Nickel: The Strategic Metal of the Clean Energy Future — An Article by SO OK TRADING

Nickel: The Strategic Metal of the Clean Energy Future ⚡

Nickel (Ni) is shifting its role from a traditional heavy industry metal to the core of the clean energy transition. Especially in electric vehicles (EVs) and energy storage systems (ESS), nickel will shape the global economy over the next 10–20 years.

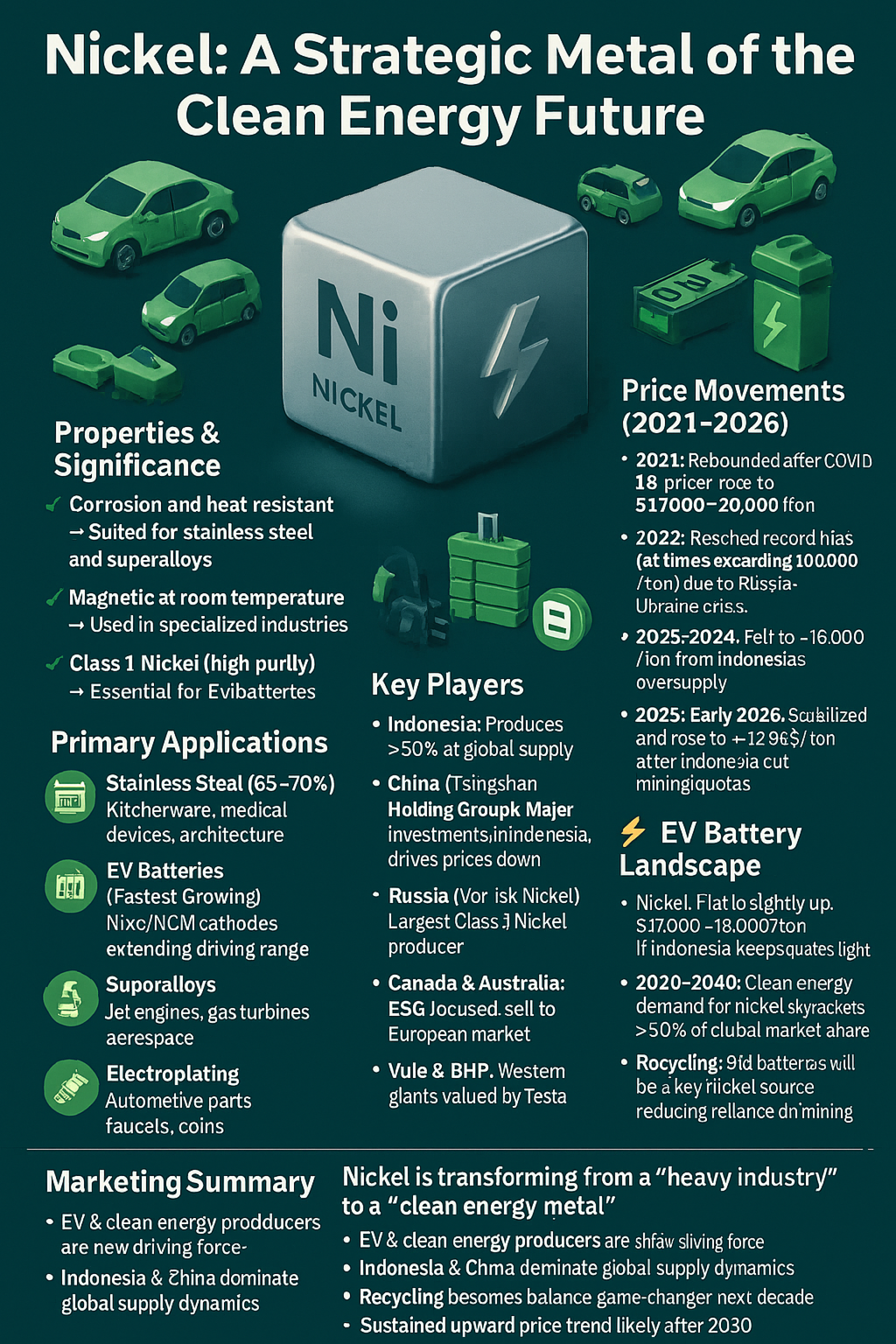

Properties & Significance

Corrosion and heat resistant → Ideal for stainless steel and superalloys

Magnetic at room temperature → Used in specialized industries

Class 1 Nickel (high purity) → Essential raw material for EV batteries

Price Movements (2021–2026)

2021: Post-COVID recovery, prices rose to $17,000–20,000/ton

2022: Historic spike (at times exceeding $100,000/ton) due to Russia–Ukraine crisis

2023–2024: Fell to ~$16,000/ton from Indonesia’s oversupply

2025–Early 2026: Stabilized and rebounded to ~$17,963/ton after Indonesia cut mining quotas

Primary Applications

Stainless Steel (65–70%): Kitchenware, medical devices, architectural structures

EV Batteries (fastest-growing): NMC/NCM cathodes, extending driving range

Superalloys: Jet engines, gas turbines, aerospace industry

Electroplating: Automotive parts, faucets, coins

Chemical Industry: Catalysts in oil refining and chemical processes

Major Players

Indonesia: Produces >50% of global supply

China (Tsingshan Holding Group): Massive investments in Indonesia, driving prices down

Russia (Norilsk Nickel): Largest Class 1 Nickel producer

Canada & Australia: ESG-focused, supplying European markets

Vale & BHP: Western giants valued by Tesla

⚡ EV Battery Battlefield

Nickel-based (NCM/NCA): Range >500 km, suited for luxury and high-performance vehicles

LFP (Lithium Iron Phosphate): Cheaper, safer, ideal for city cars and ESS

Recycling: Old batteries will become a key nickel source in the future

Price & Market Outlook

2026: Stable to slightly upward ($17,000–19,000/ton) if Indonesia maintains strict quotas

2030–2040: Clean energy demand expected to exceed 50% of global nickel consumption

Battery Recycling: Emerging as a new supply source, reducing reliance on mining

Marketing Summary

Nickel is evolving from a “heavy industry metal” to a “clean energy metal”.

EV and clean energy producers are the new driving force

Indonesia and China dominate global supply dynamics

Recycling will rebalance the market in the next decade

Sustained upward price trend expected after 2030

About SO OK TRADING

In this strategic metal battleground, SO OK TRADING is committed to bridging premium Thai non-ferrous metal producers with global markets. With expertise in non-ferrous metals and clean energy, we are your trusted business partner.

For Nickel inquiries:

Visit www.sooktrading.com → Click “Give Inquiry”

Or contact us directly via email: sooktrading@outlook.com