经济的新动脉。它将在清洁能源、电动车、军工与航天等领域发挥不可替代的作用,成为未来产业结构的战略支柱。

联系我们:

www.sooktrading.com

✉️ sooktrading@outlook.com

SO OK TRADING – FAST • SHARP • RELIABLE

Related Content

")

「霍尔木兹危机!美伊压力博弈震动全球原材料市场」

谈判尚未结束…… 全球政治与经济的博弈,所有企业都必须关注!

30 May 2026

「全球社会对特朗普第二任期(2026年)的看法」

世界正在进入“二极格局”时代 —— 美国与中国。

特朗普被视为果断但不可预测的领导人,对全球经济与安全造成巨大震荡。

22 Jul 2026