NON‑FERROUS METALS 2026–2027: Fierce Battles in the Global Arena — Navigating War, Energy, and New Supply SO OK TRADING | 30 June 2026

Non-Ferrous Metals Market Outlook 2026–2027

The market is entering one of the most volatile periods in recent years. LME prices are swinging sharply under the pressure of war, trade tariffs, and speculative capital, forcing producers and investors to adopt cautious strategies.

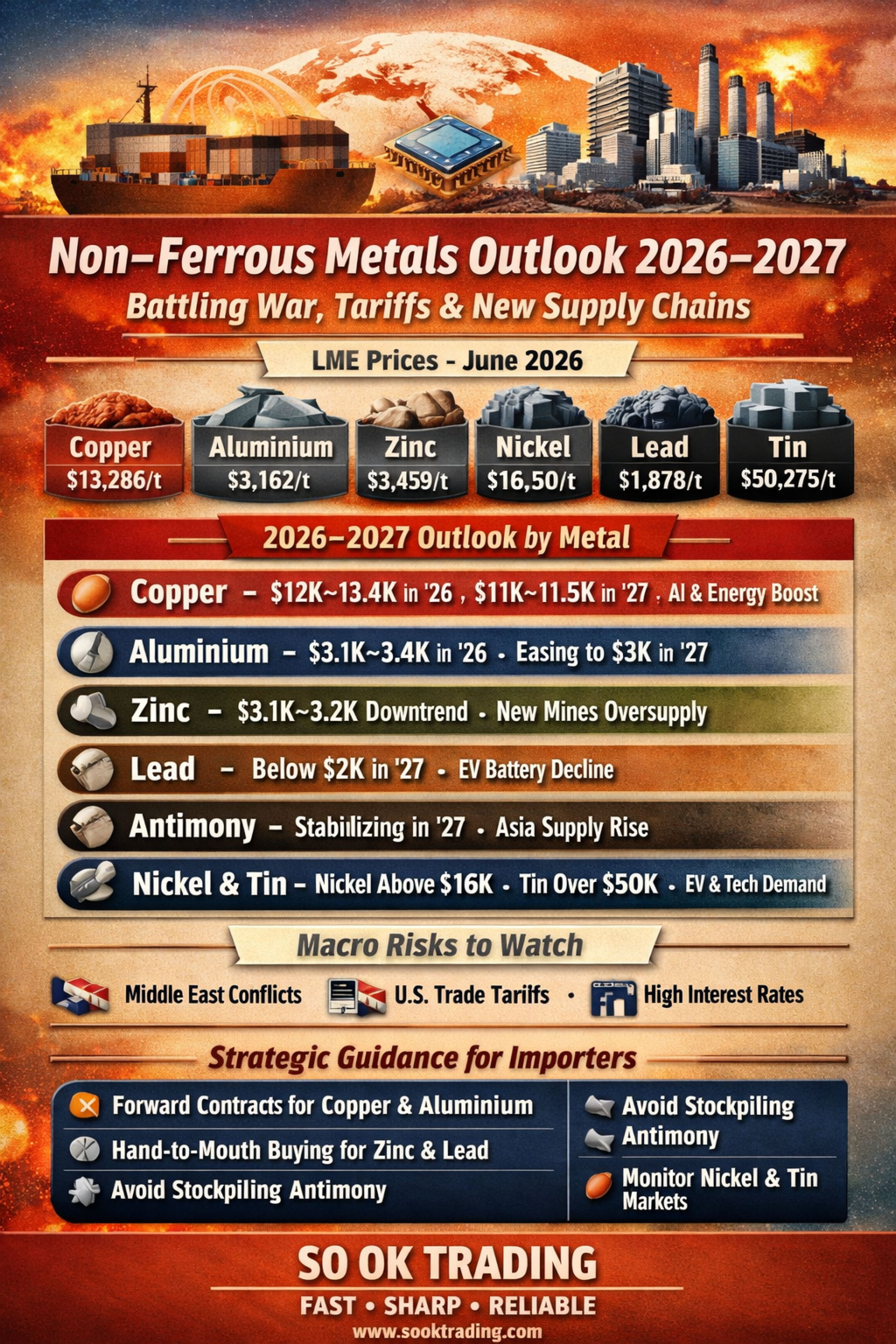

Latest Prices (June 2026 – LME Official Price)

Copper: $13,286/ton

Aluminium: $3,162/ton

Zinc: $3,459/ton

Nickel: $16,550/ton

Lead: $1,878/ton

Tin: $50,275/ton

Copper

July–Q3 2026: Trading in the high range of $12,000–$13,400/ton, supported by speculation and investment in AI data centers and power grids.

2027: Likely to correct to $11,000–$11,500/ton if U.S. tariff measures are clarified and global oversupply persists.

Supportive factors: Clean energy, power infrastructure, AI

Downside factors: U.S. tariff barriers, global surplus stocks

Aluminium

July–Q3 2026: Stable at $3,100–$3,400/ton, supported by soaring energy costs and declining LME stocks.

2027: Expected to correct to $3,000/ton as new supply from Indonesia enters and China eases production restrictions.

Supportive factors: Geopolitical risks, high energy costs

Downside factors: New capacity from Indonesia

Zinc

July 2026: Stable at $3,400–$3,500/ton.

Q3 2026: Sliding to $3,100–$3,200/ton as new mines come online worldwide.

2027: Persistently low due to oversupply.

Downside factors: Five new mines globally (Russia, Congo, China, etc.)

Lead

July–Q3 2026: Narrow range of $1,850–$1,950/ton.

2027: Continued decline as the transition to lithium-ion batteries accelerates.

Downside factors: EVs reducing lead-acid battery use, global stocks at highest since 2012

Antimony

July–Q3 2026: Ongoing correction after record highs in 2025.

2027: Expected to stabilize at a new base price as supply from Southeast Asia grows and China relaxes export restrictions.

Downside factors: New smelters, buyers delaying orders

Nickel & Tin

Nickel: Holding above $16,000/ton, supported by EV battery and stainless steel demand, but vulnerable to rising Indonesian supply.

Tin: Trading above $50,000/ton, driven by electronics and semiconductor demand, expected to remain high.

⚡ Macro Factors

Middle East war (Iran): Driving up energy costs and freight rates.

U.S. tariff measures (Section 232/301): Market volatility fueled by rumors and strategic stockpiling.

Global monetary policy: Fed’s high interest rates weigh on manufacturing recovery.

Strategic Recommendations (2026–2027)

The non-ferrous metals market is being driven more by war, tariffs, and speculative capital than by real demand. Cost management through price locking at order placement and Hand-to-Mouth purchasing will reduce risk and improve flexibility for Thai operators.

Copper & Aluminium: Use forward contracts/hedging when orders are confirmed; avoid chasing prices during spikes.

Zinc & Lead: Buy only as needed to minimize risk from price corrections.

Antimony: Avoid long-term stockpiling as new supply is entering the market.

Nickel & Tin: Monitor demand from EVs and electronics, which remain key drivers.

SO OK TRADING

Your Business Partner

FAST ・ SHARP ・ RELIABLE

VISIT US AT : WWW.SOOKTRADING.COM FACEBOOK : SO OK TRADING