アルミニウム P1020 / A7 — EV・クリーンエネルギー・グローバル産業を支える戦略的金属 この高純度アルミニウムが単なる商品ではなく、未来の持続可能な経済の基盤である理由をご紹介します。 By SO OK TRADING

Last updated: 28 Jan 2026

2274 Views

アルミニウム P1020 / A7:持続可能な未来を支える戦略的金属

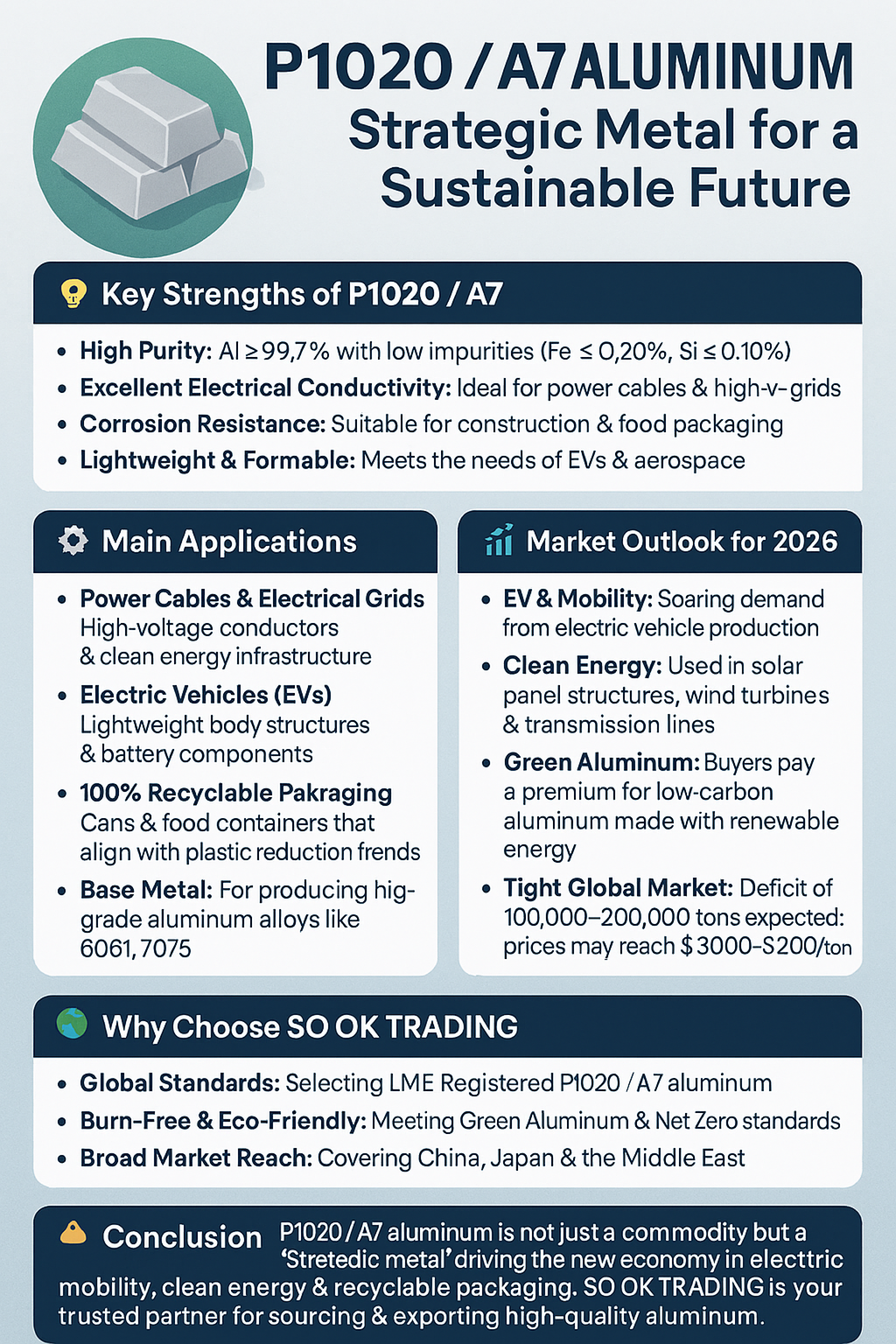

アルミニウム P1020 および A7 グレードは、純度 99.7%以上の「一次アルミニウムインゴット」として国際的に認められた標準です。LME や ASTM に登録され、電線から自動車産業、再生可能エネルギーまで幅広く利用されています。

P1020 / A7 の強み

高純度:Al ≥ 99.7%、不純物が極めて少ない (Fe ≤ 0.20%、Si ≤ 0.10%)

優れた導電性:高電圧送電線や電力インフラに最適

耐食性:建設資材や食品包装に適用可能

軽量で加工容易:EV や航空産業のニーズに対応

⚙️ 主な用途

電線・電力網:高電圧導体やクリーンエネルギー基盤

電気自動車 (EV):軽量ボディ構造やバッテリー部品

100% リサイクル可能な包装:缶や食品容器、脱プラスチックの潮流に対応

基材:6061、7075 など高強度アルミ合金の原料

2026 年の市場展望

EV & モビリティ:電気自動車の生産拡大による需要急増

クリーンエネルギー:太陽光パネル、風力タービン、送電線に利用

グリーンアルミニウム:再生可能エネルギーで製造された低炭素アルミにプレミアム価格

逼迫する世界市場:10万〜20万トンの供給不足予測、価格は 3,000〜3,200 ドル/トンに達する可能性

SO OK TRADING を選ぶ理由

✅ 国際基準品質:LME 登録ブランドの P1020 / A7 を厳選

✅ 焼畑ゼロ・環境配慮:グリーンアルミニウムや Net Zero に対応

✅ 広範な市場ネットワーク:中国、日本、中東をカバー

✅ ワンストップソリューション:調達から品質検査、輸出まで一貫対応

結論

アルミニウム P1020 / A7 は単なる商品ではなく、「戦略的金属」 として新しい経済を牽引します。電気自動車、クリーンエネルギー、リサイクル可能な包装の未来を支える存在です。

SO OK TRADING は、高品質アルミニウムの調達と輸出において信頼できるパートナーとして、産業の安定と持続可能な未来を実現します。

✨ SO OK TRADING — Pure Aluminum, Global Standards, Sustainable Future

アルミニウム P1020 および A7 グレードは、純度 99.7%以上の「一次アルミニウムインゴット」として国際的に認められた標準です。LME や ASTM に登録され、電線から自動車産業、再生可能エネルギーまで幅広く利用されています。

P1020 / A7 の強み

高純度:Al ≥ 99.7%、不純物が極めて少ない (Fe ≤ 0.20%、Si ≤ 0.10%)

優れた導電性:高電圧送電線や電力インフラに最適

耐食性:建設資材や食品包装に適用可能

軽量で加工容易:EV や航空産業のニーズに対応

⚙️ 主な用途

電線・電力網:高電圧導体やクリーンエネルギー基盤

電気自動車 (EV):軽量ボディ構造やバッテリー部品

100% リサイクル可能な包装:缶や食品容器、脱プラスチックの潮流に対応

基材:6061、7075 など高強度アルミ合金の原料

2026 年の市場展望

EV & モビリティ:電気自動車の生産拡大による需要急増

クリーンエネルギー:太陽光パネル、風力タービン、送電線に利用

グリーンアルミニウム:再生可能エネルギーで製造された低炭素アルミにプレミアム価格

逼迫する世界市場:10万〜20万トンの供給不足予測、価格は 3,000〜3,200 ドル/トンに達する可能性

SO OK TRADING を選ぶ理由

✅ 国際基準品質:LME 登録ブランドの P1020 / A7 を厳選

✅ 焼畑ゼロ・環境配慮:グリーンアルミニウムや Net Zero に対応

✅ 広範な市場ネットワーク:中国、日本、中東をカバー

✅ ワンストップソリューション:調達から品質検査、輸出まで一貫対応

結論

アルミニウム P1020 / A7 は単なる商品ではなく、「戦略的金属」 として新しい経済を牽引します。電気自動車、クリーンエネルギー、リサイクル可能な包装の未来を支える存在です。

SO OK TRADING は、高品質アルミニウムの調達と輸出において信頼できるパートナーとして、産業の安定と持続可能な未来を実現します。

✨ SO OK TRADING — Pure Aluminum, Global Standards, Sustainable Future

関連コンテンツ

「鉄鋼価格戦争2026:アジアは下落、西側は高騰。タイは買い手として優位に立つ一方、生産者は新たな戦略で生き残りをかける ― 世界市場の二極化とグリーンスチールの可能性を分析」

世界の鉄鋼市場は、今年最も激しい「二極化の戦局」に突入しています。

アジア:供給過剰と中国の需要減退により価格が急落。鉄鉱石は1トンあたり約101〜102ドルまで下落。

西側諸国:米国と欧州は輸入関税を最大50%に引き上げ、さらにエネルギーとコークス炭のコストが16%上昇し、価格は逆に高騰。

タイ市場の現状:

買い手に有利:中国やベトナムからの安価な鋼材流入で小売価格は8%以上下落。

生産者は苦境:電力・輸送コストが50%以上急騰し、利益率が圧迫。反ダンピングやCBAMなどの政策支援が不可欠。

金属包装材(ティンプレート):販売は -1.2%〜-4.5% 減少したものの、原材料コストは9〜10%低下。さらにリサイクル率92%という強みで、ESGやグリーンスチールの潮流に合致。

5 Jun 2026

An analysis of the aluminum market in 2026 indicates a likely continued market deficit and upward price pressure, driven by constrained supply and resilient demand from green energy sectors. However, significant volatility is expected due to policy uncertainties and the potential for new Indonesian supply to eventually balance the market.

Key Drivers and Projections for 2026

Supply Side Analysis

Capacity Constraints: China's primary aluminum output is approaching its self-imposed 45 million-tonne capacity cap, limiting global supply growth.

Power Challenges: Smelters outside of China face intense competition for power from energy-intensive sectors like AI data centers, which are willing to pay higher prices for long-term contracts. This has kept significant capacity offline in Europe and the US.

Production Disruptions: Outages and potential shutdowns at existing smelters in Iceland and Mozambique further tighten the market.

Scrap Supply Pressure: The EU's planned implementation of the Carbon Border Adjustment Mechanism (CBAM) and potential scrap export tariffs in spring 2026 are expected to impact global scrap flows, creating regional shortages and price volatility.

New Capacity: Indonesia is a key source of new supply, with several projects in the pipeline. However, analysts suggest the pace of the ramp-up may be slower than expected due to infrastructure and policy challenges, meaning it is unlikely to fully offset near-term tightness.

Demand Side Analysis

Green Transition Demand: Demand from "green" sectors such as solar panels, new energy vehicles, and energy transition infrastructure remains strong, providing fundamental support for the market.

Substitution Effect: Aluminum's wide price discount relative to copper has encouraged substitution in electrical applications, acting as a tailwind for demand and prices.

Construction and Automotive: The construction and automotive industries continue to be major consumers, with growing demand for lightweight, low-carbon aluminum products.

Price Forecasts and Volatility

The market is expected to remain in a deficit in 2026, with estimates ranging from 200,000 to 600,000 tonnes. This structural tightness is leading most analysts to forecast sustained or rising prices.

Bullish Views: Analysts at Bank of America project prices of $3,000/tonne as early as 2026. J.P. Morgan also expects prices to approach $3,000/tonne in Q1 2026. ING forecasts an average price of $2,900/tonne for the year.

Bearish/Conservative Views: Goldman Sachs is an outlier, forecasting prices to decline to $2,350/tonne by Q4 2026, anticipating a market surplus later in the year. SMM forecasts a "high first, then lower" pattern, with prices finding equilibrium in the $2,700–$2,800/tonne range by year-end.

Premiums: Regional premiums, particularly the US Midwest premium, are expected to remain high and volatile due to tariffs and regional supply dynamics, creating a disconnect from the LME benchmark price.

In essence, 2026 is projected to be a year of high volatility where participants need to focus on scenario readiness rather than relying on a single price forecast, as geopolitical and energy policies significantly influence regional supply and costs

31 Dec 2025