“Hormuz Crisis 2026: From a Thousand Stranded Ships to Soaring Energy, Fertilizer, and Naphtha Costs Shaking Global Industries” BY SO OK TRADING – 28 APRIL 2026

Hormuz Strait Crisis 2026: From Energy to Global Supply Chains BY SO OK TRADING : 28 APRIL 2026

On April 28, 2026, the world is facing a major crisis at the Hormuz Strait. This strategic route, once the lifeline of oil and goods transport, has become a bottleneck that is shaking the global economy severely.

Although temporary routes have been announced, actual shipping has dropped by more than 90%, with only a handful of vessels per day compared to the previous average of 140. Over 1,000 ships are stranded, confidence in shipping companies has collapsed, while Iran continues strict inspections of vessels linked to the U.S. and Israel.

Freight rates and oil prices are soaring:

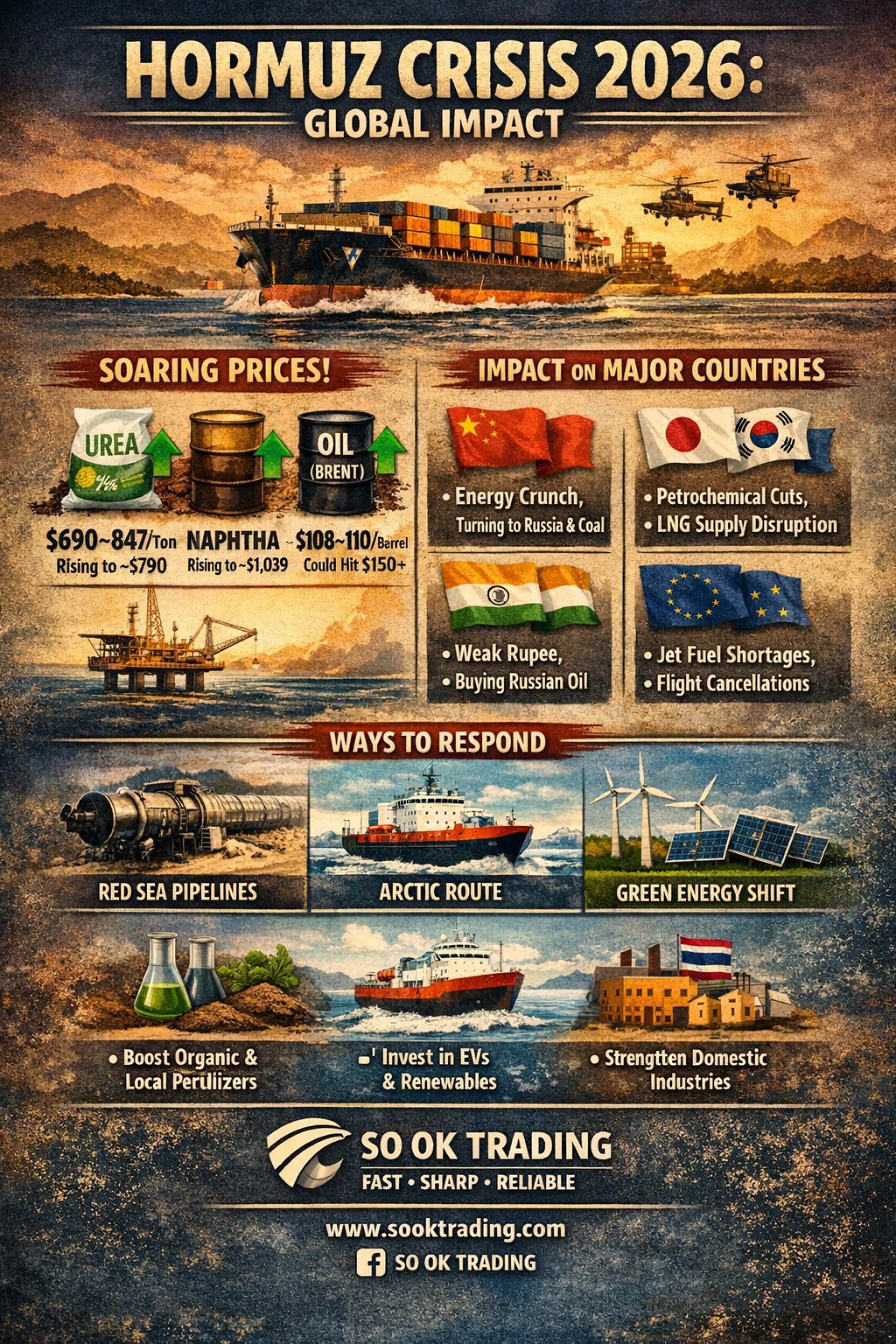

Container freight index (SCFI) is expected to surge to 1,600–1,900 points, with Thai operators facing costs 2–3 times higher

Global oil prices: Brent at $108.23–109.60 per barrel, WTI at $96.37–97.61 per barrel

⚡ Impact on supply chains: Naphtha and Urea Fertilizer

Naphtha: Prices in Asia surged ~30% within a month. Petrochemical plants in Japan, Korea, and Thailand face massive costs, with some declaring Force Majeure.

United States: Began exporting naphtha from the Atlantic coast to India, marking a historic shift in global trade flows.

Fertilizer: Urea prices jumped over 81%, reaching ~$702.25 per ton. Farmers in Brazil, India, and Thailand saw profits collapse. China continues its fertilizer export ban, worsening global shortages.

Parallel solutions: New trade routes and global shipping

New routes: Oil pipelines to the Red Sea and Gulf of Oman, Polar Silk Road

Energy beyond the Middle East: U.S. shale oil, oil from Brazil and Guyana, expansion in West Africa

Clean energy: EV boom, Green Hydrogen, Offshore Wind, Small Modular Nuclear Reactors

Price outlook for energy, fertilizer, and naphtha

Urea Fertilizer: Latest price ~$690–847/ton, likely to reach ~$790/ton within 12 months, up more than 50% year-on-year

Naphtha: Latest price ~$935/ton, expected to reach ~$1,039/ton within 12 months, up more than 70% year-on-year

Brent Crude: Latest price ~$108–110/barrel, Q2 2026 average expected at ~$110, with potential to surge to $150 if the crisis persists

Impact on major countries

China: Highly dependent on Middle Eastern imports of naphtha and oil, but shifting to Russia and coal-to-chemicals to cut costs. Large oil reserves provide resilience.

Japan & South Korea: Hit hardest, as nearly all naphtha and LNG are imported by sea. Petrochemical plants cut output by 20–30%. Inflation and high energy costs intensify.

India: Heavy reliance on imported energy, rising production costs, and currency depreciation. Importing cheap Russian oil to refine domestically and export naphtha to Europe.

United States: Benefits from shale oil and gas. Fertilizer plants running at full capacity, exporting to Europe and South America. Domestic oil prices remain high but adaptability is stronger.

Europe: Risks jet fuel shortages within six weeks if Hormuz remains closed. Airlines cancel flights and raise fuel surcharges. Facing the largest energy crisis in history.

Conclusion

Fertilizer and naphtha prices will remain high through the end of 2026, raising costs for food production and plastics globally.

Crude oil could reach $150/barrel if Hormuz remains closed into mid-year.

Energy-import-dependent countries (Japan, Korea, India, Thailand) will face the heaviest pressure.

Resource-rich countries (U.S., Russia, Brazil) will gain competitive advantage.

Thailand: Industrial sectors (PTTGC, SCC) and farmers will face sustained cost pressures. The government should accelerate promotion of alternative energy and organic fertilizers to reduce reliance on global markets.

SO OK TRADING : Your Business Partner SO OK TRADING : FAST SHARP RELIABLE