“RDF Transforms Waste into Thailand’s Clean Energy Future — Igniting the Economy and Driving the Transition to Renewable Power” SO OK TRADING: June 13, 2026

RDF – Waste-Derived Fuel and the Future of Renewable Energy in Thailand By SO OK TRADING | June 13, 2026

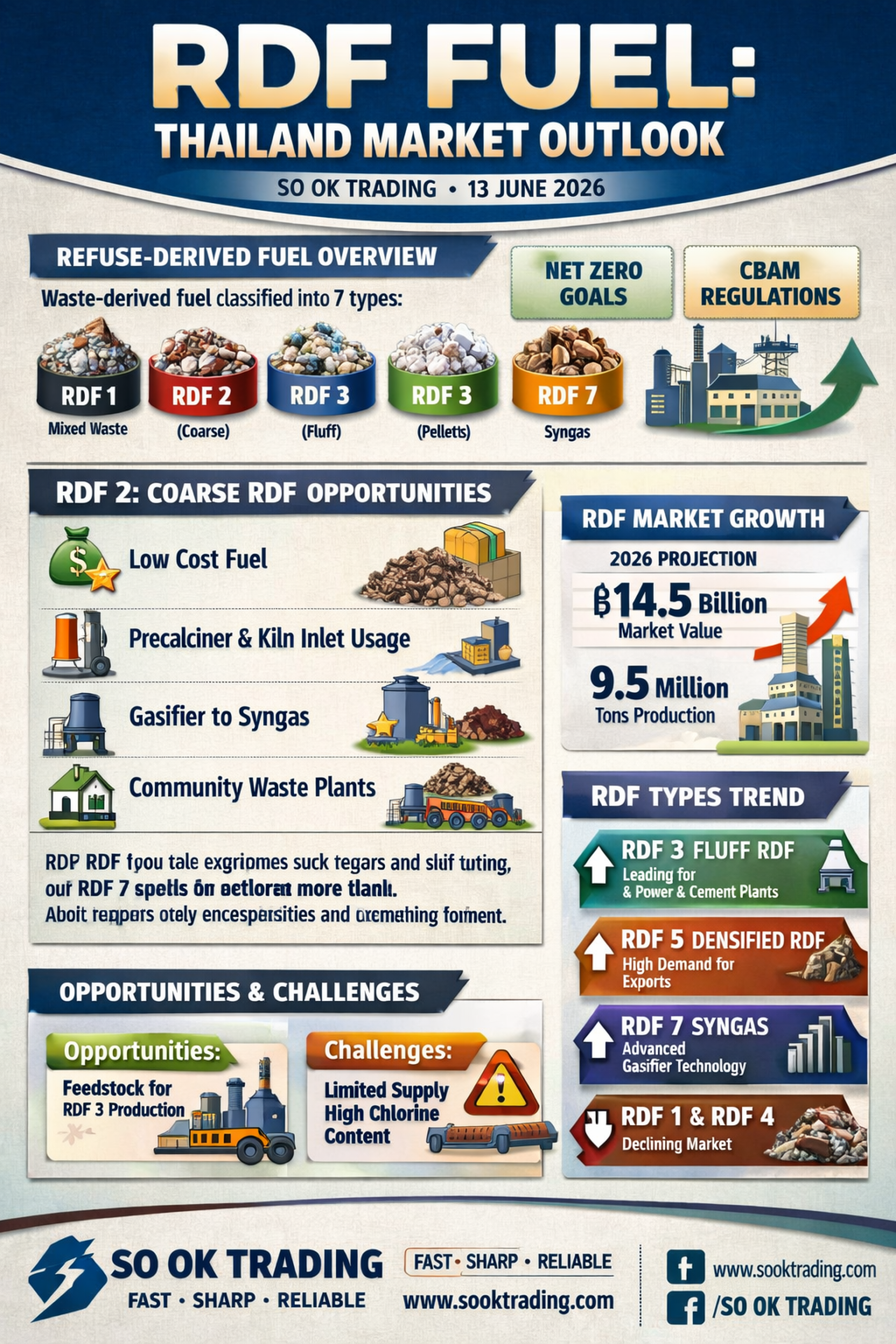

Overview of RDF and Its Role in Industry

Refuse-Derived Fuel (RDF) is fuel produced from municipal solid waste, sorted and processed to make it suitable for combustion. According to ASTM standards, RDF is classified into seven types, from RDF 1 (coarse, hand-sorted waste) to RDF 7 (Syngas), each with different particle sizes and applications.

In Thailand, RDF is becoming a key alternative fuel, reducing reliance on coal and oil while aligning with Net Zero Carbon policies and Europe’s CBAM regulations that require industries to cut carbon emissions.

⚙️ RDF 2 (Coarse RDF) – Strengths and Opportunities

Low cost: Requires less machinery and energy compared to fine shredding.

Suitable for Precalciner and Kiln Inlet: At 900–1,100°C, RDF 2 can achieve complete combustion.

Gasifier compatibility: RDF 2 can be converted into Syngas before entering the kiln, ensuring cleaner combustion.

Local economic model: Municipalities and community waste facilities can produce RDF 2 and supply it to central plants for further processing into RDF 3.

Although RDF 3 is the mainstream choice, RDF 2 is gaining importance due to economic advantages and plant design flexibility.

Outlook for Other RDF Types

RDF 3 (Fluff RDF): Fastest-growing in Thailand, used in waste-to-energy plants (~64% of the market) and major cement producers (SCG, TPIPL, INSEE) as a coal substitute.

RDF 5 (Densified RDF): Highly popular for its ease of transport and consistent quality, ideal for exports and standardized fuel needs.

RDF 7 (Syngas): Advanced technology under close watch; cement plants and waste-to-energy facilities are investing in Gasifiers to convert coarse RDF into Syngas, reducing emissions.

RDF 1 and RDF 4: Declining in demand due to difficulties in controlling heating value and moisture content.

Thailand’s RDF Industry Direction

Market expansion: By 2026, Thailand’s RDF market is projected to reach ฿14.5 billion with production exceeding 9.5 million tons.

Industrial standards (TIS): Stricter quality requirements mean low-grade RDF will struggle to find buyers.

Plastic feedstock competition: High-calorific plastics (PE, PP, PS, 6,000–8,000 kcal/kg) are in high demand as coal substitutes.

Chlorine issue: PVC and food waste introduce chlorine, causing equipment corrosion. Advanced sorting technologies such as optical sorters are needed.

New business opportunities: Investment in high-quality sorting and drying systems can elevate RDF into premium fuel markets.

⚖️ Opportunities and Challenges

Opportunities: RDF 2 can be produced locally and supplied to RDF 3 processing plants or directly used in Precalciner systems.

Challenges: Thailand’s waste segregation remains insufficient, leading to supply shortages, while high chlorine content continues to corrode industrial equipment.

Strategic Summary

RDF is no longer just “fuel from waste” — it is the heart of Thailand’s energy transition.

RDF 2: Evolving from low-cost coarse fuel into a strategic raw material.

RDF 3 and RDF 5: Standard fuels driving power plants and cement industries.

RDF 7: Future technology enabling cleaner energy and reduced emissions.

Companies that can control quality, reduce chlorine, and increase heating value will dominate Thailand’s RDF market in this new era, where competition is based on standards and quality, not just price.

SO OK TRADING Your trusted business partner FAST • SHARP • RELIABLE www.sooktrading.com Facebook: SO OK TRADING

Interested in RDF3 fuel? Contact SO OK TRADING — we are ready to serve you.