“Thai Wood Pellets: From Rubber Plantations to Global Clean Energy – Golden Export Opportunities to Japan, Europe, and South Korea” Article by SO OK TRADING | March 23, 2026

“Thai Wood Pellets: Clean Energy from Asia to the Global Stage”

Article by SO OK TRADING | March 23, 2026

Accelerating Toward Net Zero 2050

Thai biomass wood pellets are emerging as one of Asia’s most promising clean energy commodities, steadily building recognition in the global market.

Explosive Growth

In 2023, Thailand exported 207,000 tons of wood pellets, a 55% increase from 2022

Total export value exceeded USD 29 million

Key markets: South Korea (141,300 tons), Japan, and the Netherlands (57,500 tons)

Regional Market Trends

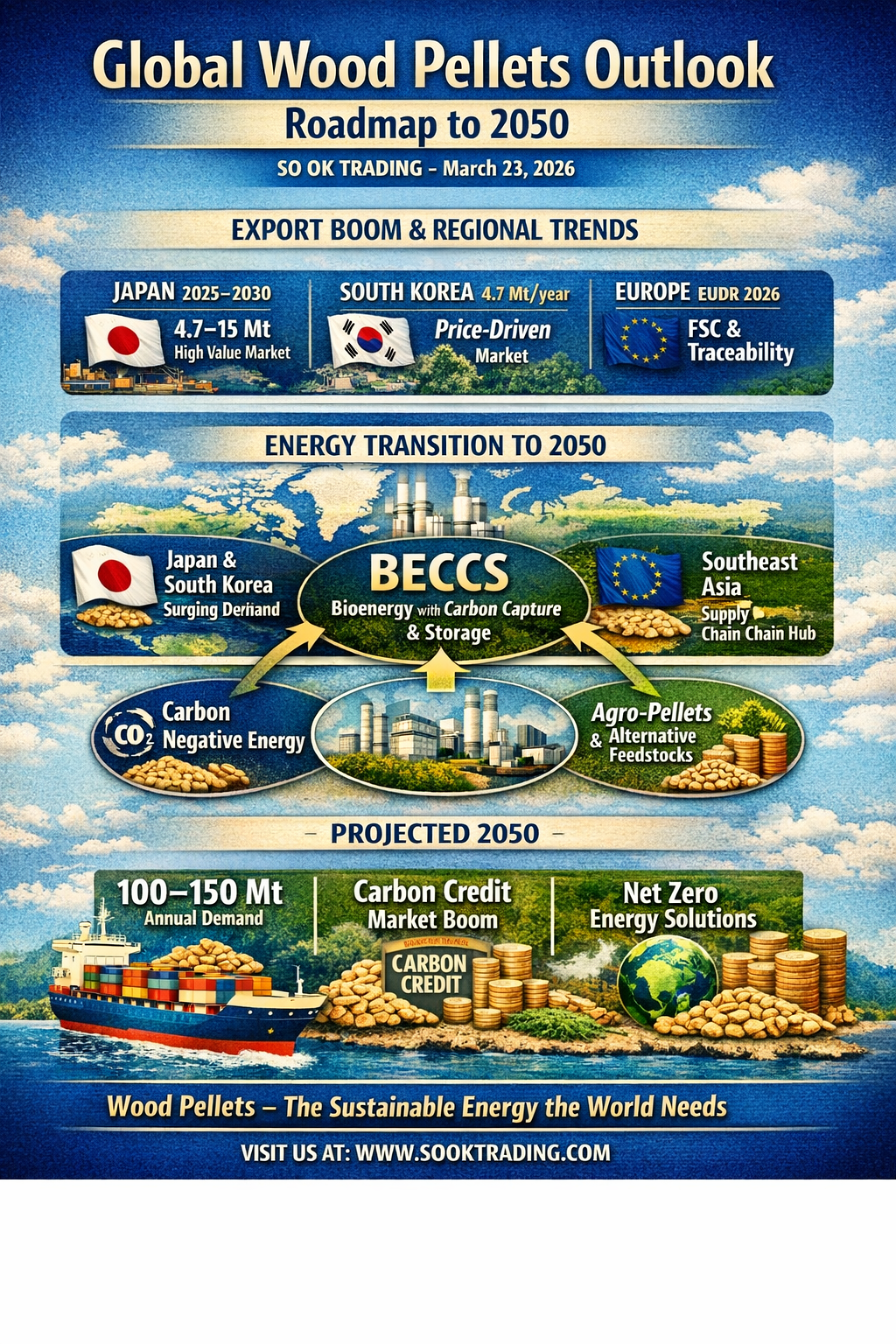

➡ Japan – Asia’s Golden Opportunity

Demand surging as coal-fired plants transition to biomass co-firing

Projected demand: 4.7 million tons by 2025, potentially reaching 15 million tons by 2030

Government continues FiT/FiP support at 24 yen/kWh

Main competitors: Vietnam and Canada, but Thailand is gaining ground

➡ South Korea – A Mature Market

Stable demand at 4.7 million tons/year

Highly price-competitive, with Vietnam holding 63% market share

Thailand must minimize freight costs to maintain competitiveness

➡ Europe – The Market of Sustainability

Recovering from slowdown in 2023–2024

EUDR regulations (effective 2026) require geolocation traceability of raw materials

Netherlands: hub for industrial-grade pellets

Germany & France: premium A1 grade for household heating

➡ Southeast Asia – The World’s Energy Kitchen

Vietnam: world’s No. 2 exporter, controlling 80% of Asia’s market

Indonesia: massive co-firing plans, domestic demand projected at 10.23 million tons/year by 2030

Thailand: current production ~1.2 million tons/year, with raw material potential up to 5.23 million tons/year if fully optimized

➡ North America & Europe

USA & Canada: largest producers globally, supply projected to exceed 31 million tons/year by 2030

Europe: despite strong domestic production, environmental regulations increase reliance on imports from tropical countries

Standards – The Key to Success

ENplus / DINplus: certify combustion quality

FSC / PEFC: ensure wood comes from plantations, not deforestation

EUDR (EU): require precise geolocation of raw materials

Long-Term Outlook

2025–2035: peak demand from Japan & Europe

2035–2050: transition to BECCS (Bioenergy with Carbon Capture & Storage), making wood pellets “carbon-negative energy”

2050: global consumption may reach 100–150 million tons/year

Demand–Supply Summary

Japan = High Value Market → Long-term contracts, premium pricing

South Korea = Market Share Maintenance → Compete via freight costs

Europe = Future Market → FSC + traceability standards essential

Southeast Asia = Supply Hub → Thailand must raise standards to compete with Vietnam

Wood Pellets – Thai biomass is not just fuel, but “the sustainable energy the world needs.”

SO OK TRADING: Your Partner in Global Business

FAST. SHARP. RELIABLE.

Visit us at: www.sooktrading.com

Contact: SOOKTRADING@OUTLOOK.COM

We are ready to serve you.

")