“War Shakes the Global Packaging Industry: Supply Chain Disruption, Plastic Shortage & Aluminum Squeeze – From Crisis to New Business Opportunities” Article by SO OK TRADING | March 26, 2026

ได้เลยครับ Mongkol — ผมช่วยแปลบทความนี้เป็นภาษาอังกฤษให้ครบถ้วนและยังคงโทนทางการตลาดที่ทรงพลังดังนี้ครับ:

“War Reshapes the Packaging Industry – Plastic Stumbles, Aluminum Faces Shortages”

The Middle East conflict has triggered a petrochemical crisis that continues to ripple into the global packaging industry. Supply chain disruption is no longer distant—it is becoming a reality that must be closely monitored.

Article by SO OK TRADING | March 26, 2026

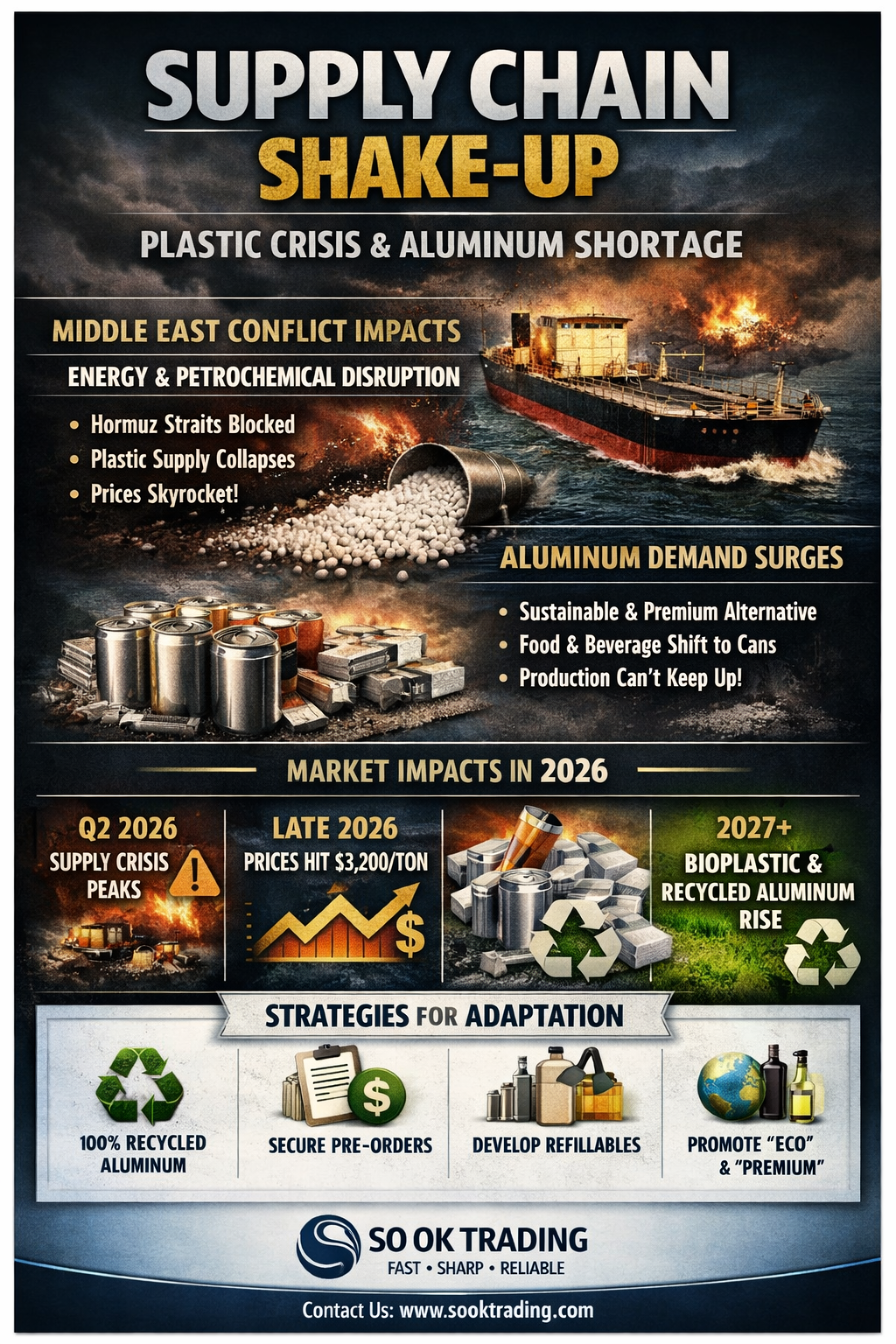

⚔️ War and Its Impact on Plastic

Hormuz Strait Blocked: Oil and petrochemical shipments halted, forcing many factories to suspend plastic resin production.

Rapid Stock Decline: In Thailand and Southeast Asia, plastic resin stockpiles are only sufficient until April–May 2026.

“Money Can’t Buy It”: Even with buyers willing to pay, supply cannot reach the market, creating a severe packaging plastic shortage.

Aluminum Packaging as the Alternative

100% Recyclable: Fully reusable, meeting ESG and Net Zero requirements.

Premium Image: Aluminum cans and packaging are perceived as more eco-friendly and upscale than plastic bottles.

Demand Surge: Food, beverage, and cosmetics industries are rapidly shifting to aluminum.

Aluminum Packaging Shortage Emerges

Transport Disruptions: Aluminum shipments from the Middle East face the same bottlenecks as plastics.

Production Capacity Shortfall: Middle Eastern smelters partially offline, reducing supply.

High Energy Costs: Aluminum smelting consumes vast electricity; European and Asian plants cut output.

Price Spike: Aluminum prices hit $3,200 per ton, the highest in years, burdening packaging producers.

Market Outlook 2026

Q2 2026: Peak supply crunch—both plastic and aluminum in shortage simultaneously.

Late 2026: Some stabilization, but prices remain higher than the previous year.

2027+: Market enters a “new balance” with recycled aluminum and bioplastics taking permanent market share.

Opportunities for Producers and Users

Shift to Green Packaging: Use recycled aluminum to differentiate and mitigate cost risks.

Secure Forward Contracts: Lock in prices and supply to hedge against volatility.

Develop Refillable Packaging: Enhance sustainability and reduce reliance on virgin materials.

Positive Consumer Communication: Turn crisis into opportunity by promoting “Eco-Friendly” and “Premium” packaging with NEO (Natural Plastic) or 100% recycled aluminum.

✨ Conclusion

This war has not eliminated plastic, but transport and energy costs have become major obstacles, pushing industries toward aluminum. Yet as demand outpaces supply, aluminum itself faces shortages.

This is a golden opportunity to pivot toward recycled packaging and innovation. In a world where supply chain disruption is the new normal, sustainable and circular materials will be the key to survival for the packaging industry.

SO OK TRADING: Your Trusted Business Partner

FAST • SHARP • RELIABLE

www.sooktrading.com