Greenland 2026: A Resource Treasure and a Nation of Geopolitical & Economic Importance SO OK TRADING Summary

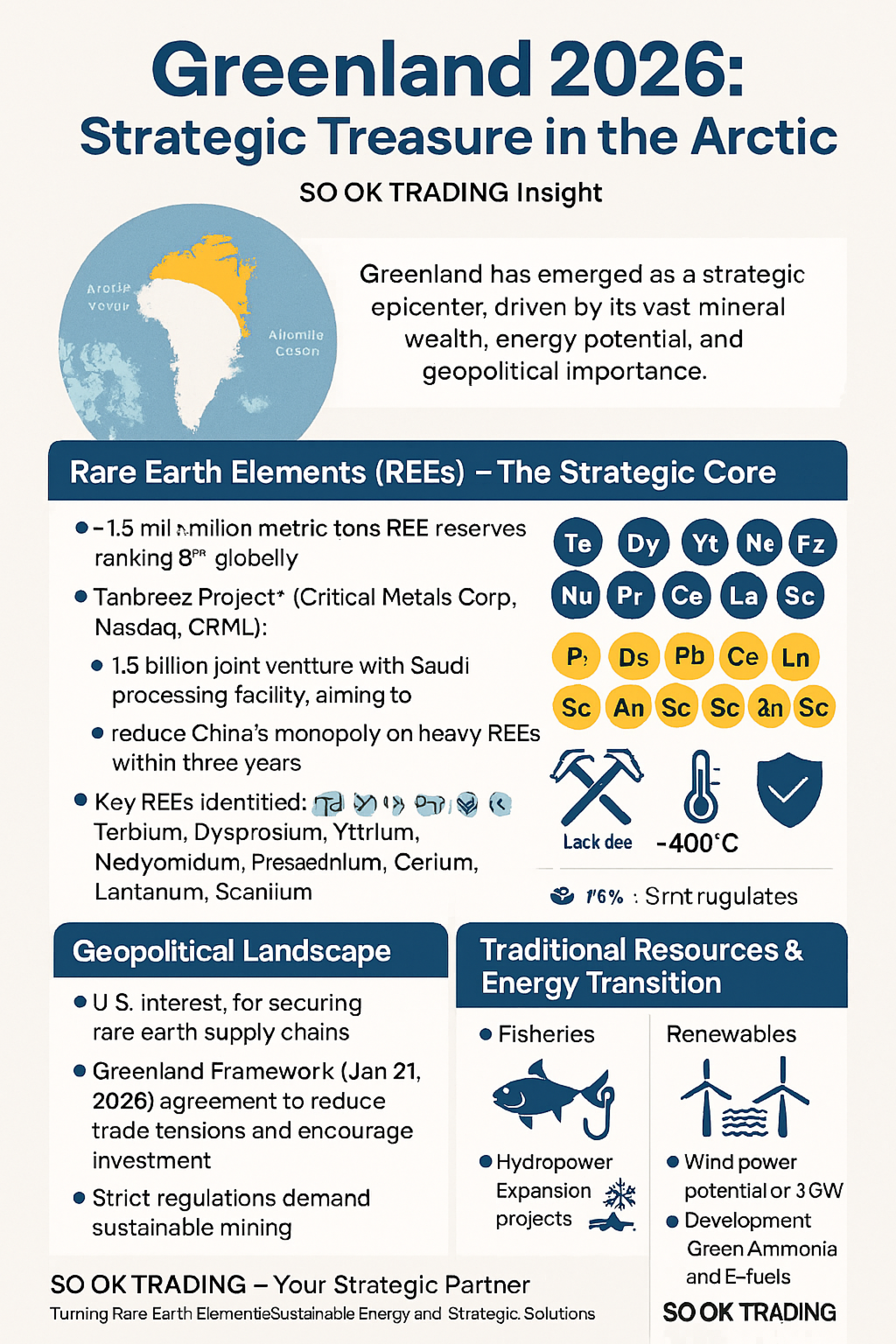

Greenland 2026: Strategic Treasure in the Arctic

SO OK TRADING Insight

Greenland – From Remote Island to Global Strategic Hub

Greenland, the world’s largest island, has emerged as a strategic epicenter in 2026. Its vast mineral wealth, energy potential, and geopolitical importance are reshaping the global supply chain for clean technology and advanced industries.

Expanded Highlights

Rare Earth Elements (REEs) – The Strategic Core

Greenland holds ~1.5 million metric tons of REE reserves, ranking 8th globally.

Tanbreez Project (Critical Metals Corp, Nasdaq: CRML):

Construction of a pilot plant began in January 2026, with launch scheduled for May.

A $1.5 billion joint venture with Saudi industry groups will establish a large-scale processing facility, supplying REEs to U.S. defense and EV industries.

Production expected in 2027, aiming to reduce China’s monopoly on heavy REEs from 97% to ~50% within three years.

Kvanefjeld Project: Stalled due to Greenland’s uranium mining ban. Legal disputes with Energy Transition Minerals highlight the regulatory complexity of resource development.

Key REEs identified: Terbium, Dysprosium, Yttrium, Neodymium, Praseodymium, Cerium, Lanthanum, Scandium.

Other Strategic Minerals

Graphite (battery anodes), molybdenum, zinc, copper, nickel, titanium.

Zirconium, niobium, tantalum, gallium, hafnium – critical for semiconductors, aerospace, and nuclear industries.

Mining & Infrastructure Challenges

Only two operational mines: gold (south) and anorthosite (feldspar, west).

Harsh climate (-40°C) and lack of deep-water ports, roads, and power plants raise costs 2–3 times higher than other regions.

Strict environmental regulations demand sustainable mining practices.

Geopolitical Landscape

U.S. Interest: Greenland seen as vital for securing rare earth supply chains.

Greenland Framework (Jan 21, 2026): New cooperation agreement to reduce trade tensions and encourage sustainable investment.

Global Competition: China, U.S., EU, and Middle Eastern investors are all vying for access to Greenland’s resources.

Traditional Resources & Energy Transition

Fisheries: Still account for 90% of exports, sustaining local livelihoods.

Oil & Gas: Estimated reserves of 17.5 billion barrels of crude oil and vast natural gas fields. Exploration remains limited due to environmental restrictions.

Renewables:

Hydropower already supplies 70% of electricity, with expansion projects underway (Buksefjord, Aasiaat, Qasigiannguit).

Wind power potential of 3 GW, with plans to export electricity via subsea cables to Europe and the U.S.

Development of Green Ammonia and E-fuels positions Greenland as a future exporter of clean fuels.

Greenland in the “Arctic Decade”

By 2026, Greenland is transforming into:

A strategic partner in clean tech supply chains, reducing Western dependence on China.

An Arctic logistics hub, with three new international airports (Nuuk, Ilulissat, Qaqortoq) lowering export costs and boosting eco-tourism.

A global clean energy producer, exporting hydropower, wind energy, green hydrogen, and green ammonia.

A geopolitical pivot, balancing resource exploitation with sustainability and sovereignty.

SO OK TRADING – Your Strategic Partner

As Greenland rises as a global resource hub, SO OK TRADING is ready to support businesses with:

Reliable rare earth supply: Neodymium, Dysprosium, and other strategic minerals sourced responsibly.

Integrated clean energy solutions: Solar + Battery ESS, magnetic systems, and industrial energy infrastructure.

Customized solutions: Covering residential, commercial, and industrial needs.

Global credibility: Partnerships with leading brands and adherence to international standards.

SO OK TRADING – Turning Rare Earth Elements into Sustainable Energy and Strategic Solutions for Your Future

Contact us today to explore tailored packages for your business and industry.