“Oil War – Global Plastic Crisis: Total Disrupt of World Industries, The Era of High Costs, Supply Chain Turbulence, and Business Game-Changing” Article by SO OK TRADING : March 20, 2026

“Oil War – Global Plastic Crisis: The Era of High Costs, Supply Chain Volatility, and Business Game-Changing”

Impact of the U.S.–Israel–Iran War on Global Supply Chains, the Plastics Industry, and World Industries

Article by SO OK TRADING : March 20, 2026

March 2026 – A Turning Point for Global Petrochemicals

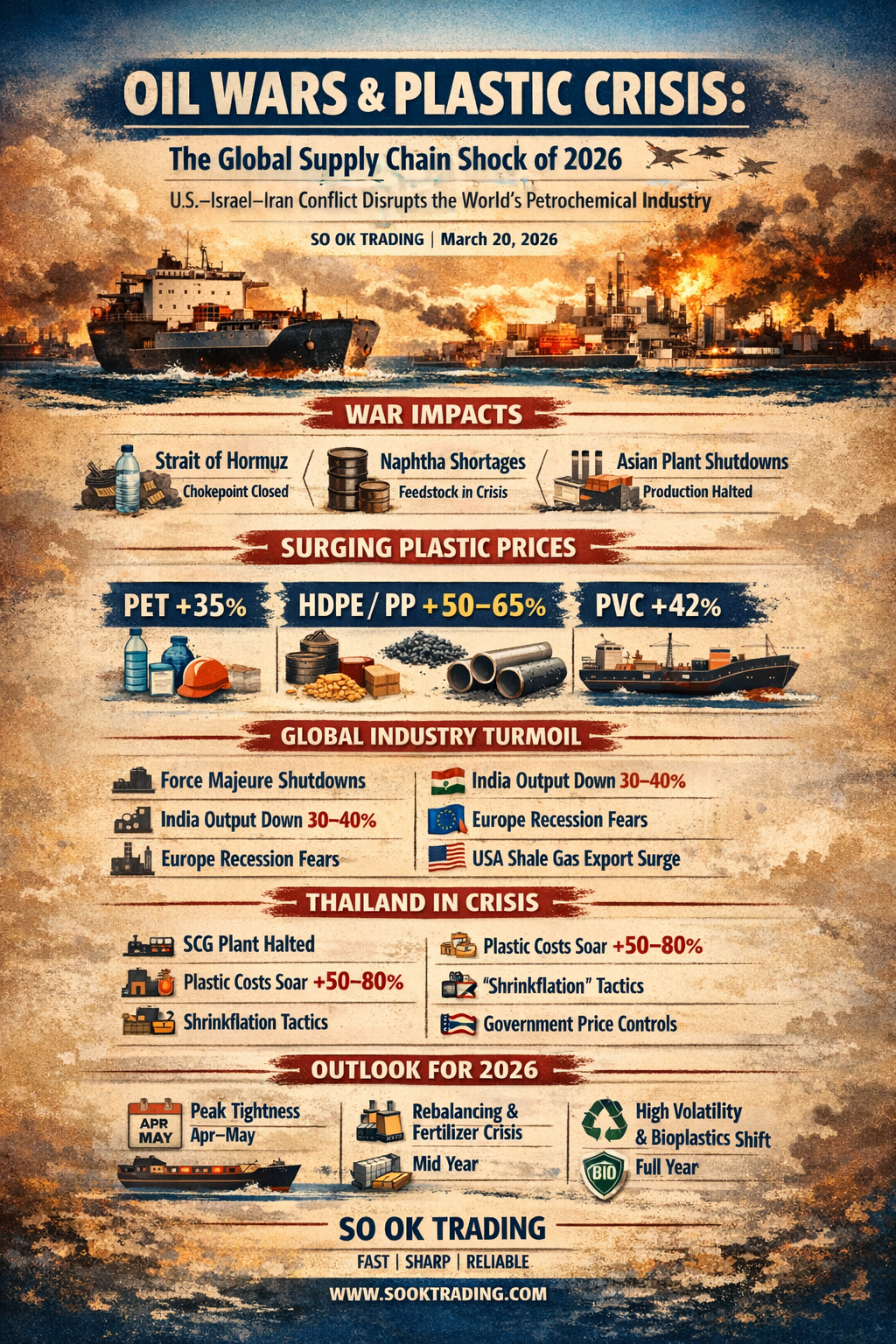

The war in Iran and the closure of the Strait of Hormuz abruptly halted oil and natural gas transport routes. The result: a raw material crisis and skyrocketing costs that struck everything from upstream factories to finished goods in consumers’ hands. The shock was immediate, creating a Total Disrupt across industries that no one anticipated.

Causes and Shocks from the War

Transport Routes Blocked: The Strait of Hormuz, the world’s vital artery, was shut down, sending Brent crude prices soaring and volatile.

Naphtha Shortages: A critical feedstock for plastics became scarce, hitting Japan and South Korea hardest.

Factories Halted: More than 10 plants across Asia shut down due to lack of raw materials.

Plastic Prices Surge

Just two weeks of war sent global plastic prices skyrocketing:

PET: +35%

HDPE, LDPE/LLDPE, PP: +50–65% (naphtha and LPG dependent)

PVC: +42%

On top of expensive feedstocks, freight rates from the Middle East to Asia jumped 3–4 times, inflating end-user costs even further.

Global Factory Impacts

Singapore, Indonesia, South Korea: Declared Force Majeure, halting operations.

India: Cut production by 30–40% as government diverted gas to households.

Europe: Facing both the Russia–Ukraine crisis and Middle East shortages; Germany warned of possible recession.

United States: Emerged as the “winner in crisis,” relying on domestic shale gas and boosting plastic exports.

Situation in Thailand

SCG Rayong Olefins (ROC) temporarily shut down due to naphtha shortages.

Plastic and packaging costs surged 50–80%, creating a “money can’t buy” crisis.

Consumer goods prices began rising; some brands adopted “shrinkflation” instead of direct price hikes.

Government intervened to stabilize prices and manage remaining stocks of plastics and fertilizers.

Regional Overview

China: Sustained production via coal-to-olefins.

Japan & South Korea: Cut output 30–50% due to reliance on Middle Eastern feedstocks.

Singapore: Struggled with soaring freight and insufficient storage.

Europe: Automotive industry worried about shortages of high-quality plastic components.

Australia: Fertilizer and agricultural plastics surged, raising food costs.

Africa: Foreign currency shortages hindered plastic imports, sparking packaging crises.

Price Outlook and Trends

Short Term (Apr–May 2026)

Peak Tightness: Prices remain high as old stocks run out.

Asian factories shut down to avoid losses.

Consumers face 10–15% price hikes.

Q2 2026

Rebalancing: Imports from the U.S. begin, despite high freight costs.

Fertilizer crisis: Natural gas diverted to petrochemicals, driving fertilizer prices up during planting season.

Political pressure: Governments may subsidize energy and raw materials if war drags on.

Full Year 2026

High Volatility: Even if war eases, petrochemical prices won’t return to old levels due to structural logistics cost changes.

Bio-Plastics & Recycling: Crisis accelerates adoption of bioplastics and recycling.

Production Shifts: Plastics-intensive industries (automotive, electronics) consider relocating to lower-risk regions like North America or Southeast Asia.

✨ Conclusion

2026 marks the end of the era of “cheap and abundant” petrochemicals, ushering in a new age of high costs, volatile supply, and relentless adaptation pressures. The Middle East war not only drove plastic prices sky-high but also rippled into food, fertilizer, and the global economy.

Brands and manufacturers that adapt quickly—through bioplastics, recycling, or new supply sources—will emerge as winners in this volatile era. Meanwhile, consumers worldwide must brace for the New Normal of higher costs and prices across the board.

✨ SO OK TRADING : FAST SHARP RELIABLE

Your trusted business partner in an era of volatility

VISIT US AT : WWW.SOOKTRADING.COM