Aluminum Price Outlook – February 2026 SO OK TRADING Insight

Aluminum Price Outlook – February 2026

SO OK TRADING Insight

Global Market Overview

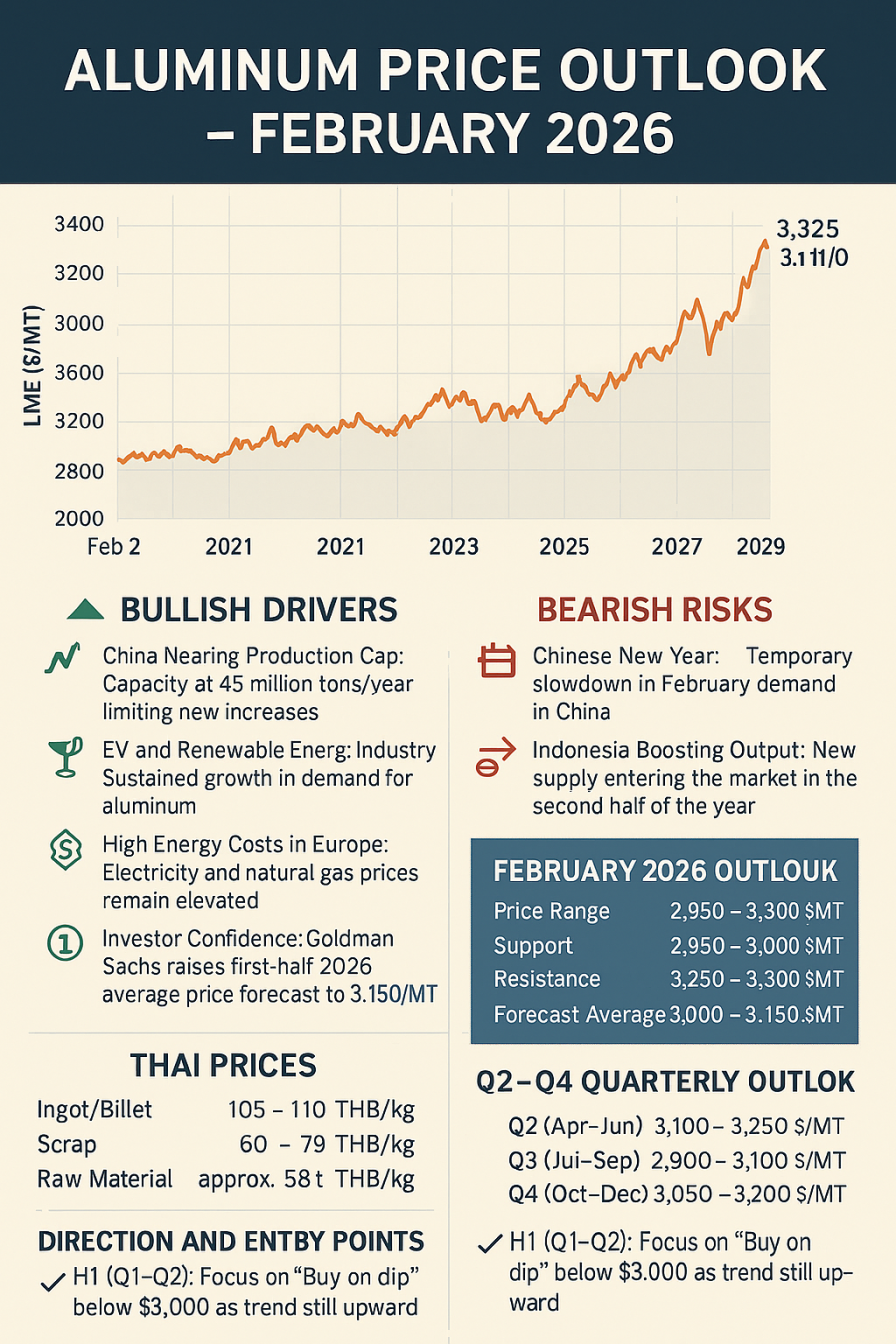

Aluminum prices remain elevated. On January 29, prices surged to USD 3,325/MT, the highest level in nearly four years, before closing at USD 3,110/MT on January 30. This marks a +8.78% increase in just four weeks, reflecting strong investor confidence and tightening supply.

Bullish Drivers

China near production cap: Output approaching 45 million tons/year limits new supply.

EV & renewable energy demand: Structural growth continues to support consumption.

High energy costs in Europe: Elevated electricity and natural gas prices push smelting costs higher.

Investor confidence: Goldman Sachs raised its H1 2026 average forecast to USD 3,150/MT.

Bearish Risks

Chinese New Year slowdown: Temporary demand dip in February.

Indonesia’s new supply: Additional capacity expected to ease tightness in H2 2026.

February 2026 Price Outlook

Range: USD 2,950 – 3,300/MT

Support: USD 2,950 – 3,000/MT

Resistance: USD 3,250 – 3,300/MT

Forecast Average: USD 3,000 – 3,150/MT

Thai Market Reference: Ingot/Billet 105–110 THB/kg Scrap 60–70 THB/kg Raw material ~98 THB/kg

Quarterly Outlook 2026

Q1 (Jan–Mar): USD 3,000 – 3,150 → High but consolidating

Q2 (Apr–Jun): USD 3,100 – 3,250 → Demand rebound + EV/renewables peak season

Q3 (Jul–Sep): USD 2,900 – 3,100 → Indonesia supply enters market

Q4 (Oct–Dec): USD 3,050 – 3,200 → Seasonal winter demand + year-end production push

Strategic Entry Points

H1 (Q1–Q2): Focus on Buy on dip below USD 3,000 as the uptrend remains intact.

H2 (Q3–Q4): Monitor Indonesia and China’s new capacity; consider long-term contracts if supply expands significantly.

✨ Summary: Aluminum prices are expected to remain above USD 3,000/MT throughout February 2026, with short-term consolidation after January’s rally. Strong demand from EV and renewable energy sectors, combined with limited supply growth, keeps the market resilient. Price dips below USD 3,000 present attractive stocking opportunities, while the second half of the year requires close monitoring of new supply flows.