アルミニウム P1020 / A7 — EV・クリーンエネルギー・グローバル産業を支える戦略的金属 この高純度アルミニウムが単なる商品ではなく、未来の持続可能な経済の基盤である理由をご紹介します。 By SO OK TRADING

Last updated: 28 Jan 2026

1931 Views

アルミニウム P1020 / A7:持続可能な未来を支える戦略的金属

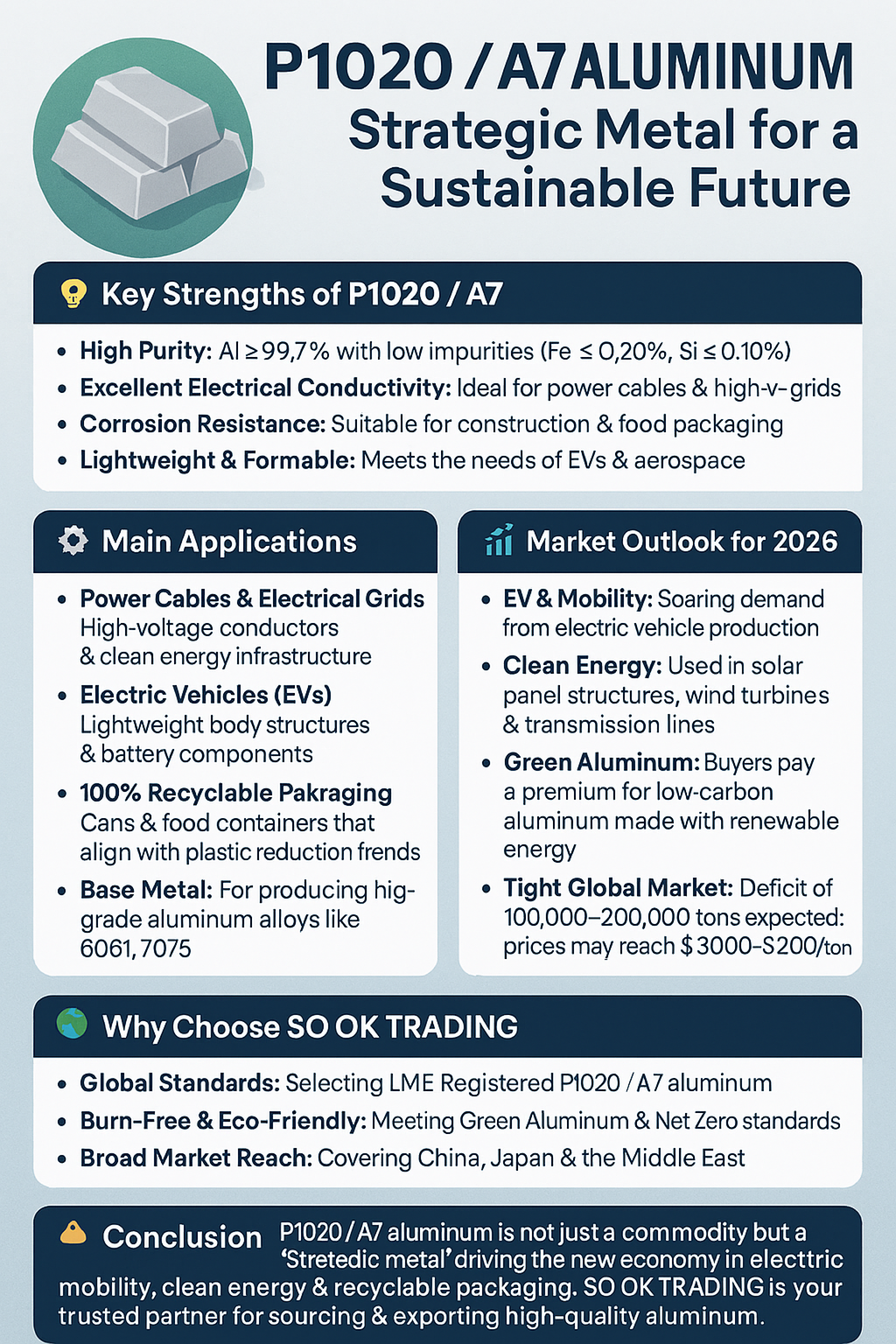

アルミニウム P1020 および A7 グレードは、純度 99.7%以上の「一次アルミニウムインゴット」として国際的に認められた標準です。LME や ASTM に登録され、電線から自動車産業、再生可能エネルギーまで幅広く利用されています。

P1020 / A7 の強み

高純度:Al ≥ 99.7%、不純物が極めて少ない (Fe ≤ 0.20%、Si ≤ 0.10%)

優れた導電性:高電圧送電線や電力インフラに最適

耐食性:建設資材や食品包装に適用可能

軽量で加工容易:EV や航空産業のニーズに対応

⚙️ 主な用途

電線・電力網:高電圧導体やクリーンエネルギー基盤

電気自動車 (EV):軽量ボディ構造やバッテリー部品

100% リサイクル可能な包装:缶や食品容器、脱プラスチックの潮流に対応

基材:6061、7075 など高強度アルミ合金の原料

2026 年の市場展望

EV & モビリティ:電気自動車の生産拡大による需要急増

クリーンエネルギー:太陽光パネル、風力タービン、送電線に利用

グリーンアルミニウム:再生可能エネルギーで製造された低炭素アルミにプレミアム価格

逼迫する世界市場:10万〜20万トンの供給不足予測、価格は 3,000〜3,200 ドル/トンに達する可能性

SO OK TRADING を選ぶ理由

✅ 国際基準品質:LME 登録ブランドの P1020 / A7 を厳選

✅ 焼畑ゼロ・環境配慮:グリーンアルミニウムや Net Zero に対応

✅ 広範な市場ネットワーク:中国、日本、中東をカバー

✅ ワンストップソリューション:調達から品質検査、輸出まで一貫対応

結論

アルミニウム P1020 / A7 は単なる商品ではなく、「戦略的金属」 として新しい経済を牽引します。電気自動車、クリーンエネルギー、リサイクル可能な包装の未来を支える存在です。

SO OK TRADING は、高品質アルミニウムの調達と輸出において信頼できるパートナーとして、産業の安定と持続可能な未来を実現します。

✨ SO OK TRADING — Pure Aluminum, Global Standards, Sustainable Future

アルミニウム P1020 および A7 グレードは、純度 99.7%以上の「一次アルミニウムインゴット」として国際的に認められた標準です。LME や ASTM に登録され、電線から自動車産業、再生可能エネルギーまで幅広く利用されています。

P1020 / A7 の強み

高純度:Al ≥ 99.7%、不純物が極めて少ない (Fe ≤ 0.20%、Si ≤ 0.10%)

優れた導電性:高電圧送電線や電力インフラに最適

耐食性:建設資材や食品包装に適用可能

軽量で加工容易:EV や航空産業のニーズに対応

⚙️ 主な用途

電線・電力網:高電圧導体やクリーンエネルギー基盤

電気自動車 (EV):軽量ボディ構造やバッテリー部品

100% リサイクル可能な包装:缶や食品容器、脱プラスチックの潮流に対応

基材:6061、7075 など高強度アルミ合金の原料

2026 年の市場展望

EV & モビリティ:電気自動車の生産拡大による需要急増

クリーンエネルギー:太陽光パネル、風力タービン、送電線に利用

グリーンアルミニウム:再生可能エネルギーで製造された低炭素アルミにプレミアム価格

逼迫する世界市場:10万〜20万トンの供給不足予測、価格は 3,000〜3,200 ドル/トンに達する可能性

SO OK TRADING を選ぶ理由

✅ 国際基準品質:LME 登録ブランドの P1020 / A7 を厳選

✅ 焼畑ゼロ・環境配慮:グリーンアルミニウムや Net Zero に対応

✅ 広範な市場ネットワーク:中国、日本、中東をカバー

✅ ワンストップソリューション:調達から品質検査、輸出まで一貫対応

結論

アルミニウム P1020 / A7 は単なる商品ではなく、「戦略的金属」 として新しい経済を牽引します。電気自動車、クリーンエネルギー、リサイクル可能な包装の未来を支える存在です。

SO OK TRADING は、高品質アルミニウムの調達と輸出において信頼できるパートナーとして、産業の安定と持続可能な未来を実現します。

✨ SO OK TRADING — Pure Aluminum, Global Standards, Sustainable Future

関連コンテンツ

「アルミニウム:未来の産業金属」

普通の素材から、EVとグリーン産業の心臓へ

アルミニウムはもはや単なる産業用金属ではなく、世界経済の新しい血流となりつつあります。特に以下の4つの主要グレードが産業を牽引しています:

19 Mar 2026