春节后的世界:美元走强、稀土短缺、人工智能崛起 从关税战到资源战——2026年的世界已不再相同 特朗普2.0震撼全球:经济正在变成战场

Last updated: 19 Feb 2026

1619 Views

全球经济进入特朗普2.0时代:从贸易战到资源战

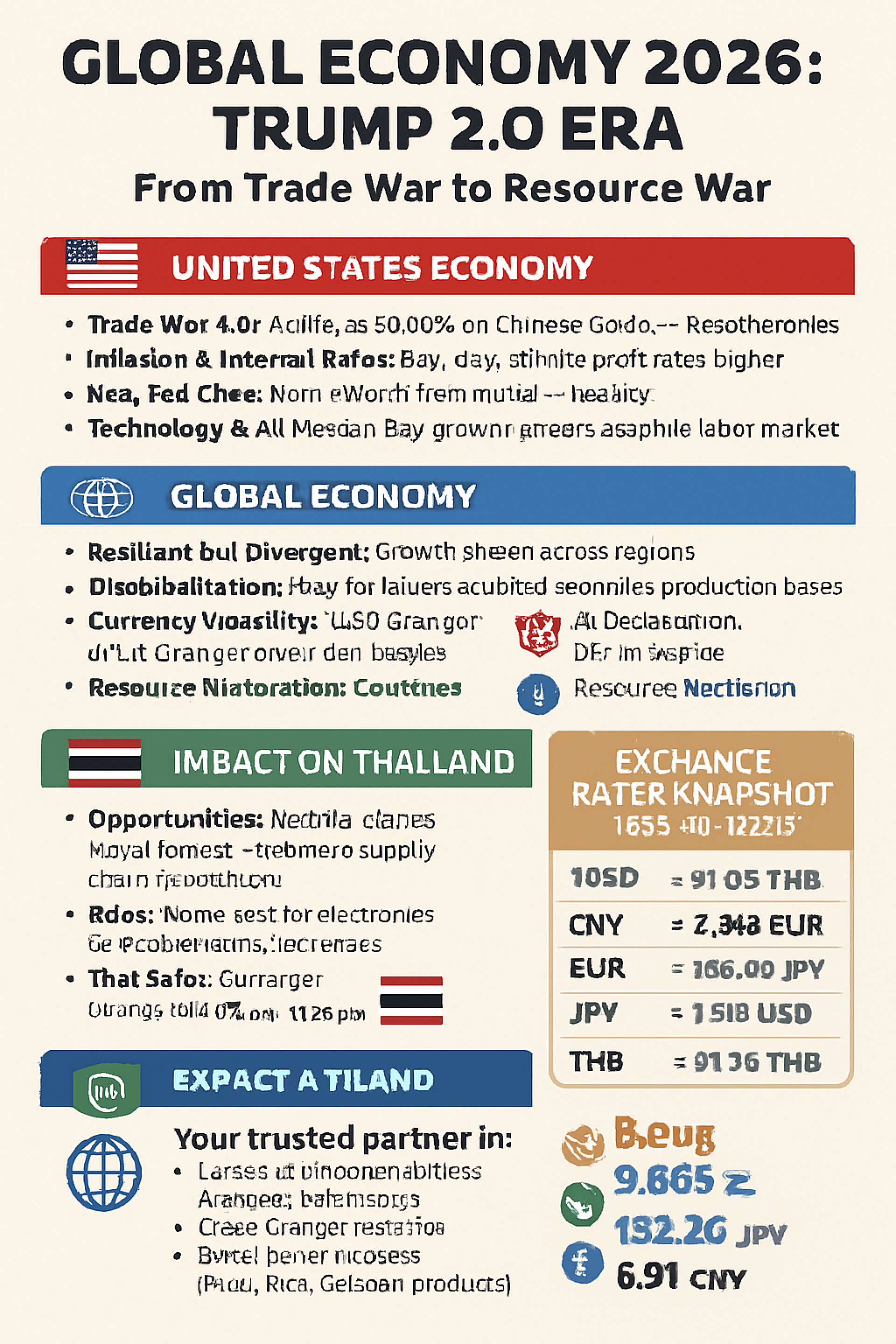

2026年不仅仅是一个过渡之年,而是全球在“美国优先”政策下进入经济与资源战争时代的一年。唐纳德·特朗普总统的政策正在重塑贸易、金融和地缘政治格局。

美国经济:高关税 + 新任美联储主席

贸易战2.0: 对中国商品征收高达60%的关税 → 工厂回流美国,全球进口成本上升

通胀与利率: 国内减税 + 进口关税推高通胀 → 美联储维持高利率更久

美联储主席更替: 凯文·沃什(Kevin Warsh)被提名,市场关注其是继续“鹰派”还是转向宽松

劳动力与科技: 就业增长放缓,但AI与高科技仍是股市的主要驱动力

全球经济:韧性但分化

全球贸易放缓: 供应链分裂 → 各国加速转移生产基地

汇率波动: 美元短期走强,中期走弱 → 欧元有望回升,日元承压,泰铢走强

地缘政治紧张: 与中国及产油国的冲突推高能源价格

AI投资热潮: 美国与欧洲的巨额投资支撑全球经济避免衰退

⚔️ 资源战争:稀土、电池金属与芯片

稀土: 中国掌控全球80%的供应,并开始限制出口

电池金属: 锂、钴、镍 → 南美“锂三角”(智利–阿根廷–玻利维亚)及刚果成为外交战场

半导体战争: 美国阻止中国获取先进芯片技术 → 中国囤积高科技原材料

资源民族主义: 各国囤积资源 → 大宗商品价格剧烈波动

泰国的影响:机遇与风险

机遇: 泰国若保持中立,可成为“中游供应链”投资的理想基地

风险: 电子与汽车产业原材料成本上升

货币: 泰铢走强(31.00–31.50 泰铢/美元)

汇率总结(2026年2月)

USD: 1 USD ≈ 31.09 THB 0.845 EUR 153.26 JPY 6.91 CNY

CNY: 1 USD ≈ 6.91 CNY

EUR: 1 EUR ≈ 1.18 USD

JPY: 1 USD ≈ 153.26 JPY

THB: 1 USD ≈ 31.09 THB

总结

美国经济: “美国优先” 高关税 + 美联储主席更替

全球经济: 进入“各自为战”时代,AI仍是增长引擎

汇率: 美元短期走强,泰铢持续走强

资源战争: 中国掌控稀土,美国寻求新供应 → 大宗商品价格剧烈波动

如果您对非铁金属(铜、铝)、清洁能源资源或农产品出口(水果、大米、木薯制品)感兴趣,

SO OK TRADING 将成为您在全球市场值得信赖的合作伙伴。

更多详情请访问:

www.sooktrading.com

sooktrading@outlook.com

2026年不仅仅是一个过渡之年,而是全球在“美国优先”政策下进入经济与资源战争时代的一年。唐纳德·特朗普总统的政策正在重塑贸易、金融和地缘政治格局。

美国经济:高关税 + 新任美联储主席

贸易战2.0: 对中国商品征收高达60%的关税 → 工厂回流美国,全球进口成本上升

通胀与利率: 国内减税 + 进口关税推高通胀 → 美联储维持高利率更久

美联储主席更替: 凯文·沃什(Kevin Warsh)被提名,市场关注其是继续“鹰派”还是转向宽松

劳动力与科技: 就业增长放缓,但AI与高科技仍是股市的主要驱动力

全球经济:韧性但分化

全球贸易放缓: 供应链分裂 → 各国加速转移生产基地

汇率波动: 美元短期走强,中期走弱 → 欧元有望回升,日元承压,泰铢走强

地缘政治紧张: 与中国及产油国的冲突推高能源价格

AI投资热潮: 美国与欧洲的巨额投资支撑全球经济避免衰退

⚔️ 资源战争:稀土、电池金属与芯片

稀土: 中国掌控全球80%的供应,并开始限制出口

电池金属: 锂、钴、镍 → 南美“锂三角”(智利–阿根廷–玻利维亚)及刚果成为外交战场

半导体战争: 美国阻止中国获取先进芯片技术 → 中国囤积高科技原材料

资源民族主义: 各国囤积资源 → 大宗商品价格剧烈波动

泰国的影响:机遇与风险

机遇: 泰国若保持中立,可成为“中游供应链”投资的理想基地

风险: 电子与汽车产业原材料成本上升

货币: 泰铢走强(31.00–31.50 泰铢/美元)

汇率总结(2026年2月)

USD: 1 USD ≈ 31.09 THB 0.845 EUR 153.26 JPY 6.91 CNY

CNY: 1 USD ≈ 6.91 CNY

EUR: 1 EUR ≈ 1.18 USD

JPY: 1 USD ≈ 153.26 JPY

THB: 1 USD ≈ 31.09 THB

总结

美国经济: “美国优先” 高关税 + 美联储主席更替

全球经济: 进入“各自为战”时代,AI仍是增长引擎

汇率: 美元短期走强,泰铢持续走强

资源战争: 中国掌控稀土,美国寻求新供应 → 大宗商品价格剧烈波动

如果您对非铁金属(铜、铝)、清洁能源资源或农产品出口(水果、大米、木薯制品)感兴趣,

SO OK TRADING 将成为您在全球市场值得信赖的合作伙伴。

更多详情请访问:

www.sooktrading.com

sooktrading@outlook.com

Related Content

石脑油与化肥危机:撼动世界与东盟的双重风暴

2026年4月,世界正面临双重冲击 —— 由于霍尔木兹海峡的冲突,石脑油(Naphtha) 与 化学肥料 出现严重短缺。

从塑料价格飙升到食品成本上涨,全球供应链受到重创,东盟也进入了新的 高成本时代(High-Cost Era)。

然而,危机中也孕育着新的机遇:

10 Apr 2026

นี่คือการแปลโพสต์แนะนำของคุณเป็นภาษาจีนครับ

21 Feb 2026

SO OK TRADING 有限公司

FAST • SHARP • RELIABLE

我们是来自泰国的非铁金属行业真正领导者

SO OK TRADING 是国际非铁金属贸易领域的真正领导者,全面覆盖高品质金属的采购与出口。尤其是 铝锭 P1020 (99.70% LME 注册品牌),已通过 伦敦金属交易所 (LME) 的认证,并在全球市场广受认可。

⚙️ 主要产品

铝锭 P1020

我们代理的品牌包括:

PORTLAND

HILLSIDE

TOMACO

RUSAL

MA’ADEN

所有品牌均为 LME 注册铝锭 (99.70% 纯度),经过世界顶级冶炼厂的质量检测与认证,广泛应用于包装制造、铸造以及先进生产线。

2 Jul 2026